ESRB Compliance Report

The European Systemic Risk Board (ESRB) ensures EU financial stability by monitoring systemic risks and guiding countercyclical buffer rates (CCyB). Its functions include risk assessment, setting buffer rates, continuous monitoring, and coordinating with national authorities.

The European Systemic Risk Board (ESRB) is a cornerstone in the framework of financial stability within the European Union. Established to monitor and mitigate systemic risks, the ESRB plays a critical role in safeguarding the financial system against potential crises. One of its primary functions is to provide detailed guidance on setting countercyclical buffer rates (CCyB), a macro-prudential policy tool designed to enhance the resilience of financial institutions during periods of economic fluctuation.

ESRB Compliance Report: Technical Aspects of Countercyclical Buffer Rates (CCyB)

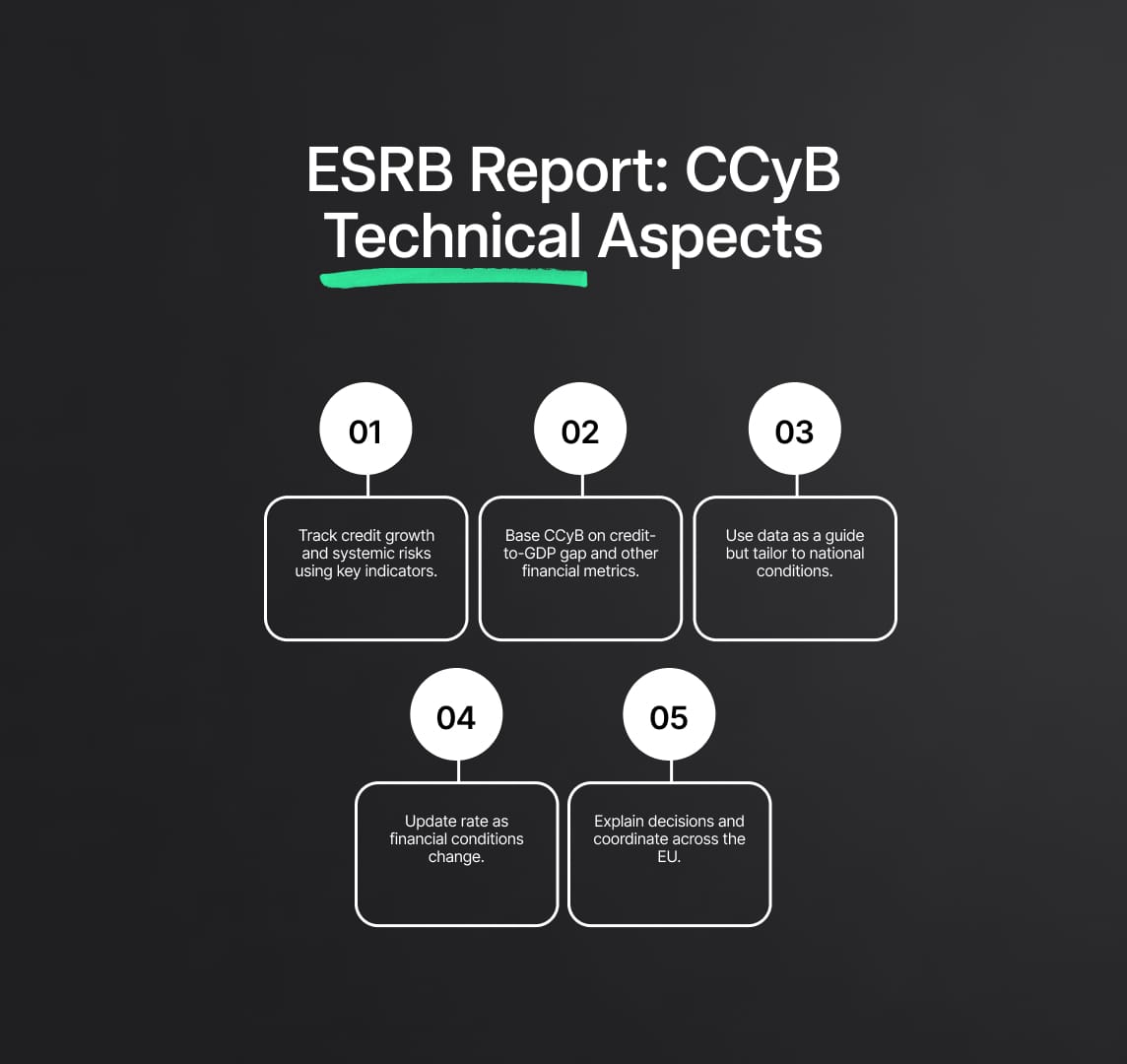

The technical implementation of countercyclical buffer rates (CCyB) is a complex process that requires meticulous assessment and periodic recalibration. The ESRB provides a structured framework for national authorities and the European Central Bank (ECB) to follow, ensuring consistency and efficacy across the EU. The primary components of this framework include:

- Risk Assessment and Identification: National authorities are tasked with continuously monitoring the financial environment to identify periods of excessive credit growth and emerging systemic risks. This involves analyzing a wide range of economic indicators, including the credit-to-GDP gap, property price trends, and sectoral imbalances.

- Setting the Buffer Rate: Based on the risk assessment, authorities determine an appropriate CCyB rate. The credit-to-GDP gap, which measures the deviation of the credit-to-GDP ratio from its long-term trend, serves as the primary indicator. However, authorities must also consider supplementary data, such as market liquidity, bank leverage ratios, and potential overvaluation in asset markets.

- Buffer Guide and Discretionary Judgment: The ESRB emphasizes a guided discretion approach, where the credit-to-GDP gap serves as a reference point, but authorities exercise judgment in setting the buffer rate. This ensures that the buffer rate accurately reflects the specific economic conditions and systemic risks of each member state.

- Monitoring and Adjustment: Once the buffer rate is set, continuous monitoring is essential. Authorities must adjust the rate in response to changes in the financial environment, ensuring that the CCyB remains effective in mitigating systemic risks. This dynamic adjustment process is crucial for maintaining financial stability.

- Communication and Coordination: Effective communication strategies are vital for ESRB compliance. Authorities must transparently communicate their decisions and the rationale behind setting or adjusting the CCyB rate. Coordination with other national authorities and the ESRB ensures a unified approach across the EU, enhancing the overall effectiveness of macro-prudential policies.

ESRB Recommendation on Guidance for Setting Countercyclical Buffer Rates

Background and Objectives

On 18 June 2014, the European Systemic Risk Board (ESRB) issued Recommendation ESRB/2014/1, which provides comprehensive guidance for setting countercyclical buffer rates (CCyB) under the Capital Requirements Directive (CRD) IV. The primary objective of this recommendation is to mitigate the pro-cyclical amplification of financial shocks within the banking system and financial markets. By establishing additional capital buffers during periods of excessive credit growth, these measures are designed to enhance the banking sector's resilience during economic downturns, thereby maintaining the continuous flow of credit to the real economy.

Objectives of the CCyB

The main goal of the CCyB is to ensure that banks maintain additional capital buffers during periods of excessive credit growth. These buffers can be released during periods of economic stress to absorb losses and sustain the flow of credit to the real economy. The CCyB can function independently or in conjunction with other macro-prudential instruments to strengthen financial stability.

Detailed Policy Objectives of the ESRB Recommendation

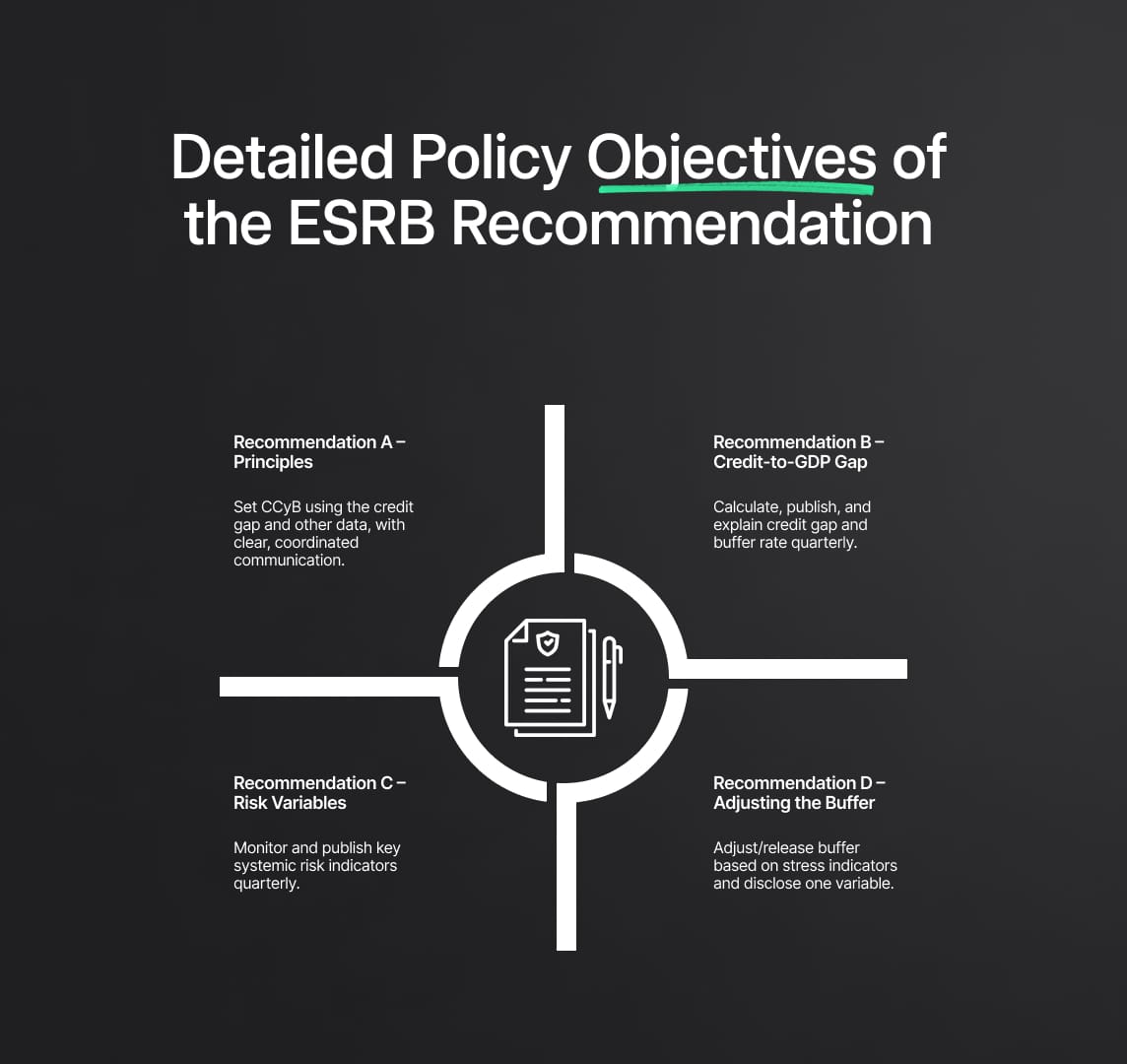

Recommendation A – Principles

Recommendation A comprises seven sub-recommendations that establish the foundational principles for designated authorities in assessing and setting CCyB rates.

- Objective: The primary aim is to shield the banking system from losses associated with the build-up of cyclical systemic risk. This is crucial for ensuring the sustainable provision of credit to the real economy throughout the financial cycle.

- Buffer Guide: The credit-to-GDP gap, defined as the deviation of the credit-to-GDP ratio from its long-term trend, should serve as the standard reference point for setting CCyB rates. However, authorities must also consider other quantitative and qualitative data, including country-specific features, and publicly explain the relevance of this information in their decision-making process.

- Risk of Misleading Information: Authorities must critically assess the data within the credit-to-GDP gap and other relevant variables to ensure that no misleading information distorts their judgment regarding the sustainability of credit growth and the appropriate CCyB rate. The periodic reassessment of these variables and models is recommended to maintain their accuracy and relevance.

- Release of the Buffer: The timely release of the buffer is advised if risks do not materialize or have receded. This release can help credit institutions continue lending and meet solvency requirements while absorbing potential losses. A gradual release may be more suitable if risks have lessened progressively.

- Communication: Authorities should develop a robust communication strategy for their decisions regarding the CCyB. This strategy should encompass mechanisms for coordination with other designated authorities and the ESRB, as well as clear processes and channels for communicating with key stakeholders and the public.

- Recognition of Buffer Rates: Recognition of CCyB rates set by other member states should generally be the norm, beyond the mandatory reciprocity arrangements. If an authority chooses not to recognize a buffer rate, it must assess the cross-border implications and notify the ESRB, the designated authority that set the buffer rate, and the ECB if applicable.

- Other Macro-prudential Instruments: Authorities should evaluate the use of the CCyB in isolation, alongside other macro-prudential instruments, or in combination with these instruments as part of a comprehensive macro-prudential strategy.

Recommendation B – Guidance on Measurement and Calculation of the Credit-to-GDP Gap

Recommendation B focuses on the precise methodology for measuring and calculating the credit-to-GDP gap, determining the benchmark buffer rate, and selecting the appropriate buffer guide. Compliance with Recommendation B entails a thorough examination of the methodologies applied by designated authorities.

- Standardized Credit-to-GDP Gap: Authorities are instructed to measure and calculate a standardized credit-to-GDP gap quarterly, adhering to BCBS guidance specified in Part I of the Annex to the Recommendation.

- Additional Credit-to-GDP Gap: Recognizing national economic differences, authorities may use a complementary method that reflects the deviation of the credit-to-GDP ratio from its long-term trend. This alternative method should be based on empirical analysis relevant to the member state and should be revised periodically.

- Benchmark Buffer Rate Calculation: Authorities are encouraged to calculate a benchmark buffer rate quarterly based on the standardized credit-to-GDP gap and may also use alternative methodologies if appropriate.

- Buffer Guide Selection: In selecting a buffer guide, authorities should choose the benchmark buffer rate that best reflects the specific economic conditions of their country.

- Publication Requirements: The announcement of the CCyB rate, as mandated by Article 136(7) of the CRD IV, should include detailed information such as the standardized credit-to-GDP gap, any additional credit-to-GDP gap, benchmark buffer rates, and the sources of underlying data. This information must be published quarterly on the authorities' websites.

- Explanation of Deviations: Authorities should provide clear explanations for any deviations from the standard methodologies for measuring the credit-to-GDP gap, calculating the benchmark buffer rate, or selecting the buffer guide in their CCyB rate announcements.

Recommendation C – Variables Indicating System-Wide Risk

Recommendation C outlines the importance of monitoring a comprehensive range of quantitative and qualitative information to detect the build-up of system-wide risk associated with excessive credit growth.

- Quantitative and Qualitative Information: Authorities should consider various data points, in addition to the credit-to-GDP gap, to confirm the presence of systemic risk. These include measures of property price overvaluation, credit developments, external imbalances, bank balance sheet strength, private sector debt burden, and potential mispricing of risk.

- Monitoring Variables: Authorities must regularly monitor these variables to maintain an accurate understanding of the financial environment and to make informed decisions regarding the CCyB rate.

- Publication Requirements: Authorities are required to publish at least one measure from each group of variables quarterly on their website, alongside the CCyB rate announcement, to ensure transparency and public awareness.

Recommendation D – Variables for Maintaining, Reducing, or Releasing the Buffer

Recommendation D focuses on the variables that should be considered when deciding whether to maintain, reduce, or fully release the CCyB.

- Quantitative and Qualitative Information: Authorities must evaluate a comprehensive range of information to determine the appropriate CCyB rate and whether the buffer should be maintained, reduced, or released.

- Monitoring Variables: Authorities should monitor indicators of stress in bank funding markets and general systemic stress to inform their decisions.

- Judgment in Monitoring: Authorities should exercise significant judgment in interpreting these variables to make accurate decisions about the buffer rate.

- Publication Requirements: Authorities are required to publish at least one of the variables mentioned in their quarterly CCyB rate announcement to maintain transparency.

ESRB Compliance: Standardised Credit-to-GDP Gap

Designated authorities are required to measure and calculate a standardized credit-to-GDP gap on a quarterly basis. This measurement must adhere to the Basel Committee on Banking Supervision (BCBS) guidance, as detailed in Part I of the Annex to the Recommendation. The standardized credit-to-GDP gap serves as a foundational metric for assessing the level of systemic risk in the financial system. By comparing the current credit-to-GDP ratio with its long-term trend, authorities can identify periods of excessive credit growth that may warrant the implementation of countercyclical buffers.

Key steps for calculating the standardized credit-to-GDP gap include:

- Data Collection: Gather comprehensive data on credit levels and GDP for the relevant period.

- Trend Estimation: Estimate the long-term trend of the credit-to-GDP ratio using statistical techniques such as the Hodrick-Prescott filter or other appropriate methods.

- Deviation Calculation: Calculate the deviation of the current credit-to-GDP ratio from its long-term trend to identify the gap.

- Quarterly Updates: Ensure that the credit-to-GDP gap is updated quarterly to reflect the most current economic conditions.

Additional Credit-to-GDP Gap

Recognising the unique economic contexts of different member states, Recommendation B allows for the use of complementary measurement and calculation methods tailored to national circumstances. Authorities may calculate an additional credit-to-GDP gap that better reflects the specificities of their economies. This alternative method should be:

- Empirically Based: Developed through rigorous empirical analysis of national economic data.

- Periodically Revised: Regularly reviewed and updated to ensure its accuracy and relevance.

- Consistently Measured: Calculated on a quarterly basis, similar to the standardized gap, to maintain consistency in monitoring and reporting.

Benchmark Buffer Rate Calculation

Authorities are encouraged to calculate a benchmark buffer rate quarterly based on the standardized credit-to-GDP gap, in accordance with BCBS guidance. Additionally, they may calculate an alternative benchmark buffer rate using different methodologies if such approaches better capture national economic conditions. The benchmark buffer rate provides a quantitative basis for setting the CCyB and helps ensure that decisions are grounded in systematic and transparent analysis.

Steps for benchmark buffer rate calculation include:

- Determine Baseline Rate: Use the standardized credit-to-GDP gap to calculate a baseline buffer rate.

- Alternative Methods: Where appropriate, apply alternative calculation methods to derive a supplementary buffer rate.

- Comparison and Selection: Compare the standardized and alternative rates to select the one that best aligns with national economic indicators and policy objectives.

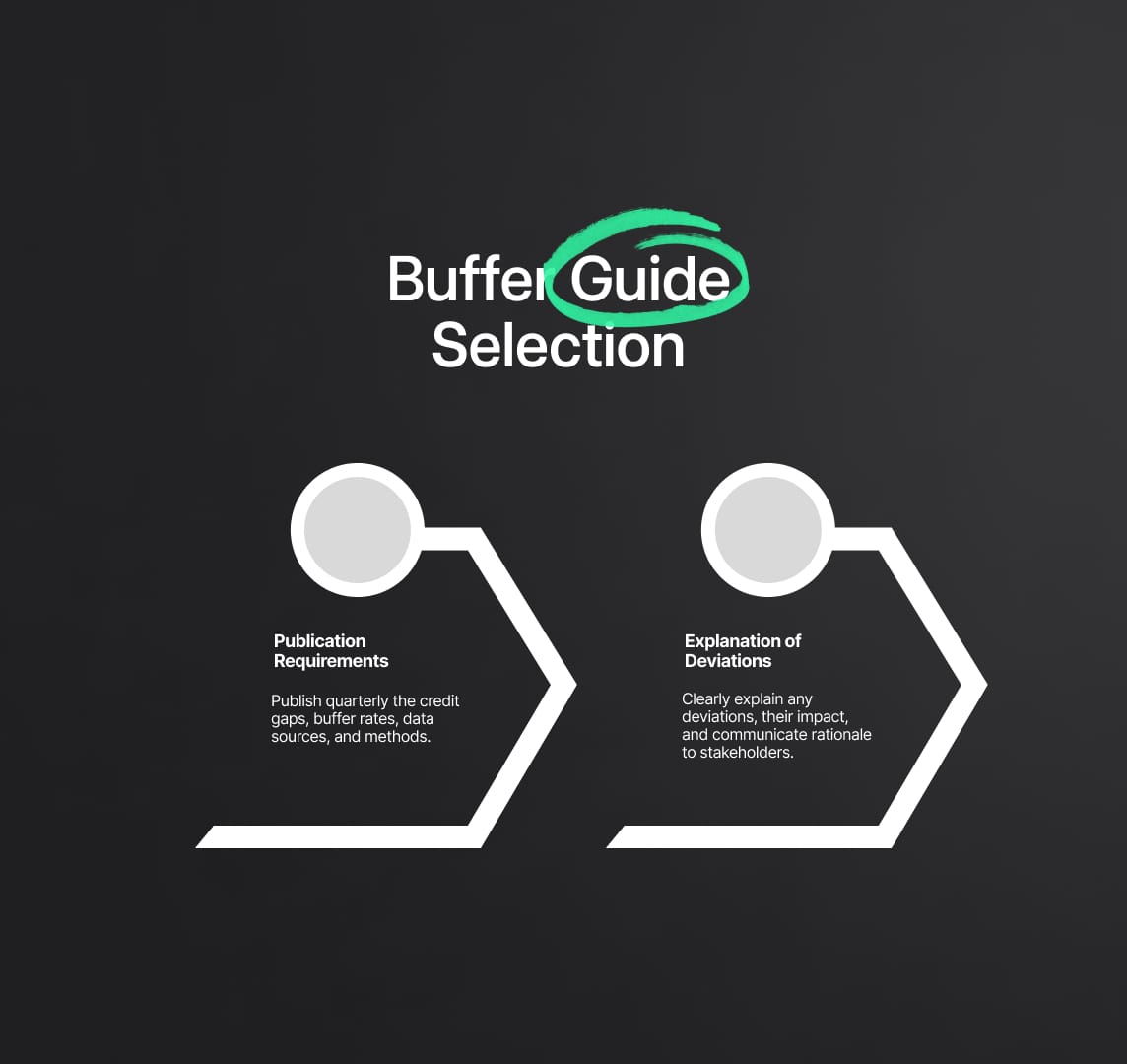

Buffer Guide Selection

When selecting the buffer guide, authorities must choose the benchmark buffer rate that most accurately reflects the unique features of their national economy. This selection process should consider various economic indicators and contextual factors to ensure that the chosen buffer rate effectively mitigates systemic risks.

Publication Requirements

To promote transparency and accountability, authorities must publish detailed information regarding the CCyB rate and its underlying calculations on a quarterly basis. This includes:

- Standardized Credit-to-GDP Gap: The calculated gap and its corresponding ratio.

- Additional Credit-to-GDP Gap: If used, the calculated gap, its ratio, and justification for any deviations from standardized methods.

- Benchmark Buffer Rates: Both standardized and alternative rates, where applicable.

- Data Sources: Information on the data sources and methodologies used in the calculations.

Explanation of Deviations

In cases where authorities deviate from the standard methodologies or selected buffer rates, they must provide clear explanations for these deviations. This ensures that stakeholders understand the rationale behind the decisions and that the process remains transparent and justifiable.

Key points to address in explanations include:

- Reasons for Deviation: Justification for choosing an alternative measurement or buffer rate.

- Impact Analysis: Assessment of how the deviation affects the overall risk assessment and buffer determination.

- Stakeholder Communication: Transparent communication with stakeholders regarding the changes and their implications.

ESRB Compliance Assessment Methodology

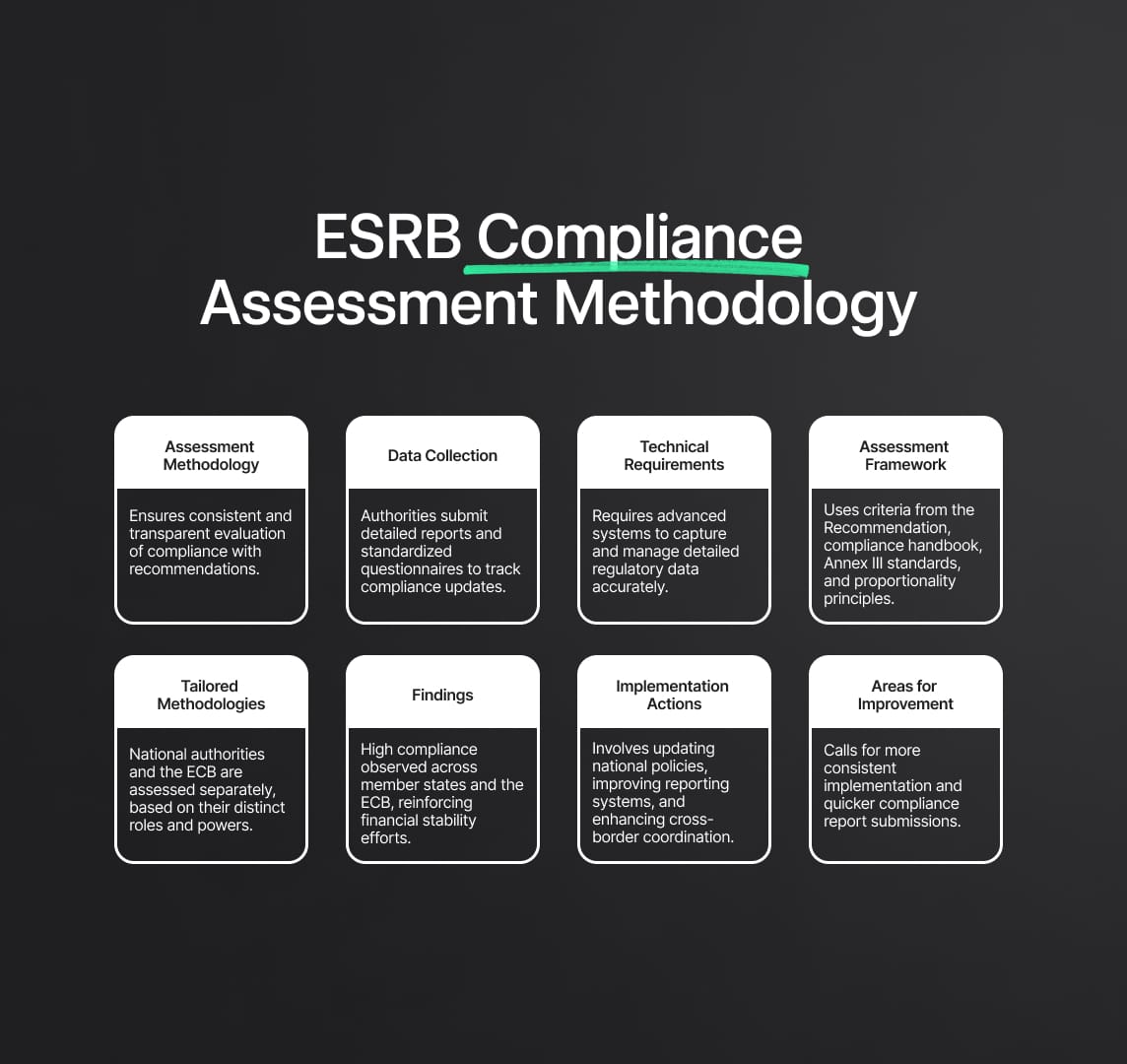

The ESRB's compliance assessment methodology is a cornerstone for ensuring ESRB compliance, reflecting a meticulous and structured approach to evaluating the adherence of designated authorities and the European Central Bank (ECB) to ESRB recommendations. This rigorous methodology follows established guidelines to ensure accuracy, consistency, and transparency in the assessment process.

Data Collection and Reporting

Designated authorities are required to submit detailed reports to the ESRB Secretariat, outlining any substantial changes since the last reporting round. This step is crucial for maintaining up-to-date records of compliance and for identifying any emerging risks or deviations from established guidelines. The data collection process involves:

- Detailed Reports: Authorities must provide comprehensive documentation of their compliance activities, including explanations of any significant changes or new measures implemented.

- Standardized Follow-Up Questionnaire: To streamline the reporting process and ensure uniformity, a standardized follow-up questionnaire template is used. This template helps in collecting consistent and comparable data across different jurisdictions.

Technical Detail: Authorities need to ensure their reporting systems are capable of capturing detailed compliance data. This often involves sophisticated data management systems that can handle large volumes of regulatory data, ensuring accuracy and timeliness in reporting.

ESRB Assessment Framework

The assessment is carried out by an Assessment Team established under the ESRB Advisory Technical Committee (ATC). This team follows a comprehensive framework designed to evaluate compliance against specific criteria, ensuring a thorough and objective assessment process. The framework includes:

- Criteria from Section 2(2) of the Recommendation: These criteria outline the fundamental requirements for compliance, including the principles and guidelines that authorities must adhere to.

- Handbook on the Assessment of Compliance: This handbook provides detailed guidance on the assessment process, including the methodologies and tools used to evaluate compliance.

- Implementation Standards Detailed in Annex III: These standards offer a more granular view of the specific actions and measures that authorities need to implement to achieve compliance.

- Principle of Proportionality: This principle ensures that the compliance requirements and assessment methodologies are proportional to the size and complexity of the financial institutions and markets within each jurisdiction.

Separate Assessment Methodologies

The report delineates different methodologies for assessing national designated authorities and the ECB, recognizing the unique roles and powers of these entities. This tailored approach ensures that the specific responsibilities and regulatory environments of each authority are appropriately considered.

- National Designated Authorities: Assessed based on their implementation of the ESRB recommendations within their jurisdictions. This involves evaluating their policies, procedures, and reporting mechanisms.

- European Central Bank: Assessed separately due to its unique role and top-up powers, which allow it to impose higher CCyB rates than national authorities but not to reduce them. The ECB's compliance is evaluated in the context of its broader supervisory and regulatory responsibilities.

Findings of the ESRB Compliance Assessment

The compliance assessment revealed a high level of adherence to the ESRB's Recommendation across member states and the ECB. This high compliance level highlights the commitment of national authorities and the ECB to enhancing financial stability through prudent macro-prudential policies.

Implementation Actions

To achieve and maintain high compliance levels, several key actions have been taken by member states and the ECB:

- Policy Establishment: Many countries have revised and established national policies to incorporate the ESRB's guidance. This often involves legislative changes and the development of new regulatory frameworks.

- Monitoring and Reporting Enhancements: Authorities have improved their mechanisms for monitoring and reporting the effectiveness of implemented measures. This includes adopting advanced data analytics and reporting tools.

- Increased Coordination: Enhanced cooperation among national authorities and the ECB has been a significant factor in achieving high compliance levels. This coordination helps in sharing best practices and addressing cross-border financial stability issues.

Technical Detail: Implementation actions often require significant investments in regulatory infrastructure and capabilities. This includes the development of sophisticated data collection and analysis systems, as well as the training of regulatory personnel.

Areas for Improvement

Despite the high compliance levels, the report identifies areas needing improvement:

- Consistency in Implementation: Ensuring more consistent application of the ESRB's recommendations across different sectors remains a challenge. Authorities are encouraged to harmonize their approaches to ensure uniform compliance.

- Timeliness of Submissions: Faster submission of compliance reports to the ESRB Secretariat is necessary for more effective monitoring and timely intervention if needed.

ESRB Compliance: Assessment of the European Central Bank (ECB)

The ECB’s macro-prudential mandate, derived from the CRD IV and the SSM Regulation, allows it to impose higher CCyB rates than national authorities but not to reduce them. This unique role requires a tailored assessment approach.

Compliance Evaluation:

- Full Compliance in Recommendations A, B, and C: The ECB has fully integrated the ESRB’s principles and methodologies into its macro-prudential policies.

- Non-Applicability of Recommendation D: Due to its specific remit, Recommendation D does not apply to the ECB.

Technical Detail: The ECB employs a range of macro-prudential tools and analytical frameworks to assess systemic risks and set appropriate buffer rates, ensuring a cohesive and effective approach to financial stability across the euro area.

Key Findings and Changes Since the Previous ESRB Compliance Assessment

Stability in Compliance

The stability in compliance grades is a testament to the effectiveness of the ESRB's macro-prudential policies and the robust implementation of its recommendations across the European Union. This consistency underscores the dedication of member states to uphold financial stability and mitigate systemic risks through adherence to ESRB compliance guidelines.

- Consistency Across Jurisdictions: The uniformity in compliance grades across various jurisdictions highlights the success of the ESRB's standardized approach. This uniformity ensures that financial institutions across the EU are operating under similar regulatory standards, thereby reducing systemic risk.

- Enhanced Monitoring Frameworks: The deployment of advanced monitoring frameworks and tools has played a critical role in maintaining stability in compliance. These tools enable authorities to detect and respond to potential risks proactively.

Improvements and Deficiencies

The assessment revealed notable improvements in compliance with Recommendation A, particularly in sub-recommendation A(4), which pertains to the prompt release of buffers. This improvement is largely attributed to actions taken during the COVID-19 pandemic, demonstrating the flexibility and responsiveness of the ESRB’s framework in crisis situations.

- Enhanced Buffer Release Mechanisms: The pandemic prompted the development and implementation of more effective buffer release mechanisms, allowing financial institutions to absorb shocks and maintain credit flow to the real economy.

- Deficiencies in Information Publication: Despite these improvements, there were deficiencies in sub-recommendation B(5) and C(3), particularly concerning the publication of comprehensive information. These deficiencies highlight the need for enhanced transparency and communication strategies to ensure that all relevant data is accessible to stakeholders.

Recommendations for Improvement:

- Enhanced Data Transparency: Authorities should focus on improving the transparency and comprehensiveness of published data, particularly regarding the credit-to-GDP gap and systemic risk indicators.

- Regular Updates and Reviews: Regular reviews and updates of the methodologies used for data collection and publication can ensure that they remain relevant and effective in capturing the current economic conditions.

Adoption of Positive Neutral CCyB Rate

A significant development since the first assessment is the adoption of a "positive neutral CCyB" rate by several addressees. This proactive approach is designed to maintain higher releasable capital buffers throughout the economic cycle, thereby enhancing the resilience of the banking sector.

- Forward-Looking Buffer Management: The positive neutral CCyB rate reflects a forward-looking approach, ensuring that banks are better prepared to absorb losses during economic downturns. This strategy is aligned with the ESRB's 2022 review, which recommended a more anticipatory build-up of CCyBs.

- Higher Capital Buffers: By maintaining higher capital buffers, banks can sustain lending even during periods of financial stress, thereby supporting economic stability and growth.

Implementation Strategies:

- Gradual Buffer Accumulation: Authorities are encouraged to gradually accumulate CCyBs during periods of economic growth, ensuring a smooth transition to higher buffer levels without disrupting financial markets.

- Dynamic Adjustment Mechanisms: Implementing dynamic adjustment mechanisms allows for timely changes to buffer rates in response to evolving economic conditions, enhancing the effectiveness of the CCyB framework.

Reduce your

compliance risks