Crisis Management and Deposit Insurance (CMDI) Framework

The European Commission's CMDI framework review enhances EU banking crisis management. It targets small and medium-sized banks to prevent reliance on public funds, ensuring financial stability. Key reforms include broadening public interest criteria and strengthening MREL, DGS, and SRF usage.

The European Commission's recent proposal to review the Crisis Management and Deposit Insurance (CMDI) framework marks a significant step in bolstering the European Union's (EU) capacity to manage and resolve banking crises effectively. This reform is particularly focused on addressing the shortcomings of the existing framework that have historically allowed small and medium-sized banks to evade stringent resolution processes.

These gaps often resulted in the reliance on public liquidation aid, thereby imposing significant burdens on taxpayers. The revised CMDI framework aims to create a more inclusive and robust system, ensuring financial stability across the EU by integrating smaller institutions into the resolution regime.

Source

[1]

Alessandro Micagni

Alessandro Micagni

[2]

Alessandro Micagni

CMDI Framework Review

The CMDI framework is designed to enhance the EU's financial stability by providing a structured and comprehensive approach to managing bank failures. This is achieved by minimizing the economic and taxpayer impact of such failures through a systematic resolution process. The primary objectives of the CMDI framework include:

- Enhancing Financial Stability: By incorporating a robust crisis management system that addresses the challenges posed by bank failures.

- Protecting Depositors: Ensuring that depositor interests are safeguarded through effective use of Deposit Guarantee Schemes (DGS).

- Reducing Taxpayer Burden: Preventing the use of taxpayer funds in bank bailouts by ensuring that the costs of bank failures are borne by shareholders and creditors.

Key Drivers for the CMDI Reform

The key drivers for the CMDI reform include:

- Inclusion of Smaller Banks: Expanding the scope of resolution to encompass small and medium-sized banks, which have previously operated on the periphery of the resolution framework.

- Public Interest Assessment (PIA): Broadening the public interest assessment criteria to ensure that the resolution authorities can effectively intervene in the insolvency of smaller banks when they pose a threat to financial stability.

- Strengthening MREL Requirements: Ensuring that all banks, regardless of size, maintain sufficient own funds and eligible liabilities to absorb losses and recapitalize, thus protecting taxpayers from the financial repercussions of bank failures.

- Enhanced Use of Industry-Funded Safety Nets: Utilizing national Deposit Guarantee Schemes (DGS) and the Single Resolution Fund (SRF) more effectively to finance resolution proceedings without disrupting the financial system.

Technical Overview of the CMDI Framework

The CMDI framework incorporates several technical components to enhance its effectiveness:

- Resolution Process: The framework outlines a clear and structured resolution process for banks, ensuring that the resolution of small and medium-sized banks is conducted in an orderly manner. This involves extending the resolution scope to these banks by broadening the public interest criterion.

- MREL Calibration: The Minimum Requirement for Own Funds and Eligible Liabilities (MREL) is a cornerstone of the CMDI framework. It mandates that banks maintain adequate loss-absorbing capacity to ensure that the financial burden of failures does not fall on taxpayers.

- Public Interest Assessment: The CMDI framework includes a detailed public interest assessment to determine whether a resolution is necessary. This assessment ensures that resolution authorities can effectively manage bank failures that pose a threat to financial stability.

- Use of DGS and SRF Funds: The framework facilitates the use of industry-funded safety nets like DGS and SRF to finance resolution proceedings. This approach ensures that failing banks can be resolved without significant disruptions to the financial system.

Financial Stability in the Crisis Management and Deposit Insurance (CMDI) Framework

Objectives of the CMDI Framework Review

The primary objective of the Crisis Management and Deposit Insurance (CMDI) framework is to enhance financial stability within the European Union (EU) by establishing a comprehensive and robust crisis management system. This system is designed to effectively address the unique challenges posed by bank failures, with a particular emphasis on small and medium-sized banks. The overarching goal is to minimize the economic and fiscal impact of these failures, thereby safeguarding taxpayers and maintaining orderly market conditions.

To achieve this, the CMDI framework focuses on several critical objectives:

- Systematic Resolution of Bank Failures: By providing clear guidelines and protocols for the resolution of failing banks, the CMDI framework ensures that disruptions to the financial system are minimized. This involves detailed planning and coordination among various regulatory and supervisory bodies to handle crises efficiently.

- Protection of Depositors: The framework aims to bolster depositor confidence by guaranteeing that their interests are protected during bank resolutions. This includes maintaining swift access to their funds and ensuring the integrity of deposit guarantee schemes (DGS).

- Minimization of Taxpayer Exposure: A core principle of the CMDI framework is to ensure that the costs associated with bank failures are primarily borne by the banks’ shareholders and creditors, rather than taxpayers. This is facilitated through mechanisms such as the Minimum Requirement for Own Funds and Eligible Liabilities (MREL), which mandates that banks hold sufficient loss-absorbing capital.

- Harmonized Regulatory Approach: By standardising the resolution processes across the EU, the CMDI framework promotes a level playing field for all banks, regardless of size. This harmonisation helps in reducing regulatory arbitrage and ensures consistent application of rules and procedures.

Challenges with the Previous Approach:

- Inconsistent Application: Smaller banks were often subject to national insolvency laws rather than the EU’s resolution regime, leading to inconsistencies in how bank failures were managed across different member states.

- Taxpayer Burden: The use of public funds to support liquidation processes placed a significant financial burden on taxpayers, contrary to the principle of minimizing taxpayer exposure.

- Market Disruptions: The ad-hoc nature of liquidations and the lack of a structured resolution process often led to market uncertainties and disruptions, undermining financial stability.

CMDI Framework’s Response: The CMDI framework aims to address these historical shortcomings by expanding the scope of resolution to include small and medium-sized banks. This expansion is guided by a broader interpretation of "public interest," which now encompasses the potential systemic impacts of smaller banks' failures on regional economies. The framework introduces several measures to ensure a more equitable and efficient resolution process:

- Broadened Public Interest Criterion: The revised CMDI framework redefines the public interest criterion to include the resolution of smaller banks whose failure could pose significant risks to financial stability. This broader scope allows resolution authorities to intervene more effectively.

- Structured Resolution Plans: Small and medium-sized banks are now required to develop detailed resolution plans, similar to those mandated for larger institutions. These plans outline the strategies and tools that will be used to manage a potential failure, ensuring preparedness and reducing ad-hoc decision-making.

- Enhanced Use of DGS and SRF: The CMDI framework facilitates the use of industry-funded safety nets, such as national DGS and the Single Resolution Fund (SRF), to finance resolution proceedings. This approach reduces the dependency on public funds and provides a more stable financial safety net.

Resolution Process for Small and Medium-Sized Banks

The revised Crisis Management and Deposit Insurance (CMDI) framework aims to significantly improve the resolution process for small and medium-sized banks. This improvement is primarily achieved by expanding the public interest criterion to encompass these banks, which historically were often managed outside the resolution framework. By broadening the public interest criterion, the CMDI framework ensures that resolution authorities have the mandate to intervene more effectively when the insolvency of a small or medium-sized bank poses a threat to financial stability. This approach is crucial for preventing systemic risks and maintaining confidence in the financial system.

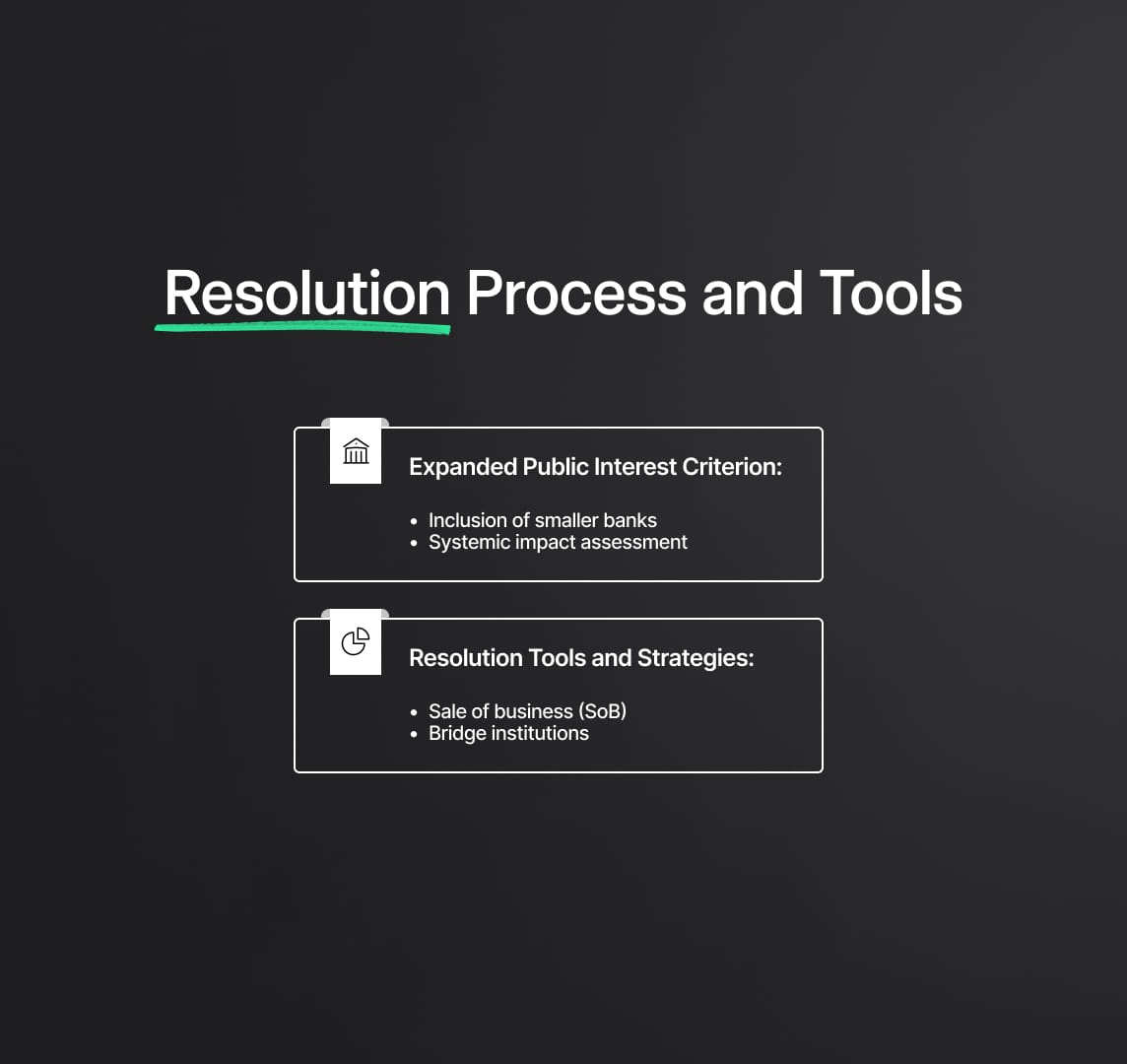

- Expanded Public Interest Criterion:

- Inclusion of Smaller Banks: The public interest assessment now considers the systemic implications of small and medium-sized bank failures. This broader scope allows for a more inclusive resolution process, ensuring that the failure of smaller banks, which could have regional economic impacts, is managed effectively.

- Assessment Criteria: The assessment includes evaluating the potential for contagion, the impact on market confidence, and the broader economic consequences of bank failures.

- Resolution Tools and Strategies:

- Sale of Business (SoB): This strategy involves transferring the bank’s assets and liabilities to a healthier institution. The CMDI framework enhances this process by ensuring that smaller banks can utilize SoB strategies effectively, thereby minimizing disruptions to banking services and maintaining depositor confidence.

- Bridge Institutions: The framework provides for the creation of bridge institutions that temporarily take over and operate the critical functions of a failing bank until a permanent solution is found.

Minimum Requirement for Own Funds and Eligible Liabilities (MREL)

The Minimum Requirement for Own Funds and Eligible Liabilities (MREL) is a cornerstone of the CMDI framework. MREL mandates that banks maintain sufficient loss-absorbing capacity to manage financial distress without resorting to public funds. This requirement is designed to ensure that shareholders and creditors bear the primary responsibility for absorbing losses and recapitalizing the bank, rather than relying on taxpayer support.

- MREL Calibration:

- Proportional Requirements: MREL targets are calibrated based on the size and complexity of the bank. For smaller banks, the CMDI framework allows for a more proportionate approach, recognizing their limited access to capital markets.

- Loss-Absorbing Instruments: Banks can meet MREL requirements through various instruments, including Common Equity Tier 1 (CET1) capital, subordinated debt, and other eligible liabilities. The framework specifies the criteria and hierarchy for these instruments to ensure effective loss absorption.

- Implementation and Compliance:

- Phased Implementation: The CMDI framework provides for a phased implementation of MREL requirements, allowing smaller banks adequate time to build up their loss-absorbing capacity.

- Supervisory Oversight: Regulators are tasked with monitoring banks' compliance with MREL targets, conducting regular assessments, and ensuring that banks maintain the necessary buffers to absorb potential losses.

Industry-Funded Safety Nets

The CMDI framework enhances the robustness of industry-funded safety nets, such as national Deposit Guarantee Schemes (DGSs) and the Single Resolution Fund (SRF). These safety nets are critical in providing additional financial resources for resolution proceedings, thereby reducing the reliance on taxpayer funds and ensuring a smoother resolution process for failing banks.

- Deposit Guarantee Schemes (DGS):

- Expanded Role in Resolution: DGS funds can be used not only for depositor payouts in insolvency scenarios but also to support resolution actions. This includes financing the transfer of assets and liabilities to another institution, thus preserving the continuity of banking services.

- Funding and Contributions: The CMDI framework stipulates that banks contribute to DGS based on their risk profile and size, ensuring that the schemes are adequately funded to handle potential failures.

- Single Resolution Fund (SRF):

- Access and Utilization: The SRF can be accessed to provide temporary financial support during resolution, particularly in cases where a bank’s internal loss-absorbing capacity is insufficient. This ensures that resolutions can be executed effectively without causing major market disruptions.

- Priority and Repayment: The CMDI framework outlines a clear hierarchy for the use of SRF funds, prioritizing the repayment to the SRF from the recovered assets of the resolved bank. This mechanism helps maintain the sustainability of the SRF.

Public Interest Assessment (PIA) in the Crisis Management and Deposit Insurance (CMDI) Framework

A cornerstone of the Crisis Management and Deposit Insurance (CMDI) Framework is the public interest assessment (PIA). This critical process determines whether the resolution objectives are at risk and mandates resolution actions accordingly. The PIA ensures that the resolution procedure is only initiated if it is necessary to protect financial stability, thereby safeguarding the economy and taxpayers from the fallout of bank failures.

- Comprehensive Threat Assessment:

- Systemic Impact Analysis: The resolution authority conducts a detailed analysis of the potential systemic impact of a bank's failure. This involves assessing the bank's interconnectedness with other financial institutions, its role in critical financial services, and the potential for contagion.

- Criteria for Public Interest: Specific criteria are set to evaluate public interest, including the bank's size, complexity, and the nature of its business. This ensures a standardized approach to determining whether a bank's failure would pose significant threats to financial stability.

- Resolution Objectives:

- Maintaining Financial Stability: The primary objective is to maintain overall financial stability. This involves preventing disruptions in the banking system that could lead to broader economic instability.

- Protecting Depositors: Ensuring that depositors are protected and have continued access to their funds is a crucial component of the resolution objectives. This protection helps maintain public confidence in the financial system.

- Minimizing Public Costs: The CMDI framework aims to resolve banks in a manner that minimizes the cost to taxpayers. This is achieved by ensuring that the bank's shareholders and creditors absorb the losses, rather than relying on public funds.

Insolvency Procedure

- Comparison of Insolvency and Resolution Procedures:

- Cost-Benefit Analysis: A detailed cost-benefit analysis is conducted to compare the potential outcomes of normal insolvency versus resolution. This includes evaluating the financial and operational impacts on the bank, its customers, and the wider economy.

- Recovery Rates: The analysis considers expected recovery rates for creditors under both procedures, ensuring that the chosen approach maximizes returns and minimizes losses.

- Assessment of Economic Disruptions:

- National and Regional Impacts: The Council's mandate emphasizes the importance of assessing the potential disruptions to the real economy at both national and regional levels. This involves evaluating how the failure of a small or medium-sized bank could impact local businesses, employment, and economic activities.

- Critical Functions: The assessment includes identifying the bank's critical functions that are essential for economic stability. If these functions are at risk of being disrupted, the resolution procedure is prioritized to ensure their continuity.

- Decision-Making Framework:

- Structured Evaluation Process: The CMDI framework provides a structured evaluation process for making decisions about the resolution or insolvency of banks. This process includes predefined triggers and thresholds to ensure consistency and transparency in decision-making.

- Coordination with Authorities: Effective coordination with national and regional authorities is essential to ensure that all relevant factors are considered in the public interest assessment. This collaboration helps align the resolution strategy with broader economic and financial stability goals.

Bridging the Gap in the CMDI Framework

One of the primary objectives of the CMDI reform is to facilitate the resolution of failing banks, thereby minimizing contagion risks and spillovers to the real economy. The Crisis Management and Deposit Insurance (CMDI) Framework aims to enhance the robustness and credibility of the resolution process by addressing funding issues that small and medium-sized banks often face. This involves the strategic use of Deposit Guarantee Schemes (DGS) and the Single Resolution Fund (SRF) to bridge financial gaps during resolution proceedings.

Utilization of DGS and SRF Funds:

- Role of DGS in Resolution:

- Extended Functionality: The CMDI framework extends the role of DGS beyond traditional depositor payouts to actively support resolution strategies. This extension includes facilitating asset transfers and providing liquidity to ensure the continuity of critical banking functions.

- Risk Mitigation: By using DGS funds in a controlled manner, the framework aims to mitigate the risk of bank runs and maintain depositor confidence during the resolution process.

- Single Resolution Fund (SRF):

- Support Mechanism: The SRF acts as a financial backstop, providing additional resources to manage the resolution of failing banks. This fund is particularly crucial for medium-sized banks that may not have sufficient internal resources to meet resolution requirements.

- Operational Integration: The CMDI framework integrates the SRF into the resolution planning and execution phases, ensuring that funds are available to bridge financial gaps and facilitate orderly resolution.

Safeguards on the Use of DGS and SRF Funds

To prevent unintended consequences and moral hazard, the CMDI framework incorporates stringent safeguards governing the use of DGS and SRF funds. These safeguards ensure that these funds are not used as a substitute for loss absorption by the failing bank’s shareholders and creditors.

- Loss Absorption Hierarchy:

- Priority Structure: The CMDI framework enforces a clear priority structure, ensuring that shareholders and creditors bear the initial losses before any DGS or SRF funds are deployed. This hierarchy maintains accountability and minimizes reliance on public funds.

- Regulatory Oversight: Strict regulatory oversight is mandated to monitor the application of these funds, ensuring compliance with the loss absorption hierarchy and preventing misuse.

- Risk Containment Measures:

- Cap on Fund Usage: A cap is placed on the amount of DGS and SRF funds that can be used in resolution scenarios. This cap is designed to protect the solvency of these funds and ensure their availability for future crises.

- Contingency Planning: Resolution authorities are required to develop detailed contingency plans that outline the specific conditions under which DGS and SRF funds can be utilized. These plans include predefined triggers and conditions to activate fund usage.

Burden Sharing

The CMDI framework mandates adequate burden sharing between the DGS and SRF, ensuring a balanced approach to resolution funding. The Single Resolution Fund (SRF) is given priority for repayment purposes, with the Deposit Guarantee Scheme (DGS) providing supplementary support within defined limits.

- Repayment Priority:

- SRF Priority: The SRF is prioritized for repayment, ensuring that its resources are replenished first. This prioritization helps maintain the SRF’s capacity to support future resolutions.

- DGS Role: The DGS plays a supplementary role, providing additional funds when necessary, but always within the constraints of its primary function of depositor protection.

- Pecking Order:

- Balanced Approach: The CMDI framework establishes a ‘pecking order’ for the utilization of resolution funds, ensuring a structured and balanced approach. This order maintains financial stability while protecting the integrity of the DGS and SRF.

Restrictions for Larger Banks

To address the potential impact of larger banks on the financial system, the CMDI framework imposes stricter requirements and limitations on the use of DGS and SRF funds for banks with a balance sheet size between €30 billion and €80 billion. These measures are designed to limit the systemic risk posed by larger institutions and ensure that resolution strategies are both effective and proportionate.

- Stricter Criteria:

- Eligibility Criteria: Enhanced eligibility criteria are applied to larger banks, ensuring that only those meeting specific conditions can access DGS and SRF funds. This approach targets resources where they are most needed while maintaining systemic stability.

- Temporary Measure: This provision is a temporary measure, available for ten years after the CMDI framework’s entry into force. This period allows for a gradual transition to more sustainable resolution funding mechanisms.

- Monitoring and Compliance:

- Regular Reviews: The CMDI framework includes provisions for regular reviews and updates to the restrictions, ensuring they remain relevant and effective. This dynamic approach allows for adjustments based on evolving financial conditions and institutional needs.

- Compliance Enforcement: Stringent compliance mechanisms are in place to enforce the restrictions, with penalties for non-compliance. This enforcement ensures adherence to the framework and protects the integrity of the resolution process.

Hierarchy of Claims and Least Cost Test in Crisis Management and Deposit Insurance (CMDI) Scheme

Maintaining Depositor Preference

The CMDI framework is designed to prioritise the protection of depositors in the event of bank insolvency. To achieve this, the framework maintains a hierarchy of claims that ensures deposits benefit from a general preference. This hierarchy is crucial for enhancing depositor confidence and ensuring financial stability.

- General Preference for Deposits:

- Prioritization of Claims: Deposits are given a general preference over other unsecured claims. This prioritization ensures that in the event of bank liquidation, depositors are among the first to be reimbursed from the available assets of the insolvent bank.

- Impact on Creditor Hierarchy: By prioritizing deposits, the CMDI framework effectively reduces the risk to depositors, thereby maintaining their confidence in the banking system. This preference helps to prevent bank runs and other destabilizing behaviors during financial distress.

- Introduction of Super-Preference Status:

- Enhanced Protection for DGS-Protected Depositors: The Council’s mandate reintroduces a 'super-preference status' for depositors protected under Deposit Guarantee Schemes (DGS). This status further elevates the priority of these deposits in the insolvency hierarchy.

- DGS Subrogation: In cases where the DGS steps in to reimburse depositors, it inherits their claims against the insolvent bank. The super-preference status ensures that the DGS is reimbursed before other unsecured creditors, preserving its financial integrity and ability to protect depositors in future crises.

Effective Use of DGS Funds

The CMDI framework includes rigorous measures to ensure that DGS funds are used effectively and efficiently. The framework broadens the 'least cost test' to determine the most cost-effective use of DGS resources, balancing the need to protect depositors with the need to maintain financial stability.

- Broadened Least Cost Test:

- Holistic Cost Assessment: The least cost test is designed to ensure that the cost of using DGS funds does not exceed the hypothetical cost of reimbursing covered depositors in a liquidation scenario. This assessment includes direct costs, potential second-round effects, systemic costs, and opportunity costs.

- Application Beyond Pure Payouts: The broadened least cost test applies not only to pure payout scenarios but also to other resolution strategies that might involve the use of DGS funds, such as facilitating mergers or asset transfers. This ensures a comprehensive evaluation of the most efficient use of resources.

- Implementation Mechanisms:

- Coordination Between Authorities: Effective implementation of the least cost test requires seamless cooperation between national DGS managers and resolution authorities. This cooperation includes information sharing and joint modeling efforts to ensure accurate and comprehensive cost assessments.

- Regulatory Framework: The CMDI framework establishes a robust legal basis for the least cost test, ensuring that it is consistently applied and that decisions are transparent and accountable.

Preventive and Alternative Measures

The CMDI framework differentiates between preventive measures aimed at averting bank failures and alternative measures used during resolution. The Council’s mandate provides clear guidelines for these measures, ensuring that they are effectively implemented to maintain financial stability.

- Preventive Measures:

- Objective: Preventive measures are designed to address emerging risks before they escalate into full-blown crises. These measures include regulatory interventions, capital injections, and liquidity support to stabilize a bank's operations.

- Process Flow and Authority Involvement: The mandate clarifies the roles and responsibilities of various authorities in implementing preventive measures. This includes timelines for action, criteria for intervention, and mechanisms for coordination among supervisory bodies.

- Institutional Protection Schemes (IPS):

- Role of IPS: Institutional Protection Schemes (IPS) provide mutual support among member banks, often funded by contributions from these banks rather than public funds. IPS can implement preventive measures to maintain stability within the network.

- Framework for IPS Operations: The CMDI framework preserves the functionality of IPS by establishing clear guidelines for their preventive actions. This ensures that IPS can operate effectively without conflicting with broader regulatory objectives.

Extraordinary Public Financial Support

In extraordinary circumstances, the CMDI framework allows for public financial support to failing banks. The Council’s mandate outlines the forms of permissible support and the process for its application, ensuring that such interventions are judiciously used and effectively managed.

- Forms of Public Financial Support:

- Capital Injections and Guarantees: Public financial support can take the form of capital injections, guarantees, or other financial instruments aimed at stabilizing a failing bank. These interventions are designed to be temporary and targeted, with clear exit strategies.

- Conditions for Support: The mandate specifies the conditions under which public financial support can be provided, including thresholds for systemic risk, criteria for bank eligibility, and requirements for burden sharing among private stakeholders.

- Application Process:

- Workable Framework: The CMDI framework establishes a detailed process for the application of public financial support. This includes stages of approval, oversight mechanisms, and transparency requirements to ensure that support measures are implemented effectively and responsibly.

- Coordination with EU Authorities: The process involves close coordination with EU authorities to align national interventions with broader European objectives, ensuring a cohesive and unified response to banking crises.

CMDI Framework: SRB Governance

The governance structure within the CMDI framework is crucial for ensuring effective crisis management and resolution of failing banks. The Council's mandate confirms the pivotal role of the executive session of the Single Resolution Board (SRB) in adopting legal instruments essential for resolution planning and execution. This structure promotes a streamlined and efficient decision-making process.

- Executive Session:

- Primary Responsibilities: The executive session is responsible for adopting the SRB's legal instruments, which include resolution plans, MREL requirements, and decisions on the use of the Single Resolution Fund (SRF).

- Composition and Functioning: Typically composed of the Chair, Vice-Chair, and permanent members, the executive session operates with a high degree of independence, ensuring decisions are made swiftly and based on technical criteria.

- Plenary Session:

- Role and Function: The plenary session includes representatives from national resolution authorities and addresses broader policy issues, strategic decisions, and significant resolution cases. It ensures that the interests and insights of national authorities are integrated into the decision-making process.

- Promoting Inclusiveness: By involving national resolution authorities, the plenary session fosters an inclusive Single Resolution Mechanism (SRM), balancing the need for centralized decision-making with regional perspectives.

Supervisory and Early Intervention Measures

Early intervention is a cornerstone of the CMDI framework, designed to prevent bank failures before they become systemic threats. The CMDI proposal enhances the existing supervisory framework by providing authorities with a comprehensive set of tools for early intervention.

- Improved Supervisory Tools:

- Triggers for Action: The framework specifies clear metrics and thresholds, such as breaches in capital requirements or liquidity shortfalls, that trigger early intervention measures. These metrics are continuously monitored to ensure timely action.

- Range of Interventions: Authorities can impose restrictions on dividend payments, require capital increases, mandate changes in business strategy, and replace management to stabilize banks showing signs of distress.

- Collaboration Among Authorities:

- Coordinated Efforts: Enhanced cooperation between the European Central Bank (ECB), SRB, and national supervisory authorities ensures a unified approach. This collaboration is facilitated through regular information sharing, joint inspections, and coordinated action plans.

Principle of Optionality

The CMDI framework's principle of optionality provides authorities with the flexibility to choose from a range of tools and strategies tailored to the specific circumstances of each bank crisis.

- Comprehensive Toolkit:

- Resolution Tools: These include bail-in mechanisms, asset separation, bridge banks, and sale of business options, allowing for tailored resolution strategies that minimize disruption and maximize recovery.

- Preventive Measures: Authorities can implement measures such as temporary public ownership, precautionary recapitalisation, and liquidity support to stabilize banks before resolution becomes necessary.

- Tailored Interventions:

- Case-by-Case Basis: The optionality principle ensures that interventions are proportionate and effective, considering the unique operational and financial structure of each bank. This approach helps in mitigating systemic risks while preserving the stability of the broader financial system.

Precautionary Recapitalisation

Precautionary recapitalisation is a preventive measure that allows for the injection of public funds into fundamentally sound banks facing temporary difficulties. This measure is strictly regulated to prevent misuse and ensure financial stability.

- Strict Conditions:

- Eligibility Criteria: Only viable banks with temporary capital shortfalls are eligible for precautionary recapitalisation. The measure cannot be used to cover losses that were incurred before the recapitalisation.

- Regulatory Approval: The European Commission and the ECB must approve any precautionary recapitalisation, ensuring it meets strict criteria and does not distort competition.

- Safeguarding Public Funds:

- Burden Sharing: Shareholders and junior creditors must absorb losses before public funds are used. This requirement ensures that public funds are only used as a last resort.

- Exit Strategy: Banks receiving precautionary recapitalisation must present a clear plan to restore their capital position and repay the public funds, ensuring the measure is temporary.

Deposit Guarantee Schemes (DGSs)

Traditionally, Deposit Guarantee Schemes (DGSs) have served as a safety net for depositors, ensuring the payout of covered deposits in the event of a bank failure. The CMDI reform proposes an expanded role for DGSs, allowing their funds to be used in various resolution scenarios.

Resolution Scenarios:

- Support for Resolutions: DGS funds can be used to facilitate the transfer of deposits to another institution, support bridge banks, or finance other resolution tools. This expanded role helps to ensure that depositors continue to have access to their funds during the resolution process.

- Limits and Safeguards: The CMDI framework imposes strict limits on the use of DGS funds to prevent depletion and ensure they remain available to cover depositor payouts. The use of these funds must pass the least cost test to ensure cost-effectiveness.

- Preventive and Alternative Measures:

- Flexibility in Use: DGSs can also be used for preventive measures, such as funding early interventions that prevent a bank's failure, and alternative measures, such as supporting mergers or restructuring plans that enhance the stability of the banking sector.

Information Sharing

Effective crisis management requires close collaboration and information sharing among all relevant stakeholders. The CMDI framework emphasizes the importance of cooperation between the European Central Bank (ECB), the Single Resolution Board (SRB), and other authorities.

- Coordination Mechanisms:

- Joint Decision-Making: Regular meetings and communication channels between the ECB, SRB, and national authorities ensure coordinated and timely decision-making during crises.

- Information Sharing Protocols: Establishing robust protocols for sharing information on financial health, supervisory actions, and resolution plans ensures that all relevant parties are well-informed and can act swiftly.

- Crisis Simulations and Drills:

- Preparedness Activities: Regular crisis simulations and drills involving all stakeholders help to test the effectiveness of coordination mechanisms and ensure readiness for actual crises. These activities help identify potential gaps and areas for improvement in crisis response strategies.

Liquidity in Resolution

The availability of liquidity is vital for the successful resolution of banks. Recent financial turmoil has demonstrated the need for credible liquidity backstops that are transparent and understood by market participants and depositors.

- Liquidity Backstops:

- Central Bank Support: The CMDI framework ensures that central banks can provide emergency liquidity assistance to solvent banks undergoing resolution. This support is crucial for maintaining confidence and preventing bank runs.

- Resolution Funds: The Single Resolution Fund (SRF) can also provide liquidity support during resolution, ensuring that resolved entities have the necessary funds to continue operations and meet obligations.

- Transparency and Communication:

- Clear Guidelines: The CMDI framework establishes clear guidelines for the provision and use of liquidity during resolution. These guidelines ensure that all parties understand the conditions and processes for accessing liquidity support.

- Market Communication: Transparent communication with market participants about the availability and use of liquidity backstops helps to maintain confidence and stability during the resolution process.

Crisis Management and Deposit Insurance (CMDI) Framework: Insolvency Laws

Cross-Border Banking Groups

The heterogeneity of national insolvency regimes presents a significant challenge in the resolution of cross-border banking groups. This diversity in legal frameworks can complicate and delay resolution processes, undermining financial stability. Harmonising insolvency laws across the EU is essential to strengthen the CMDI framework, ensuring a consistent and effective approach to managing banking crises.

- Inconsistencies in National Laws:

- Diverse Procedures: Different countries have varying insolvency procedures, which can lead to conflicting legal outcomes for cross-border banks. These discrepancies make it challenging to coordinate a unified resolution strategy.

- Legal Uncertainty: The lack of harmonization results in legal uncertainty, which can deter timely intervention and complicate the execution of resolution plans.

- Benefits of Harmonization:

- Streamlined Processes: Harmonized insolvency laws would streamline resolution processes across member states, ensuring quicker and more efficient handling of bank failures.

- Increased Predictability: A unified legal framework would provide greater predictability for banks and resolution authorities, enhancing confidence in the resolution process and financial stability.

- Steps Towards Harmonization:

- Legislative Alignment: The European Commission can work towards aligning national insolvency laws with the principles of the CMDI framework. This would involve drafting EU-wide regulations that standardize key aspects of insolvency procedures.

- Cooperation Mechanisms: Establishing robust cooperation mechanisms between national authorities and EU bodies like the European Central Bank (ECB) and Single Resolution Board (SRB) is crucial. These mechanisms would facilitate information sharing and coordinated action during cross-border resolutions.

Institutional Protection Schemes (IPS)

Institutional Protection Schemes (IPS) play a vital role in the crisis management framework, providing ex-ante funds to address sectoral imbalances. These systems have proven effective in supporting the stability of the banking sector and should be integrated into the CMDI framework to enhance its robustness.

- Functioning of IPS:

- Preventive Measures: IPS can implement preventive measures to support member banks in distress, reducing the likelihood of failure and enhancing overall sector stability.

- Ex-Ante Funding: IPS collect funds from member banks on an ongoing basis, creating a financial buffer that can be used in times of crisis. This proactive approach helps mitigate systemic risks.

- Integration into CMDI:

- Complementary Role: Integrating IPS into the CMDI framework ensures that these schemes complement other resolution tools, providing additional layers of protection and support.

- Coordination with Authorities: Enhanced coordination between IPS and resolution authorities ensures that preventive and resolution measures are well-aligned, maximizing their effectiveness.

Next Steps

- Legislative Process:

- Interinstitutional Negotiations: The European Parliament adopted its position in the first reading on April 24, 2024. The Council's agreement paves the way for interinstitutional negotiations, with the aim of reaching an agreement in early second reading. Once an agreement is reached, it will need to be formally adopted before becoming law.

- Background and Future Directions:

- Legislative Proposals: On April 18, the Commission adopted a set of legislative proposals to review the CMDI framework. These proposals include amendments to the bank recovery and resolution directive, the deposit guarantee schemes directive, and the single resolution mechanism regulation. Targeted amendments to the daisy chain act were adopted on March 26, 2024.

Reduce your

compliance risks