IFRS 9: Overlays, Model Improvements, and Governance for Novel Risks

IFRS 9 requires banks to include forward-looking data in expected credit loss calculations, posing challenges with risks like COVID-19, geopolitical instability, high interest rates, inflation, and climate change. Overlays and strong governance are vital for managing these risks effectively.

IFRS 9, the International Financial Reporting Standard for financial instruments, mandates banks to integrate all reasonable and supportable information, including forward-looking data, into their expected credit loss (ECL) calculations. This requirement presents substantial challenges, especially with the advent of novel risks such as the COVID-19 pandemic, geopolitical instability, high interest rates, inflation, and climate change. These emerging risks necessitate the use of overlays and robust governance practices to ensure comprehensive risk assessment and management. This article provides a detailed analysis of the role of overlays in managing these risks, highlights methodological considerations, and outlines the next steps for enhancing risk management practices under IFRS 9.

Source

[1]

Alessandro Micagni

Alessandro Micagni

IFRS 9: Overview of the ECB’s Targeted Review

ECB's Forward-Looking Supervisory Approach

To systematically address banks' provisioning practices under IFRS 9, the European Central Bank (ECB) initiated a targeted review in November 2022, involving 51 banks. This comprehensive review aimed to assess the extent to which these banks' IFRS 9 provisioning frameworks were capable of capturing emerging risks effectively. The review's findings were communicated to the banks, pinpointing weaknesses and offering recommendations for best practices. In 2024, the ECB conducted a follow-up review, covering 2023 year-end financial figures, to monitor the implementation of these recommendations and evaluate the effectiveness of supervisory actions.

Scope and Methodology

The ECB's targeted review was extensive, encompassing both quantitative and qualitative assessments. Banks were selected based on a benchmarking framework designed to evaluate the quality of their internal provisioning practices. This selection ensured a balanced geographical coverage and included a diverse range of banks. The review involved detailed questionnaires and data templates to gather comprehensive information on how banks incorporated novel risks into their ECL calculations.

Findings and Communication

The review revealed several critical findings regarding banks' approaches to novel risks:

- Variability in Methodologies: There was significant variability in how banks addressed novel risks. While some banks had advanced frameworks, others lagged in incorporating these risks effectively.

- Reliance on Overlays: Most banks relied on overlays to capture novel risks, but the robustness and methodological rigor of these overlays varied widely.

- Integration of Forward-Looking Information: Banks were found to incorporate forward-looking information to varying degrees, with some relying heavily on qualitative assessments.

The 2024 Follow-Up Review

The follow-up review conducted in 2024 was aimed at evaluating the implementation of the ECB's recommendations. This review focused on assessing the changes made by banks to their provisioning practices and the effectiveness of these changes in addressing novel risks. Key areas of focus included:

- Adoption of Best Practices: The extent to which banks had adopted the ECB's recommended best practices in their provisioning frameworks.

- Effectiveness of Overlays: Evaluation of the robustness and effectiveness of overlays used by banks to capture novel risks.

- Governance Enhancements: Assessment of improvements in governance practices and the clarity of roles and responsibilities in the risk management process.

The Continued Prominence of Overlays in IFRS 9

Necessity and Application

Overlays have become indispensable tools for banks to manage novel risks under IFRS 9. The primary reason for their necessity is the insufficiency of historical data to model these risks accurately. Traditional statistical models depend heavily on historical data to predict future credit losses. However, novel risks such as the COVID-19 pandemic, geopolitical instability, high interest rates, inflation, and climate change do not have sufficient historical precedents to inform these models. Consequently, out-of-model adjustments, or overlays, are necessary to ensure comprehensive risk coverage.

During the COVID-19 pandemic, the use of overlays became particularly prevalent as banks faced unprecedented challenges. The pandemic underscored the limitations of existing models and highlighted the need for flexible, forward-looking adjustments to capture the impact of novel risks accurately. Even as the immediate effects of the pandemic have subsided, the continued emergence of new risks has maintained the relevance of overlays. These tools are now recognized as crucial for addressing risks that lack sufficient historical data, providing banks with a means to incorporate forward-looking information into their ECL calculations effectively.

Methodological Considerations

For overlays to be effective, they must be grounded in robust analysis and supported by sound governance. This process involves several critical methodological considerations:

- Data Use: Effective overlays require the integration of all reasonable and supportable information. This includes internal experience, peer data, and public information. By leveraging a broad spectrum of data sources, banks can construct more accurate simulations and scenarios that reflect potential future conditions.

- Scenario Analysis: While IFRS 9 does not mandate a large number of detailed simulations, it does require that overlays incorporate a reasonable level of detail. Scenario analysis is a crucial component of this process. Banks must develop multiple scenarios that capture a range of possible outcomes related to novel risks. This approach helps to ensure that overlays are comprehensive and reflect a wide array of potential future events.

- Governance Frameworks: Robust governance frameworks are essential to oversee the application of overlays. This includes clear responsibilities, involvement of finance and business units, and well-defined escalation procedures. Effective governance ensures that overlays are applied consistently and transparently, enhancing their reliability and effectiveness.

- Methodological Rigor: Overlays should not rely solely on subjective judgment. Instead, they should be based on quantifiable data and rigorous analytical methods. This helps to mitigate biases and enhances the objectivity of the ECL calculations.

Persistent Use and Variability

Despite initial expectations that the influx of new data would reduce the reliance on overlays, their use has remained steady. Approximately a quarter of loan loss coverage in banks' performing loan books is attributed to overlays. This persistence is due to the ongoing emergence of novel risks and the inherent limitations of existing statistical models in capturing these risks adequately.

However, the ECB's review highlighted significant variability in banks' reliance on overlays. This variability is influenced by several factors:

- Legacy Model Capabilities: Banks with more advanced legacy models may rely less on overlays, while those with less sophisticated models depend more heavily on them. The capability of these models to incorporate forward-looking information effectively is a key determinant of this variability.

- Risk Exposures: The extent and nature of a bank's exposure to novel risks also affect the reliance on overlays. Banks with higher exposure to specific novel risks are more likely to use overlays extensively.

- Methodological Robustness: The robustness of the methodologies used to develop overlays varies significantly among banks. Some banks have implemented highly sophisticated and detailed overlay frameworks, while others have more rudimentary approaches. This disparity can lead to differences in the effectiveness and reliability of the overlays.

IFRS 9 Specific Considerations for Long-Lasting Novel Risks

Climate and Environmental Risks

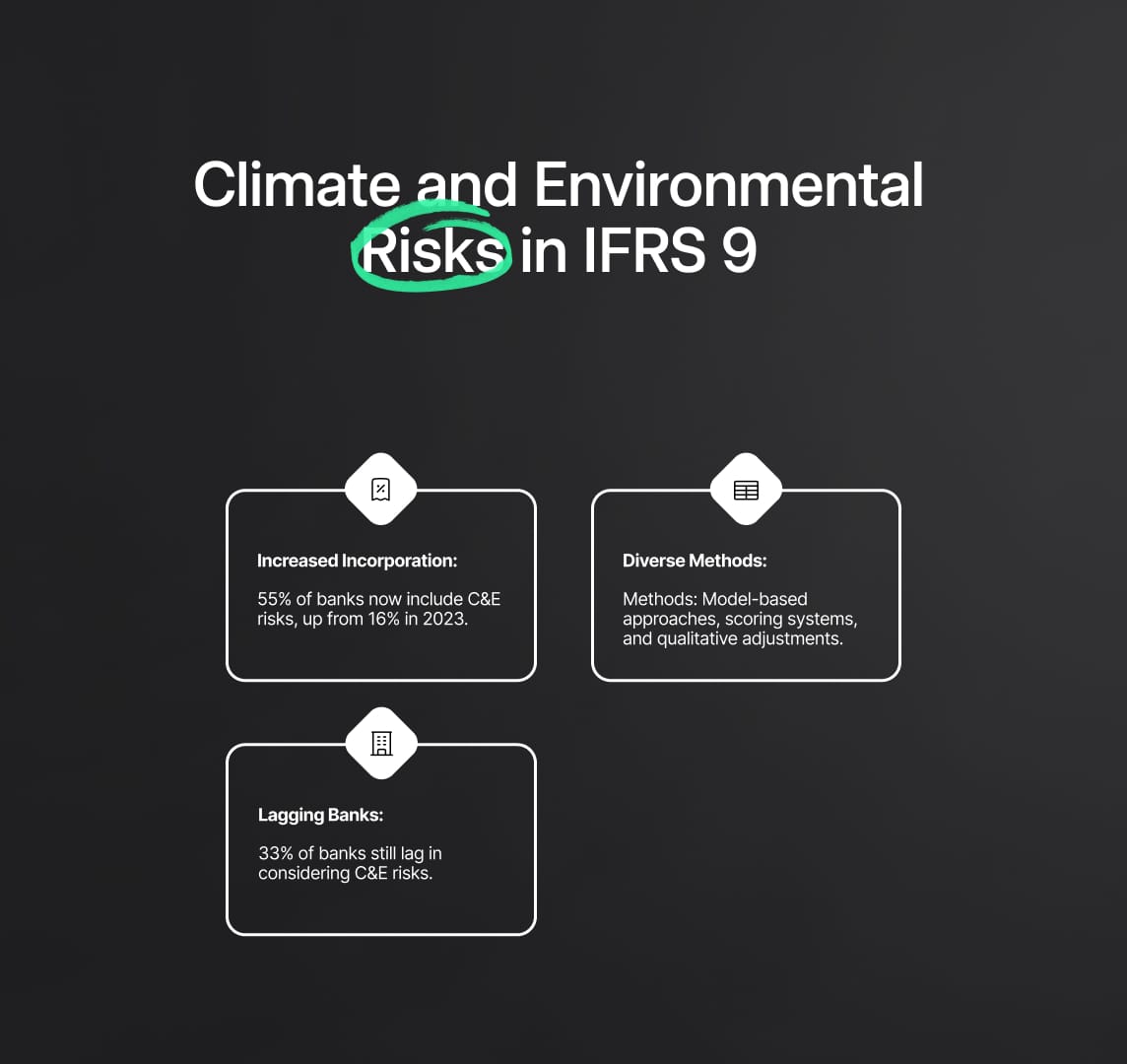

The European Central Bank (ECB)'s first targeted IFRS 9 review and subsequent initiatives have significantly increased the consideration of climate and environmental (C&E) risks among banks. As of the latest review, 55% of banks now incorporate C&E risks into their provisioning frameworks, up from a mere 16% in 2023. This marked increase reflects a growing awareness of the financial implications of climate change and environmental factors, as well as a proactive shift towards integrating these considerations into risk management practices. However, this progress also highlights the need for continued improvements to ensure comprehensive and effective risk assessment.

Methods of Incorporation

Banks employ a variety of methods to account for C&E risks, ensuring that their risk management frameworks are both robust and forward-looking. These methods include:

- Model-Based Approaches: Some banks utilize quantitative models and simulation-based approaches to project potential future scenarios. These models often consider various risk factors, such as increased transition risk due to regulatory changes or physical risks from extreme weather events. By modeling these scenarios, banks can better understand the potential impact on their portfolios.

- Scoring Systems: Another common approach involves the development of scoring systems to evaluate the exposure of debtors to transition and physical risks. These systems assign scores based on factors like the carbon footprint of a debtor’s operations or their geographic location's susceptibility to environmental changes. Such scoring systems help in synthesizing complex data into actionable insights.

- Qualitative Adjustments: Some banks integrate C&E risks directly into their underlying credit ratings through qualitative adjustments. This might involve expert judgment to assess how well-prepared a debtor is for transitioning to a low-carbon economy or their resilience to environmental disruptions. These qualitative elements ensure that the risk assessments are not solely dependent on historical data, which might not fully capture future risks.

Challenges and Lagging Banks

Despite notable progress, significant challenges remain. The ECB's review identified that 33% of banks still do not consider C&E risks in their provisioning frameworks. Additionally, 12% of banks rely on macro-components of their IFRS 9 models to address these risks indirectly through general forward-looking scenarios. This indirect approach often lacks the necessary risk sensitivity and fails to differentiate between debtors unevenly affected by C&E risks. As a result, the risk assessments can be incomplete, potentially leading to inadequate provisioning for these long-term risks.

IFRS 9 & Geopolitical Risks

Current Practices and Limitations

The incorporation of geopolitical risks into banks' provisioning frameworks has seen a slight increase, with 63% of banks using overlays and 4% employing in-model adjustments. However, this level of consideration does not adequately reflect the rising uncertainties and potential downside risks in the current geopolitical landscape. Events such as trade wars, political instability, and sanctions can have significant and uneven impacts on different sectors and regions, which are not fully captured by many banks' current risk assessment practices.

Ineffective Approaches

A common issue is that some banks include geopolitical risks only in the narrative underpinning their macroeconomic scenarios or by stressing existing scenarios. This approach is often too crude, failing to capture the sector-specific impacts of geopolitical events. For example, while a trade war might not drastically alter GDP projections, it could severely impact export-reliant industries and specific companies within those industries. This lack of differentiation hampers timely risk identification and comprehensive risk management, leading to potential underestimation of credit risks associated with geopolitical factors.

Interest Rate Risks in Commercial Real Estate (CRE) Portfolios

Sectoral Approaches and Compliance

Provisioning for interest rate risks in commercial real estate (CRE) portfolios remains a notable weak spot for many banks. Only half of the banks in the sample have developed a sectoral approach to measure the impact of interest rate risks, specifically through interest rate overlays for CRE. This indicates a significant gap in compliance with ECB expectations, which recommend sector-specific in-model adjustments or overlays to account for the effects of higher interest rates on CRE client debt capacity.

Good and Bad Practices

Good Practices:

- Simulations and Stress Testing: Effective practices include conducting simulations of probability of default (PD) and loss given default (LGD) effects by stressing the financial figures of counterparties subject to high interest rates. These simulations consider potential declines in collateral valuations and assess the overall impact on the borrower’s financial health.

- Detailed Scenario Analysis: Banks that employ detailed scenario analysis to evaluate the impact of different interest rate environments on their CRE portfolios are better positioned to manage these risks. Such analyses help in understanding how varying interest rate levels can affect debt servicing capabilities and property values.

Bad Practices:

- General Expert Judgment: Some banks rely heavily on general references to expert judgment without further corroboration. While expert opinions are valuable, they should be supplemented with quantitative data and robust analysis to ensure accuracy and reliability.

- Inadequate Risk Differentiation: A common bad practice is applying lifetime ECL to CRE portfolios without proper risk differentiation or stage transfers. This approach fails to account for the specific risk profiles of different borrowers and properties, leading to potential under-provisioning.

- Ignoring Specific Risks: Failing to differentiate between various risks within the CRE sector, such as location-specific risks or varying impacts of interest rate changes on different types of properties, results in incomplete risk assessment and management.

Quantification, IFRS 9 Stage Transfers, and Governance

Quantification of Risks

The ECB’s review has underscored both advancements and ongoing challenges in the quantification methodologies of overlays under IFRS 9. While some banks have improved their practices, significant design flaws persist in a small number of institutions. Notably, the use of umbrella overlays that cover a broad spectrum of risks without specific differentiation is a common issue. Such generic approaches fail to accurately capture the distinct nature and impact of various risks, leading to potential underestimation of expected credit losses (ECL). Additionally, the inappropriate application of lifetime losses to vulnerable sectors without adequately measuring the specific impact of these risks further complicates accurate provisioning.

Common Bad Practices

One widespread bad practice identified is the application of overlays at the total ECL level. This approach is fundamentally at odds with IFRS 9 principles, which mandate that all identifiable risks should be reflected in the probabilities of default (PD) and staging assessments. Using total ECL overlays leads to an aggregated view that lacks the necessary granularity to differentiate and address specific risks effectively. The ECB strongly recommends discontinuing this practice as it results in insufficient risk coverage and inadequate differentiation, which can ultimately undermine the reliability of the provisioning process.

IFRS 9 Stage Transfers

Stage transfers are critical within the IFRS 9 framework as they accurately reflect the evolving credit risk of loans. The ECB’s review revealed substantial deficiencies in the methodologies and governance processes related to stage transfers. While some improvements were noted, particularly in linking overlays and in-model adjustments to stage assessments, many banks still fall short of ECB recommendations.

Issues with Umbrella Overlays

A significant issue identified is the continued use of umbrella overlays that do not differentiate between specific risks. This practice results in an inadequate risk coverage and fails to comply with IFRS 9 principles, which require that stage transfers should reflect all identifiable risks accurately. Furthermore, some banks incorrectly apply lifetime ECL to entire vulnerable sectors without a detailed assessment of the novel risks impacting these sectors, leading to potential misestimation of the necessary provisions.

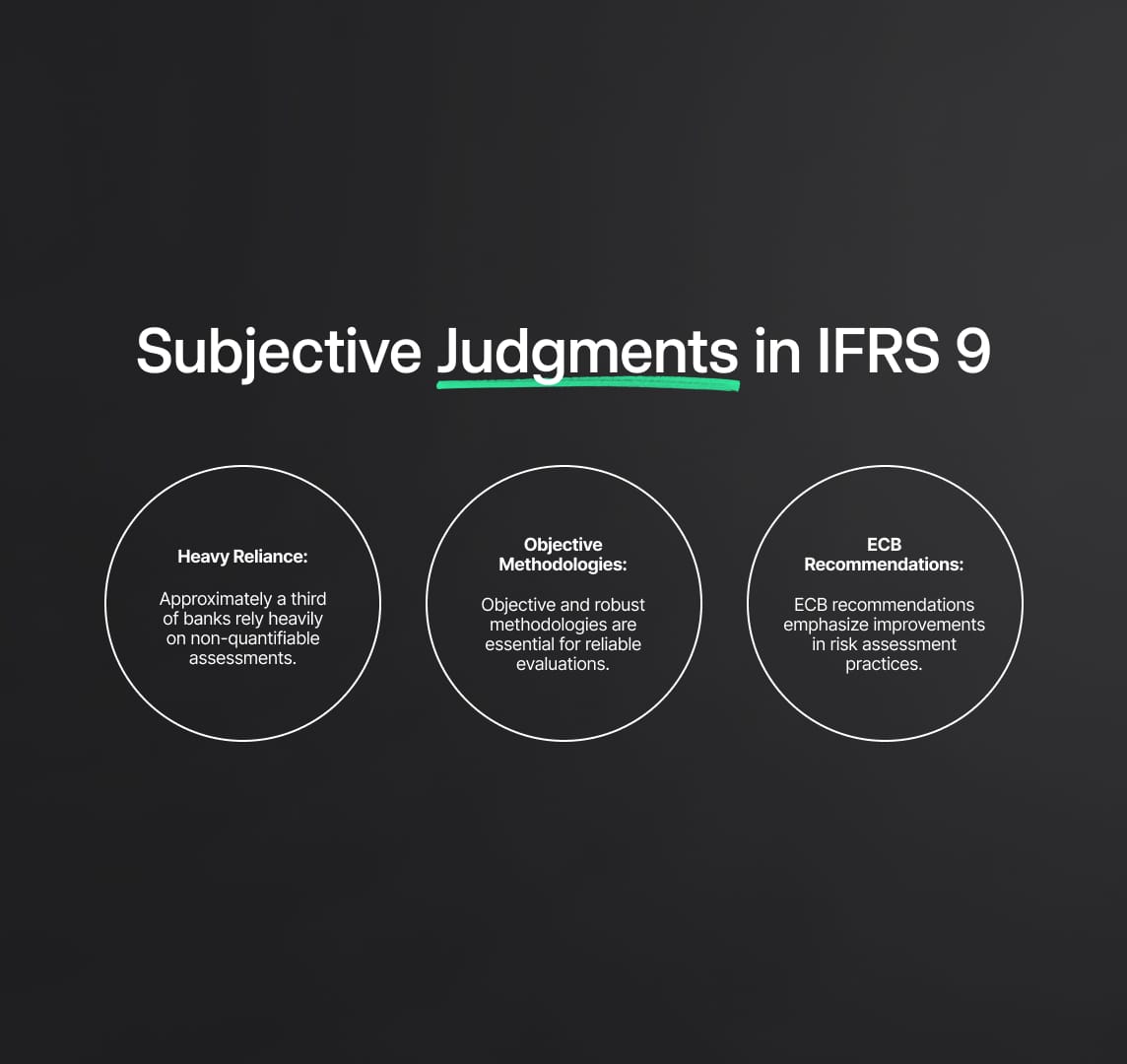

Subjective Judgments

Another critical challenge is the over-reliance on subjective judgments in the stage transfer process. Approximately a third of the banks reviewed depend heavily on non-quantifiable assessments, which undermines the objectivity and reliability of risk evaluations. Despite the inherent difficulties in quantifying certain risks, the ECB maintains that objective and robust methodologies are essential. The successful implementation of these methodologies by many banks demonstrates that the ECB’s expectations are realistic and achievable.

IFRS 9 Governance and Compliance

To address the deficiencies observed in risk quantification and stage transfers, the ECB has issued specific recommendations emphasizing the importance of robust methodologies and comprehensive governance frameworks. These recommendations are designed to ensure banks’ compliance with IFRS 9 requirements and to enhance their risk management practices. Banks are expected to implement these guidelines to improve their overall risk assessment and provisioning processes.

Supervisory Actions

Banks that fail to comply with the ECB’s recommendations can expect further supervisory actions. These actions are aimed at enforcing adherence to IFRS 9 principles, ensuring that all identifiable risks are accurately captured and quantified. The ECB’s ongoing supervision is intended to promote best practices across the banking sector, enhancing the overall resilience and stability of financial institutions.

Technical Details of IFRS 9 Stage Transfers

Effective IFRS 9 stage transfers require precise methodologies that reflect the nuanced risk profiles of various loans. These methodologies should incorporate:

- Probability of Default (PD) Adjustments: Banks need to adjust PD calculations to account for emerging risks accurately. This involves integrating forward-looking information and scenario analysis to anticipate how different risk factors might influence the likelihood of default.

- Loss Given Default (LGD) Adjustments: Similar to PD adjustments, LGD models should be recalibrated to reflect the potential impacts of novel risks. This might involve stress testing against various economic scenarios to determine the potential loss severity.

- Staging Criteria: Establishing clear criteria for stage transfers is crucial. This includes defining quantitative thresholds and qualitative indicators that signal increased credit risk. Regular reviews and updates to these criteria ensure they remain relevant in a changing risk environment.

Comprehensive Governance Frameworks

Robust governance frameworks are essential to oversee and validate the stage transfer process. These frameworks should encompass:

- Clear Allocation of Responsibilities: Defining roles and responsibilities across different units, including risk management, finance, and business lines, to ensure accountability and proper oversight.

- Involvement of Finance and Business Units: Active involvement of these units ensures that stage transfer decisions are informed by comprehensive financial data and business insights.

- Escalation Procedures: Establishing well-defined escalation procedures for cases where significant judgment is required ensures that complex decisions are reviewed and validated by senior management or specialized committees.

- Regular Validation and Backtesting: Continuous validation and backtesting of stage transfer methodologies against actual performance data help in refining the models and improving their predictive accuracy.

Data Insights and Analysis for IFRS 9

Overlays in Loan Loss Provisions

Overlays have become a critical component in the loan loss provisioning process for banks under IFRS 9. These out-of-model adjustments are employed to address novel risks that traditional models cannot adequately capture due to insufficient historical data.

The ECB's review indicates a significant variance in how banks apply overlays, which is reflective of the diverse methodologies and risk exposures across the sector. Some banks employ sophisticated overlay techniques that integrate forward-looking information and scenario analysis, while others rely on more rudimentary approaches. This variance impacts the aggregated coverage ratios of loan loss provisions, demonstrating that while some banks are effectively using overlays to cover a wide array of risks, others are not fully capturing the potential future credit losses.

Earnings Management and Provisions

The relationship between loan loss provisions and pre-provisioning profits suggests that overlays may be used for earnings management purposes. The ECB's analysis reveals that overlay provisions are statistically significantly correlated with pre-provisioning profits.

This implies that banks might be adjusting their overlays to smooth out earnings and manage financial performance. In contrast, provisions derived from Expected Credit Loss (ECL) models do not show this correlation, indicating that they are less likely to be influenced by profit considerations. This finding underscores the need for stringent governance and transparency in the application of overlays to ensure they reflect genuine risk considerations rather than financial performance manipulation.

Use of Overlays Across Loan Types

Banks recognise that novel risks impact all segments of their lending business, leading to the widespread use of overlays across various loan types. These include corporate loans, loans to small and medium-sized enterprises (SMEs), and retail loans. The comprehensive application of overlays across different loan portfolios highlights the banks' efforts to adapt their risk management practices to the evolving risk landscape.

This approach ensures that they can address specific risks associated with each loan type, which may vary significantly in nature and impact. For instance, corporate loans might be more susceptible to geopolitical risks, while retail loans might be more influenced by macroeconomic conditions such as inflation and employment rates.

Methods of Capturing Emerging Risk Factors

Banks employ a variety of methods to capture emerging risk factors within their IFRS 9 provisioning frameworks. The ECB's review indicates a growing reliance on overlays, reflecting their effectiveness in addressing novel risks that are not well-represented in historical data. However, there is a persistent reliance on legacy models by some banks, which may not adequately capture the complexities of current risk factors. Effective risk capture methods include incorporating detailed scenario analysis and forward-looking information into overlay calculations. This ensures a more accurate and comprehensive assessment of potential future credit losses.

Interest Rate Overlays for CRE Exposures

The application of interest rate overlays specifically for commercial real estate (CRE) exposures remains limited, with only half of the banks adopting a sector-specific approach. This indicates a gap in the risk management practices of many banks, as sector-specific overlays are crucial for accurately capturing the impact of interest rate changes on CRE portfolios. Effective interest rate overlays should account for the unique sensitivities of CRE clients to interest rate fluctuations, which can significantly affect their debt servicing capabilities and, consequently, the bank's credit risk.

Compliance with ECL Quantification Methodology

Improvements have been observed in the design and quantification methodologies of overlays, with a growing number of banks complying with the ECB’s recommendations. This progress is essential for ensuring that overlays are based on sound and robust methodologies that accurately reflect the potential credit losses. However, there is still room for improvement as not all banks have fully adopted the recommended practices. Ongoing supervision and targeted reviews by the ECB are necessary to ensure continued progress and adherence to best practices.

Level of Overlays Application

A common issue identified in the ECB’s review is the application of overlays at an aggregated level. This practice hinders effective risk differentiation and fails to align with IFRS 9 principles, which emphasize the need for detailed and specific risk assessments. Applying overlays at a granular level ensures that all identifiable risks are accurately captured and appropriately provisioned. Banks need to move towards more granular and differentiated risk assessments to enhance the effectiveness of their overlays and overall risk management strategies.

Collective Staging Practices

Stage 2 assessments under IFRS 9 are crucial for capturing increased credit risks. However, the ECB's review shows that the majority of banks still conduct these assessments predominantly at the individual borrower level, with limited use of collective assessments. This approach does not fully incorporate the collective impact of risks, leading to incomplete risk coverage. Collective staging assessments are essential for accurately reflecting the credit risk across entire loan portfolios, particularly in the context of systemic risks that affect multiple borrowers simultaneously.

Reduce your

compliance risks