EMIR and Third-Country CCPs Fee Adjustments

EMIR ensures a safer derivatives market through strict regulations and CCP oversight. It classifies CCPs into Tier 1 and Tier 2 for tailored regulation. ESMA's fee structure adjustments, based on market impact and stakeholder feedback, promote financial stability and transparency.

The European Securities and Markets Authority (ESMA) recently published a report outlining changes, to the fees for Tier 1 third country Central Counterparties (CCPs) regulated by the European Market Infrastructure Regulation (EMIR). These adjustments are aimed at establishing an proportional fee system for CCPs located outside the European Union. The report explains the updated method, for determining fees, which will primarily consider the level of risk that a CCP presents to the EU sector. Additionally this new approach will factor in the CCPs earnings and the complexity of its operations. By implementing these fee modifications it is anticipated that a risk aware and just fee framework will be fostered for third country CCPs [1][2].

Source

[1]

Alessandro Micagni

Alessandro Micagni

A great regulatory framework designed to improve the transparency, safety and resilience of derivatives markets in Europe is the European Market Infrastructure Regulation (EMIR). There is no better way of explaining this than the fact that these laws are crucial in keeping global financial markets honest and solid. Central Counterparties (CCPs) require a properly organised worldwide monitoring system ensuring their integrity and stability as part of international finance. These non-EU CCPs are called Third-Country CCPs or TC-CCPs.

Core Objectives of EMIR

EMIR’s main aim is to curtail systemic risk and make sure a more secure and open derivatives market. By imposing rigid reporting requirements for risk mitigation strategies, and operational rules that are easily understood, it deals with intricacies and inherent vulnerable positions of the derivatives market, thus ensuring financial stability within EU countries and worldwide.

Oversight of CCPs Under EMIR

Central Counterparties are key players in the financial system, serving as middlemen in the derivatives market and safeguarding against default risks to facilitate trade. EMIR regulations aim to strengthen the operational resilience, risk management, and transparency of these crucial entities.

Classification of CCPs: Tier 1 and Tier 2

CCPs under EMIR are carefully categorized as Tier 1 or Tier 2 based on a thorough evaluation of their systemic importance and risk profile in relation to the EU financial system.

- Tier 1 CCPs are classified as entities with reduced systemic risk, subject to a regulatory framework that recognizes their lower risk level. This enables a simplified oversight process that is suitable given the level of risk involved.

- Tier 2 CCPs are considered to possess greater systemic importance and, as a result, a more substantial risk profile. The regulatory standards for Tier 2 CCPs are stricter, reflecting their potential influence on the EU's financial stability. This hierarchical system enables more customized regulatory supervision to address the individual risks presented by each CCP effectively.

The Importance of EMIR in Global Finance

EMIR categorizes TC-CCPs into Tier 1 and Tier 2 to improve regulatory oversight and promote consistent risk management globally. This system ensures appropriate scrutiny based on risk levels, supporting financial market stability. ESMA monitors and regulates TC-CCPs to bolster the EU's financial markets, implementing fees for oversight and reducing systemic risks. ESMA's recent fee changes for Tier 1 CCPs aim to create a fairer regulatory environment, reflecting detailed considerations for TC-CCPs and the wider financial sector.

European Market Infrastructure Regulation: Fee Structure for Tier 1 TC-CCPs

ESMA's suggested changes to the fee system aim to align fees more accurately with the size and systemic risk profile of Tier 1 CCPs, resulting in a fairer distribution of regulatory costs reflective of their market presence. The proposed improvements include various key features.

- Framework for Annual Fee Range: It sets limits on annual fees to avoid extremely low or high payments by any TC-CCP. The goal is to make sure all CCPs, regardless of their size or earnings, contribute fairly to regulatory expenses.

- Weighted Turnover Model: The proposed changes include implementing a model to calculate annual fees based on the global turnover of each Tier 1 CCP, ensuring fees align with market impact and transaction volumes to cover regulatory oversight costs. Global turnover is chosen to accurately reflect activity level and systemic relevance.

- Classification into Three Revenue Groups: ESMA suggests categorizing Tier 1 CCPs into three revenue groups based on global clearing revenues. Each group has a designated weighting factor for calculating annual fees, promoting fairness and competitiveness. This system recognizes varying CCP sizes and capabilities, adjusting regulatory costs accordingly.

ESMA's proposed stratification and weighted turnover model show its commitment to a regulatory framework that is comprehensive, adaptive, fair, and in line with the current dynamics of global financial markets. These changes aim to balance TC-CCPs' operational realities with the EU's need for strong financial oversight, ensuring that the fee structure supports financial system development and guards against systemic risks. These modifications align TC-CCPs' financial contributions with their market presence and systemic importance, reflecting the EU's dedication to a stable, transparent, and efficient financial market framework that evolves alongside the markets it oversees. The focus on creating a balanced fee structure is part of the EU's strategy to keep its financial markets resilient, competitive, and able to meet the challenges of global finance.

ESMA has made significant efforts to improve regulatory fees for TC-CCPs, considering stakeholder input and diverse market participants. These changes show a thorough understanding of challenges faced by CCPs.

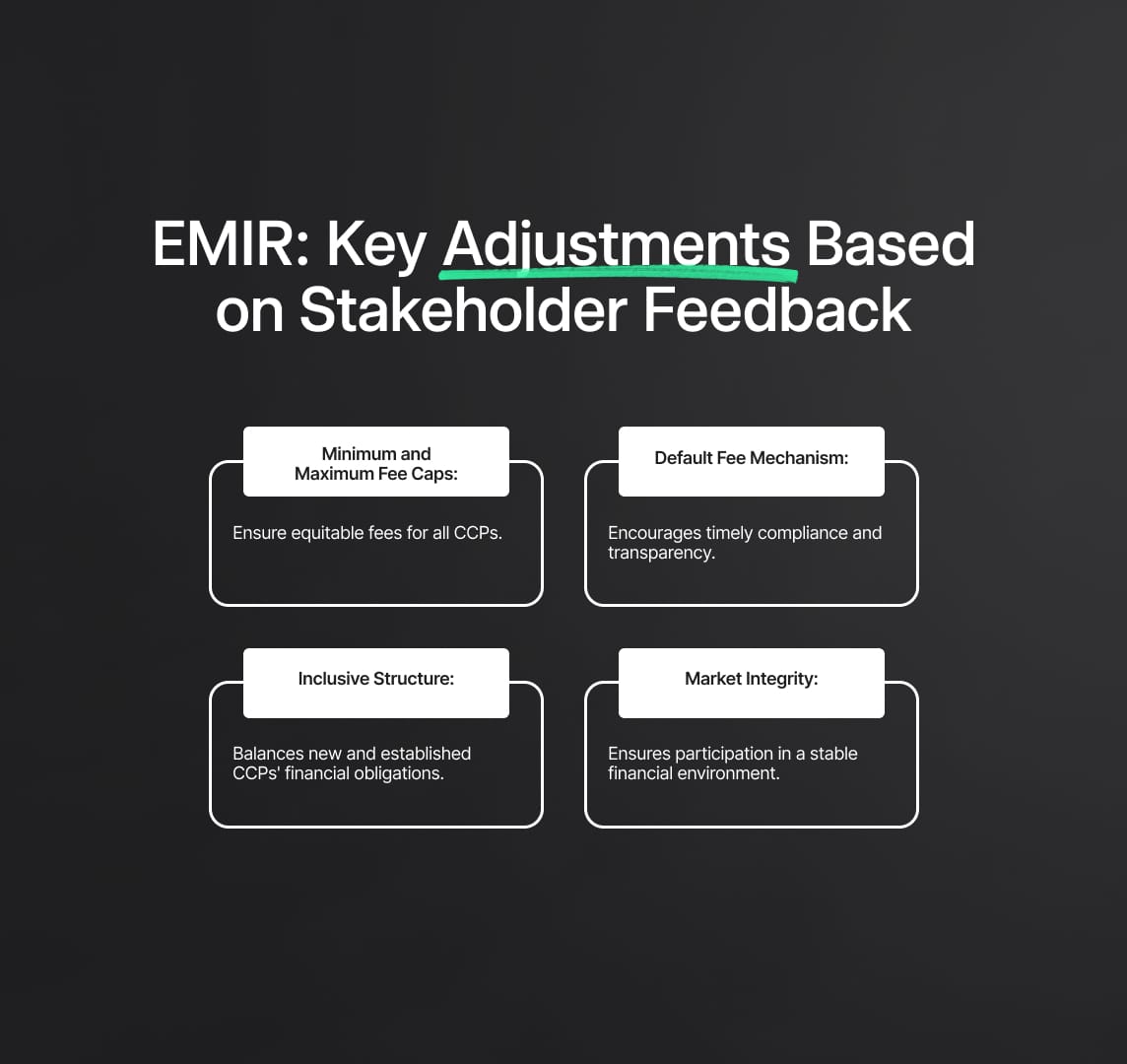

EMIR: Key Adjustments Based on Stakeholder Feedback

- Introduction of a Minimum and Maximum Fee Cap:

- Minimum Annual Fee for Group 1 CCPs: The minimum annual fee for Group 1 CCPs is EUR 40,000. This change addresses worries regarding the high financial burden on smaller or newer CCPs. ESMA is reducing the fee to make sure that smaller organisations can still join the market despite financial limitations.

- Maximum Fee Cap for Group 3 CCPs: The Maximum Fee Cap for Group 3 CCPs is set at EUR 250,000 to avoid excessively high fees for the biggest CCPs, keeping their contribution significant but manageable. This strategic cap maintains an equitable and sustainable fee system for all sizes and revenues of CCPs.

Default Fee Mechanism for Encouraging Compliance:

- A new default fee system has been implemented to motivate timely submission of audited turnover data. It is a practical method to promote compliance, urging CCPs to meet reporting deadlines and uphold transparency in financial activities.

European Market Infrastructure Regulation Strategic Considerations

- Inclusive and Balanced Fee Structure: The updated fee structure aims to be fair and equitable, allowing new CCPs to meet regulatory standards while also taking into account the financial obligations of established CCPs to avoid hindering their operations.

- Promoting Timely Adherence: The default fee mechanism serves as a strategic instrument emphasizing the significance of prompt and precise financial reporting. It not only enables efficient regulatory monitoring but also fosters a culture of transparency and accountability among the CCP community.

- Adapting to Stakeholder Feedback: ESMA's willingness to change fee structure based on stakeholder feedback shows a responsive and flexible regulatory philosophy. This boosts credibility and encourages collaboration between regulators and market players.

- Ensuring Market Integrity: ESMA aims to protect the integrity of financial markets it supervises by improving the fee system. The changes guarantee that all CCPs, no matter their scale, can participate in and gain from a steady, open, and strong financial environment.

The development of regulations for Tier 1 Third-Country Central Counterparties (TC-CCPs) under EMIR involved collaboration between ESMA and market participants, leading to varied opinions on fee structures, specifically the use of global turnover for differentiation. Feedback has influenced ESMA's efforts to create a fair and efficient regulatory system for TC-CCPs.

Moving Forward with a Balanced Regulatory Framework: EMIR

- Stakeholder Concerns on Fee Differentiation Basis:

- During the consultation, stakeholders expressed worries about using global turnover as the main factor for fee differences. They indicated a preference for a more detailed approach considering EU activities and direct monitoring costs by ESMA.

- ESMA's Rationale for Global Turnover Method:

- ESMA has upheld the use of global turnover for fee allocation, citing the need to address diverse accounting practices among third-country CCPs and allow flexibility in reporting audited revenue figures, ensuring the fee structure is responsive to operational differences.

- Adaptability to Diverse Accounting Practices: Recognising the different accounting standards and practices in TC-CCPs worldwide, the global turnover method provides a standardised criterion that promotes fairness and consistency in fee structures.

- Flexibility in Financial Reporting: ESMA promotes a regulatory environment that is both strict and flexible by allowing for flexibility in submitting audited revenue figures, demonstrating a dedication to practical regulatory oversight.

- Proportionate Fee Allocation: Proportional allocation of fees: Using worldwide revenue to differentiate fees ensures that fees charged to TC-CCPs are appropriate for their size and influence in the market, thereby upholding the principle of proportionality.

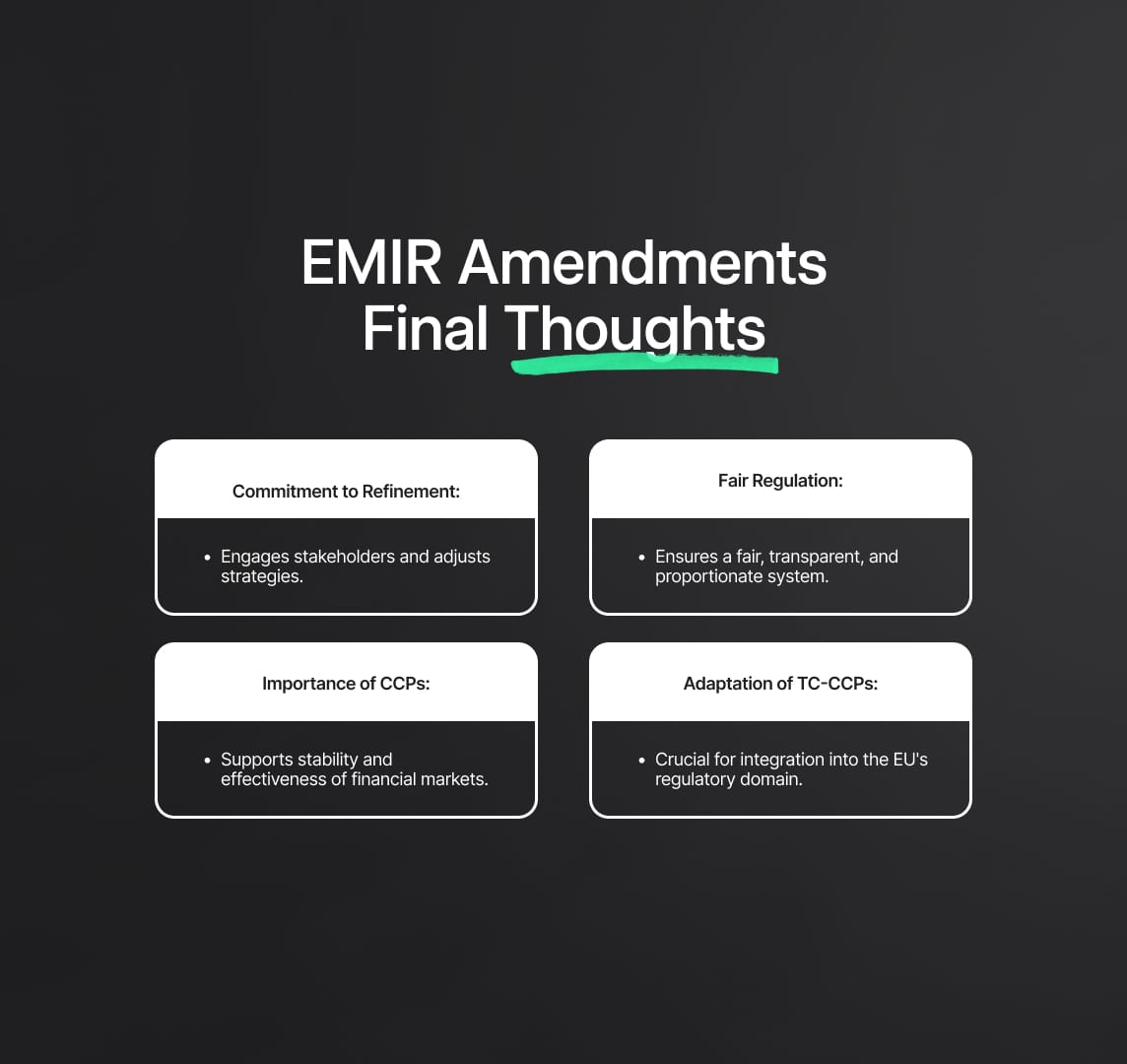

EMIR Amendments Final Thoughts

- Commitment to Refinement: ESMA's strong dedication to improving the regulatory framework for Tier 1 TC-CCPs is shown through actively engaging with stakeholders and being willing to adjust strategies in response to feedback. This dedication enhances the regulatory environment and maintains its relevance and effectiveness in the ever-changing global finance landscape.

- Fair, Transparent, and Proportionate Regulation: ESMA seeks to create a regulatory system that is fair, transparent, and proportionate to enable CCPs to operate effectively and support the stability and integrity of the EU's financial markets.

- Importance of CCPs: The effort emphasizes the crucial role of CCPs in supporting the stability and effectiveness of financial markets, demonstrating the EU's dedication to maintaining a strong financial environment amidst worldwide challenges.

- Importance of TC-CCPs' Adaptation: Adaptation of TC-CCPs is crucial for recognition under EMIR, as understanding the refined fee structure is vital. Seamless integration into the EU's regulatory domain is key to improving the integrity and stability of the global financial market.

Reduce your

compliance risks