DPE Regime for Post-Trade Transparency of OTC Transactions

On July 22, 2024, ESMA introduced the Designated Publishing Entity (DPE) regime under the MiFIR review to enhance OTC transaction transparency and streamline reporting. This article details ESMA's guidelines, focusing on the DPE register, technical integration, and the transition timeline.

Introduction to the DPE Regime

On July 22, 2024, the European Securities and Markets Authority (ESMA) issued a pivotal public statement addressing the transition to a new regime for post-trade transparency of over-the-counter (OTC) transactions. This new regime, referred to as the Designated Publishing Entity (DPE) regime, was introduced as part of the comprehensive Markets in Financial Instruments Regulation (MiFIR) review. The MiFIR review aims to enhance market transparency, streamline reporting processes, and ensure robust regulatory oversight. This article delves into the intricate details of the new regime, offering a technical and thorough overview based on ESMA's latest guidelines.

Source

[1]

Alessandro Micagni

Alessandro Micagni

Establishment of the DPE Register

As mandated by MiFIR, ESMA is required to establish a comprehensive public register of all DPEs by September 29, 2024. This register will detail the identity of DPEs, along with the specific classes of financial instruments for which they act as DPEs. The register aims to facilitate market participants' preparation for the new regime by providing a centralized and accessible source of information. Initially, the DPE register will be published in XLSX format on ESMA's website, ensuring that all relevant data is readily available for stakeholders to access and review.

Technical Specifications and Integration into ESMA’s IT Systems

In parallel with the establishment of the DPE register, ESMA is undertaking significant technical integration efforts to incorporate the register into its existing IT systems. This integration is expected to be completed by the end of 2025, transitioning the register from its initial XLSX format to a fully integrated, dynamic system accessible via a dedicated portal. This transition will not only enhance the accessibility and usability of the register but also ensure that it is automatically updated with new information as NCAs introduce modifications. This automatic updating is crucial for maintaining the accuracy and relevance of the register, providing real-time data to market participants.

Classes of Financial Instruments Covered

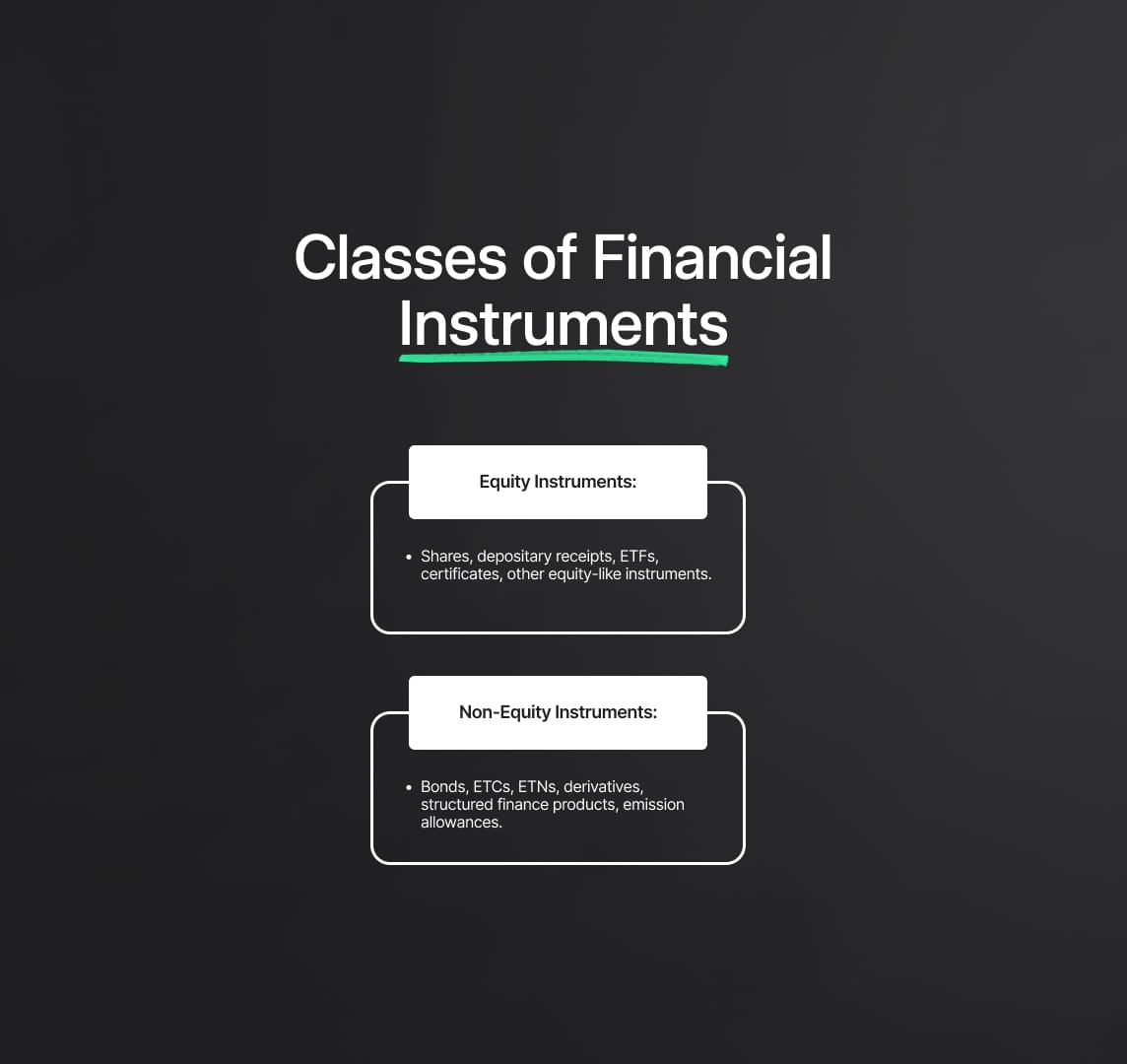

The DPE register will encompass a wide array of financial instruments, categorised into equity and non-equity instruments. The equity instruments include shares, depositary receipts, ETFs, certificates, and other equity-like financial instruments. The non-equity instruments cover bonds, ETCs, ETNs, interest rate derivatives, credit derivatives, structured finance products, and emission allowances. This comprehensive coverage ensures that all relevant transactions are captured, thereby enhancing the overall transparency and integrity of the market.

No Transitional Provisions

The MiFIR review does not include transitional provisions for the application of the DPE regime. This necessitates a well-coordinated and prompt approach to ensure a seamless transition from the current system to the new regime. The absence of transitional provisions underscores the importance of immediate compliance and preparation by market participants, highlighting the urgency for investment firms to align their operations with the new regulatory requirements.

Two-Step Transition Approach

To facilitate a smooth transition, ESMA and NCAs have agreed on a two-step approach to implement the DPE regime effectively:

- Initial Publication of the DPE Register: ESMA will publish the initial DPE register on September 29, 2024. This publication will provide market participants with the necessary information to prepare for the forthcoming changes.

- Full Operational Status: The DPE regime for post-trade transparency will become fully operational on February 3, 2025. From this date onwards, registered DPEs involved in a transaction must make the transaction public through an APA, and the reliance on SIs will cease.

Understanding the DPE Regime

Key Provisions of the MiFIR Review

The Markets in Financial Instruments Regulation (MiFIR) review has introduced several pivotal provisions that significantly reshape the post-trade transparency landscape. Central to these provisions is the empowerment of National Competent Authorities (NCAs) to grant investment firms the status of Designated Publishing Entities (DPEs). This empowerment, encapsulated in Article 21a of MiFIR, establishes a new paradigm for transaction transparency in financial markets.

Responsibilities of Designated Publishing Entities (DPEs)

According to Article 21a, when DPEs are party to a transaction, they are responsible for making the transaction public through an approved publication arrangement (APA). This marks a substantial shift from the previous reliance on Systematic Internalisers (SIs), who traditionally bore the responsibility for transaction publication. The shift to DPEs aims to centralize and standardize the transparency process, ensuring a more robust and efficient reporting mechanism. This change is expected to enhance the accuracy, reliability, and accessibility of post-trade data, thereby fostering greater market transparency and investor confidence.

Establishment of the DPE Register

As part of the new regulatory framework, ESMA is mandated to establish a comprehensive public register of all DPEs by September 29, 2024. This register is a crucial component of the new regime, designed to provide transparency and operational readiness. It will detail the identity of each DPE and the specific classes of financial instruments for which they act as DPEs. The initial publication of the DPE register will be in XLSX format on ESMA’s website, ensuring that market participants have access to essential information needed for compliance and preparation.

Technical Specifications of the DPE Register

The DPE register will include detailed information about each DPE, including their legal identifiers and the classes of financial instruments they cover. The register will cover both equity instruments (such as shares, depositary receipts, ETFs, certificates, and other equity-like financial instruments) and non-equity instruments (including bonds, ETCs, ETNs, interest rate derivatives, credit derivatives, structured finance products, and emission allowances). This comprehensive coverage ensures that all relevant transactions are captured under the new transparency requirements.

Transition Timeline and Steps

No Transitional Provisions

The MiFIR review does not provide for any transitional provisions for the application of the DPE regime. This lack of transitional provisions underscores the importance of an immediate and well-coordinated approach to ensure a smooth transition from the existing system to the new DPE regime.

Two-Step Transition Approach

To manage this transition effectively, ESMA and NCAs have agreed on a structured two-step approach:

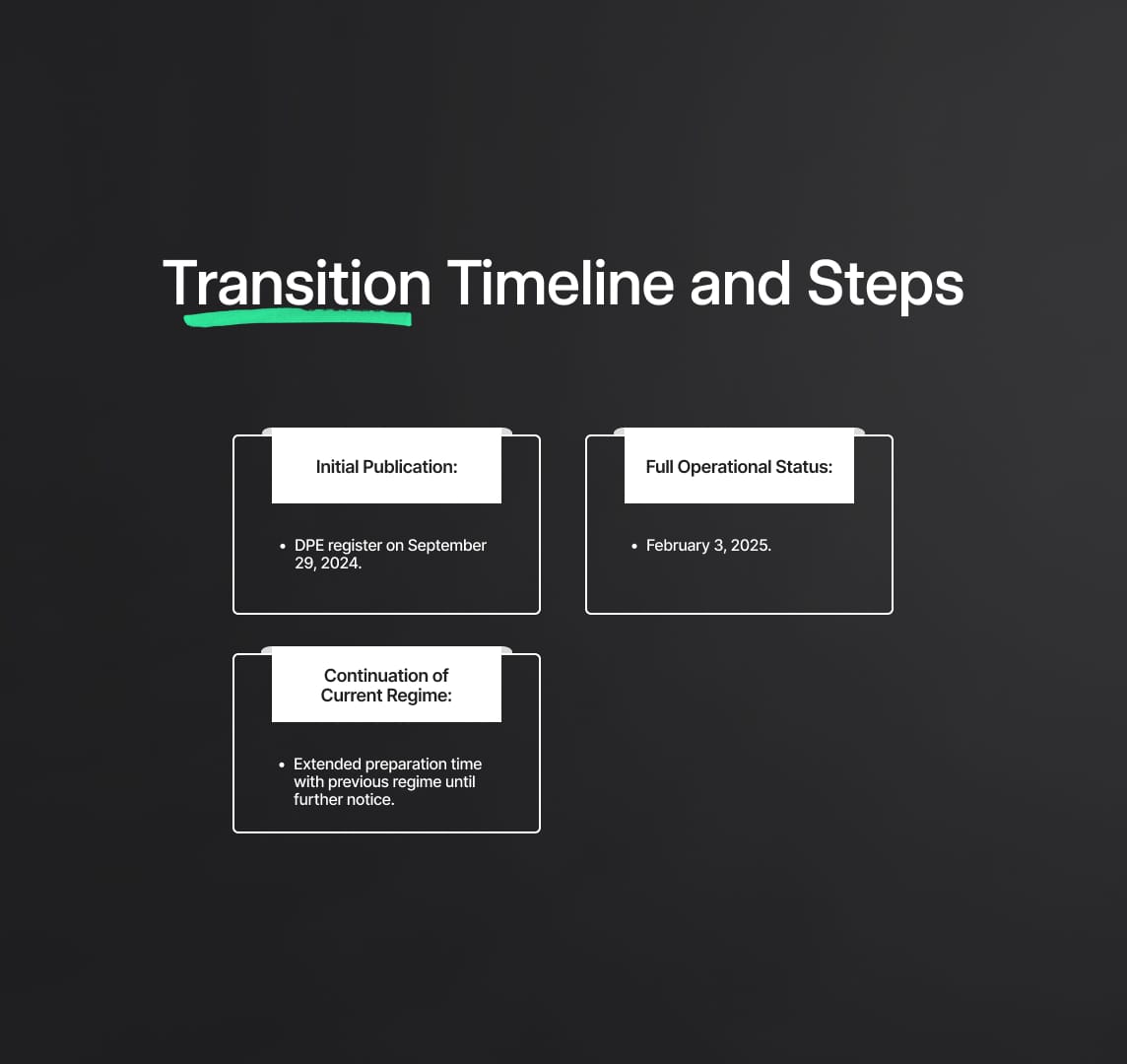

- Initial Publication of the DPE Register: On September 29, 2024, ESMA will publish the initial DPE register. This publication is designed to provide market participants with the necessary information to prepare for the forthcoming changes. It will list all registered DPEs along with the classes of financial instruments they cover.

- Full Operational Status: The DPE regime will become fully operational on February 3, 2025. From this date, all registered DPEs that are party to a transaction will be required to make the transaction public through an APA. Concurrently, the existing reliance on SIs for transaction publication will cease. This full operational status marks the culmination of the transition period, solidifying the DPEs' role in enhancing market transparency.

Registration of DPEs

Investment firms intending to become Designated Publishing Entities (DPEs) are urged to register with their respective National Competent Authority (NCA). This registration is a critical step for firms to align with the new regulatory framework established by the MiFIR review. The registration process involves several detailed steps designed to ensure comprehensive compliance and seamless integration into the new system.

Detailed Registration Process

- Identification of Financial Instruments: Investment firms must specify the classes of financial instruments they intend to cover as DPEs. This specification is crucial for delineating the scope of their responsibilities and ensuring accurate public reporting of transactions.

- Provision of Legal Entity Identifiers (LEIs): Firms are required to provide LEIs, which serve as unique identifiers for legal entities participating in financial transactions. LEIs ensure that each entity is distinctly identified in the public register, thereby enhancing transparency and traceability.

- Submission of Additional Identifying Information: NCAs may request additional identifying information to complete the registration process. This information can include, but is not limited to, detailed corporate structures, contact details, and regulatory history.

Once the registration details are collated, NCAs will transmit this information to ESMA for inclusion in the public DPE register. This process ensures that all relevant data is captured and accurately reflected in the register, facilitating regulatory oversight and public transparency.

Integration into ESMA’s IT Systems

ESMA is undertaking significant technical efforts to integrate the DPE register into its IT systems. This integration is critical for ensuring that the register is accessible, up-to-date, and user-friendly.

Technical Specifications of Integration

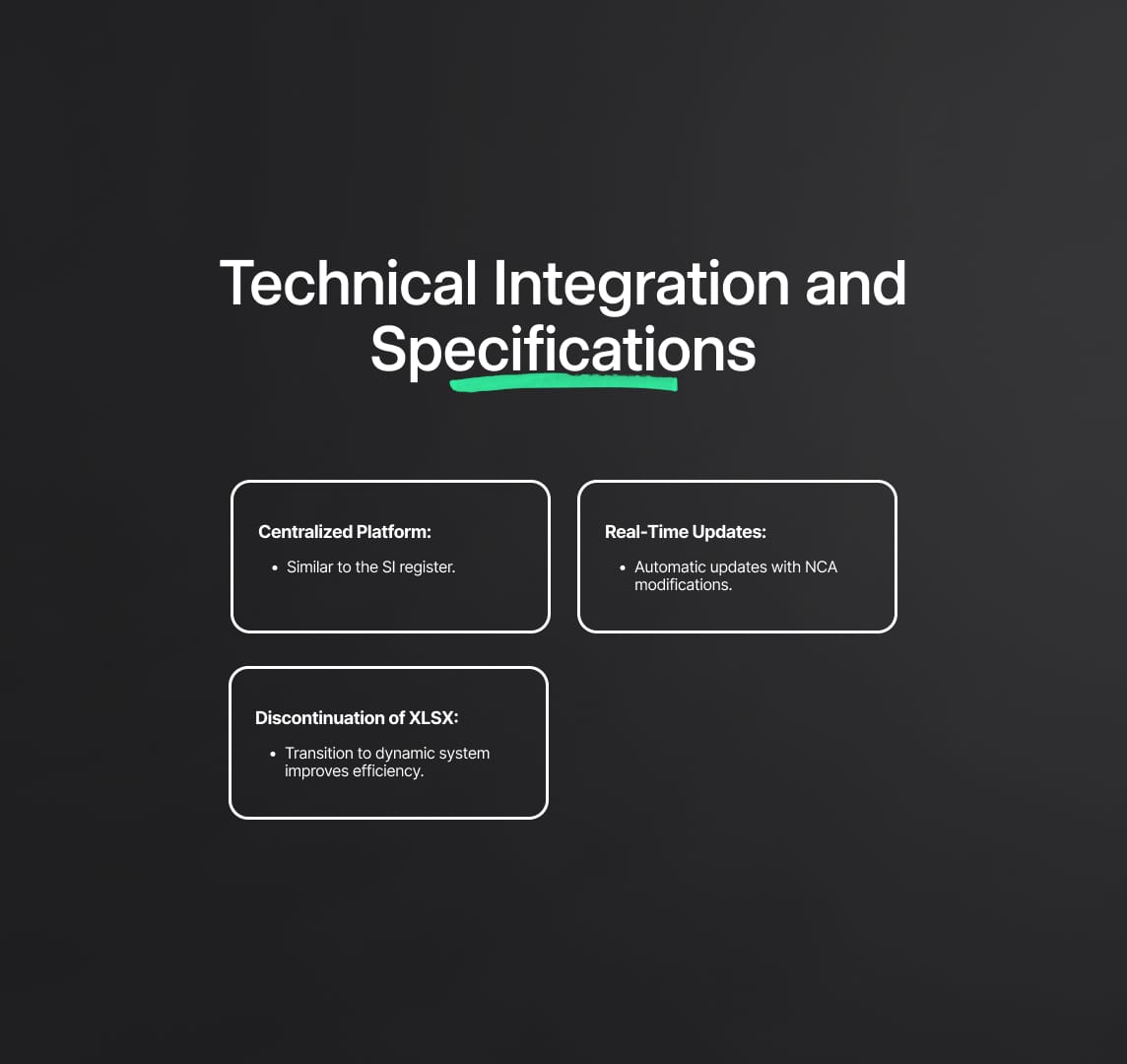

- Dedicated Portal Access: The integrated system will provide access through a dedicated portal, similar to other entity registers (e.g., the Systematic Internalisers (SI) register). This portal will offer a centralized platform for accessing DPE information, thereby simplifying data retrieval and enhancing user experience.

- Automatic Updates: Post-integration, the DPE register will be automatically updated with new information as NCAs introduce modifications. This real-time updating mechanism ensures that the register remains current and accurate, providing reliable data for market participants and regulators.

- Discontinuation of XLSX Format: Once the integrated IT system goes live, expected by the end of 2025, the initial XLSX format of the register will be discontinued. The transition to a fully integrated, dynamic system marks a significant upgrade, improving the efficiency and reliability of the data management process.

Classes of Financial Instruments

The DPE register will cover a broad range of financial instruments, categorised into equity and non-equity instruments. This comprehensive coverage ensures that all relevant transactions are captured, enhancing overall market transparency.

Equity Instruments

- Shares: Common and preferred stocks of publicly traded companies.

- Depositary Receipts: Financial instruments issued by banks to represent a foreign company’s publicly traded securities.

- ETFs (Exchange-Traded Funds): Marketable securities that track an index, commodity, bonds, or a basket of assets.

- Certificates: Financial instruments representing ownership or a claim on assets.

- Other Equity-Like Financial Instruments: Including but not limited to equity warrants and convertible bonds.

Non-Equity Instruments

- Bonds: Debt securities issued by entities to raise capital.

- ETCs (Exchange-Traded Commodities): Securities that track the performance of a commodity index.

- ETNs (Exchange-Traded Notes): Unsecured debt securities that track an underlying index of securities.

- Interest Rate Derivatives: Financial instruments whose value is derived from interest rates.

- Credit Derivatives: Financial instruments used to transfer credit risk from one party to another.

- Structured Finance Products: Securitized financial assets such as asset-backed securities.

- Emission Allowances: Permits allowing the holder to emit a certain amount of carbon dioxide or other greenhouse gases.

Continuation of the Current Regime

In response to stakeholder feedback requesting more time to prepare for the transition, ESMA clarified in its March 27, 2024, statement that the previous regime, relying on SIs, should continue applying until further notice. This decision ensures that market participants have adequate time to adapt to the new requirements and make necessary adjustments to their systems and processes.

Reference Data Reporting Requirements

The rules applicable to reference data reporting and the requirements for DPEs will become effective as soon as the revised Regulatory Technical Standards (RTS 23) start applying. Until then, the existing rules under Level 1 prior to the MiFIR review and the current RTS 23 will continue to apply. The revised RTS 23 will outline specific requirements for DPEs concerning reference data reporting, ensuring that all data is accurately captured and reported in compliance with the new regulatory standards.

Practical Guidance and Compliance

Transparency and Reporting

The transition to the Designated Publishing Entity (DPE) regime represents a significant milestone in enhancing transparency within the over-the-counter (OTC) markets. This regime, introduced under the MiFIR review, centralizes the responsibility of transaction reporting to DPEs, thereby streamlining the reporting process and improving the accuracy of post-trade information. Enhanced transparency is a key objective of the MiFIR review, aimed at fostering greater market integrity and investor confidence through detailed, timely, and accurate transaction reporting.

Centralisation of Reporting Responsibilities

The shift of reporting responsibilities from Systematic Internalisers (SIs) to DPEs is intended to standardize and centralize the post-trade transparency process. By consolidating this function within DPEs, the new regime eliminates inconsistencies and potential discrepancies that may arise from decentralized reporting mechanisms. DPEs, being specialized entities, are expected to adhere to stringent reporting standards, thereby ensuring the reliability and completeness of post-trade data.

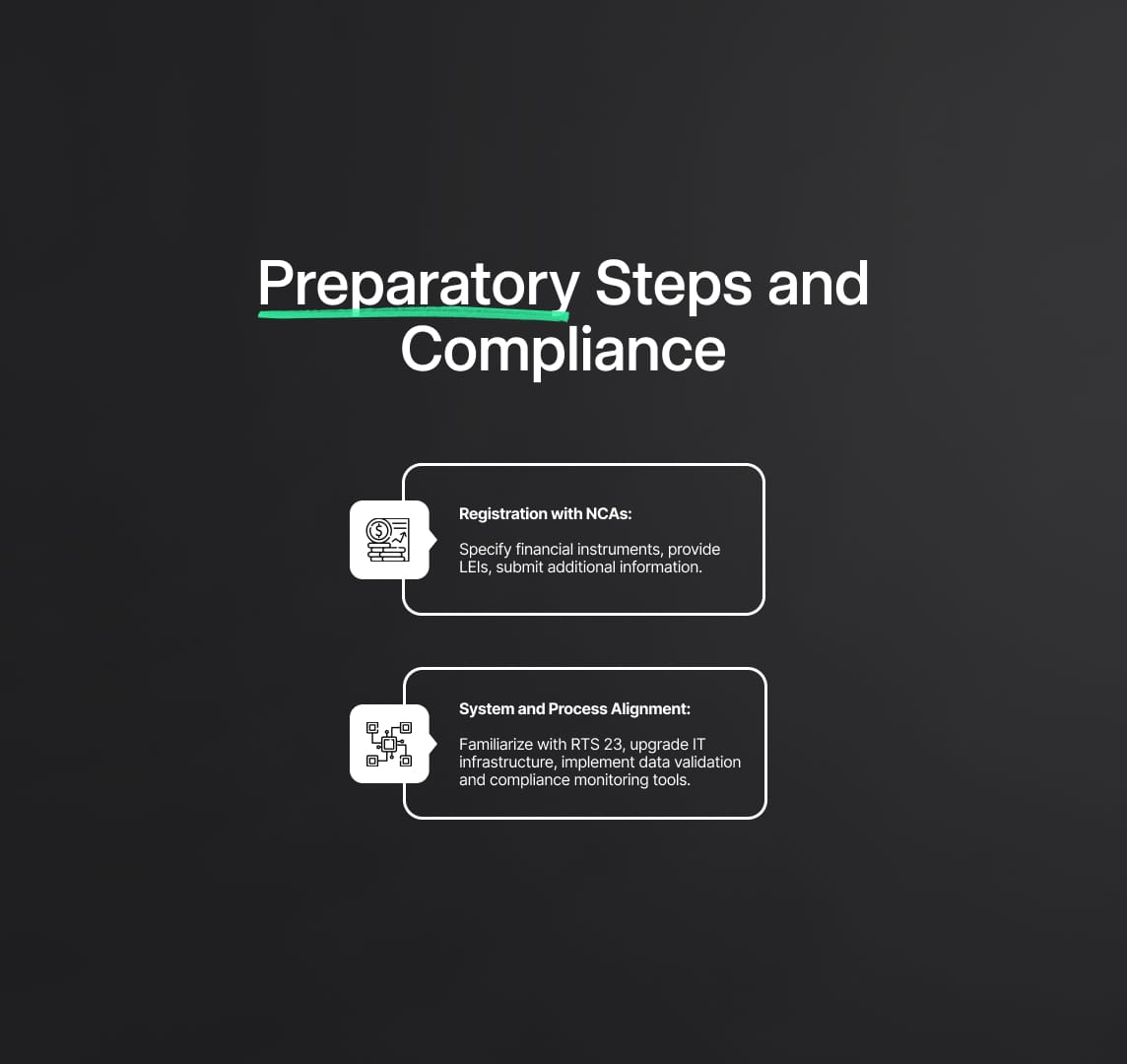

Preparatory Steps for Investment Firms

Investment firms must undertake several critical preparatory steps to align with the new DPE regime. These steps are essential to ensure compliance and seamless integration into the updated regulatory framework.

Registering with NCAs

Investment firms aiming to become DPEs must initiate the registration process with their respective National Competent Authorities (NCAs) promptly. Early registration is crucial as it allows firms to establish their roles and responsibilities under the new regime well ahead of its full implementation. The registration process involves specifying the classes of financial instruments the firm intends to cover, providing Legal Entity Identifiers (LEIs), and submitting additional identifying information as required by the NCAs.

Familiarising with DPE Requirements

Understanding the specific requirements under the revised Regulatory Technical Standards (RTS 23) is paramount for compliance. Firms must familiarise themselves with the detailed reporting obligations, data submission protocols, and compliance timelines outlined in RTS 23. This knowledge is essential for aligning internal processes and systems with the regulatory expectations.

System and Process Alignment

To ensure compliance with the new reporting obligations, firms need to conduct a thorough review and alignment of their systems and processes. This includes upgrading IT infrastructure to support the new reporting formats, integrating real-time data submission capabilities, and implementing robust data validation mechanisms. Ensuring that internal systems can efficiently handle the increased reporting demands and maintain data integrity is critical for smooth compliance.

Impact on IT Systems and Registers

ESMA will continue to assess the IT implications related to reference data and transaction reporting under the new DPE regime. The integration of the DPE register into ESMA’s IT systems is a significant aspect of this transition. This integration aims to enhance the accessibility, reliability, and real-time updating of the register, ensuring that all transaction data is accurately captured and readily available for regulatory oversight.

IT System Upgrades

Firms are advised to invest in comprehensive IT system upgrades to meet the enhanced reporting requirements. These upgrades should include:

- Automated Data Capture and Reporting: Implementing systems capable of automatically capturing transaction data and generating accurate, real-time reports.

- Data Validation and Error Checking: Integrating robust data validation mechanisms to ensure the accuracy and completeness of reported data.

- Compliance Monitoring Tools: Deploying tools to continuously monitor compliance with reporting obligations and promptly address any discrepancies.

Key Dates to Remember

To effectively transition to the new DPE regime, firms must adhere to the following key dates:

- September 29, 2024: Initial publication of the DPE register by ESMA. This publication will provide a comprehensive list of registered DPEs and the classes of financial instruments they cover, allowing firms to benchmark their registration status.

- February 3, 2025: Full operational status of the DPE regime. From this date, DPEs will be responsible for making transactions public through an Approved Publication Arrangement (APA), and the reliance on SIs for transaction publication will cease.

- End of 2025: Integration of the DPE register into ESMA's IT systems and discontinuation of the XLSX version. This marks the transition to a fully integrated, dynamic system that ensures real-time updates and enhanced data accessibility.

Reduce your

compliance risks