How do firms manage the KYC of intermediaries?

In the rapidly evolving regulatory landscape, companies are not only expected to know their customers (KYC), but also their business intermediaries. This article delves into the concept of "Know Your Intermediaries" and its growing importance in compliance, particularly within the financial sector.

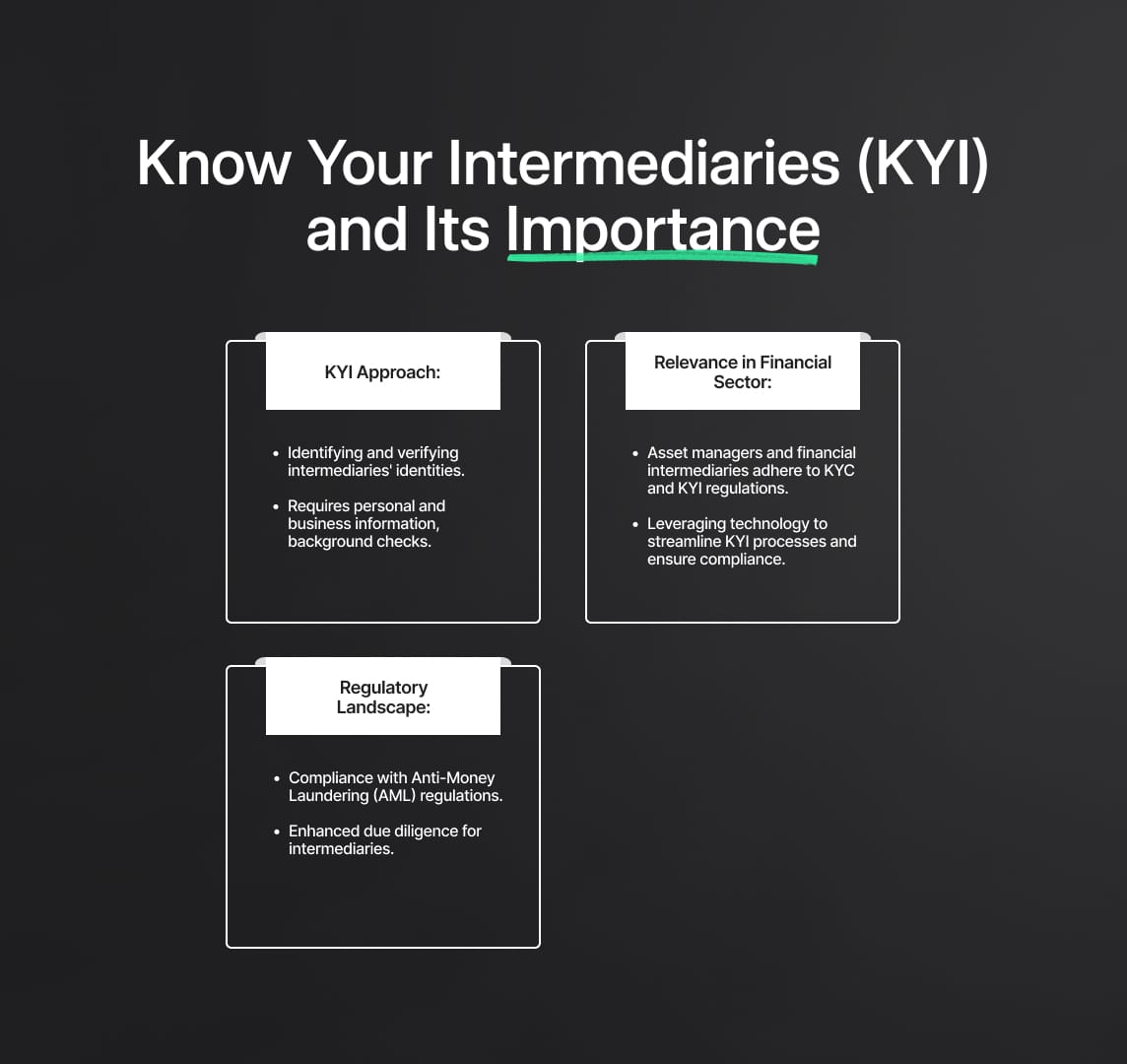

To manage the KYC of intermediaries, companies are increasingly expected to adopt a "Know Your Intermediaries" (KYI) approach [1][2][3]. This approach is similar to the "Know Your Customer" (KYC) approach and refers to the process of identifying and verifying the identity of intermediaries doing business with the company. To implement KYI, companies may require intermediaries to provide personal and business information, as well as conduct background checks [1]. Asset managers and financial intermediaries, in particular, are subject to stringent KYC and Anti-Money Laundering (AML) regulations, making it imperative for them to follow KYC and KYI processes [4]. Companies can leverage technology to streamline their KYI processes and ensure compliance with regulatory requirements [1][3].

Source

[1]

KYC Compliance: the regulatory process

Over the past few years, the Anti-Money Laundering (AML) and Know Your Customer (KYC) landscape in the European Union has undergone significant changes. Directive 2019/1153, which all EU member states were required to adopt by August 2021, aimed to address the prevalence of money laundering within the union. The directive facilitates information exchange with Europol, gives Financial Intelligence Units (FIUs) access to law enforcement information, and streamlines access to financial and bank account information by law enforcement and anti-corruption authorities.

KYC and AML regulations play a crucial role in preventing criminal activities such as money laundering, which often stem from illegal activities like drug dealing, human trafficking, and black-market firearms. Laundered money can be used to fund terrorism and expand criminal enterprises.

AML rules are particularly important in Europe due to the Schengen Agreement, which allows for ease of movement across national borders, making it easier for criminals to conduct illicit activities.

In addition to Directive 2019/1153, other directives and regulations governing money laundering in the EU include the Payments Services Directive (PSD2), which secures electronic payments through Secure Customer Authentication (SCA); the General Data Protection Regulation (GDPR), which governs data usage and ensures customer privacy; the Financial Action Task Force (FATF) Recommendations, which create the framework for KYC and AML regulations; and Customer Due Diligence (CDD)and Enhanced Due Diligence (EDD) processes.

In 2022, the EU also announced the creation of the Anti-Money Laundering Authority AMLA, which would oversee FIUs and assist with the launch and implementation of new AML regulations. AMLA has the authority to impose fines of up to €10 million or 10% of annual turnover for non-compliance. GDPR breaches can also result in substantial fines, with a cap of €20 million or 4% of global turnover for the previous financial year, whichever is highest.

It is crucial for companies operating within the European Union to stay up-to-date with AML/KYC regulations to avoid substantial fines and other serious penalties. A Data Pro, for example, provides extensive due diligence reports to help businesses stay compliant and checks sanctions lists and scans relevant databases for known offenders.

In conclusion, the evolving landscape of AML and KYC regulations within the EU reflects the ongoing efforts to combat money laundering and other criminal activities. Financial institutions must adapt and adhere to these changes to protect both their customers and themselves from the risks associated with illegal financial transactions. By staying informed and compliant, businesses can contribute to a safer and more transparent financial ecosystem.

Reduce your

compliance risks