Macroprudential Regulations for NBFI

In May 2024, the European Commission initiates a consultation on NBFI macroprudential policies, aiming to address vulnerabilities and improve supervision.

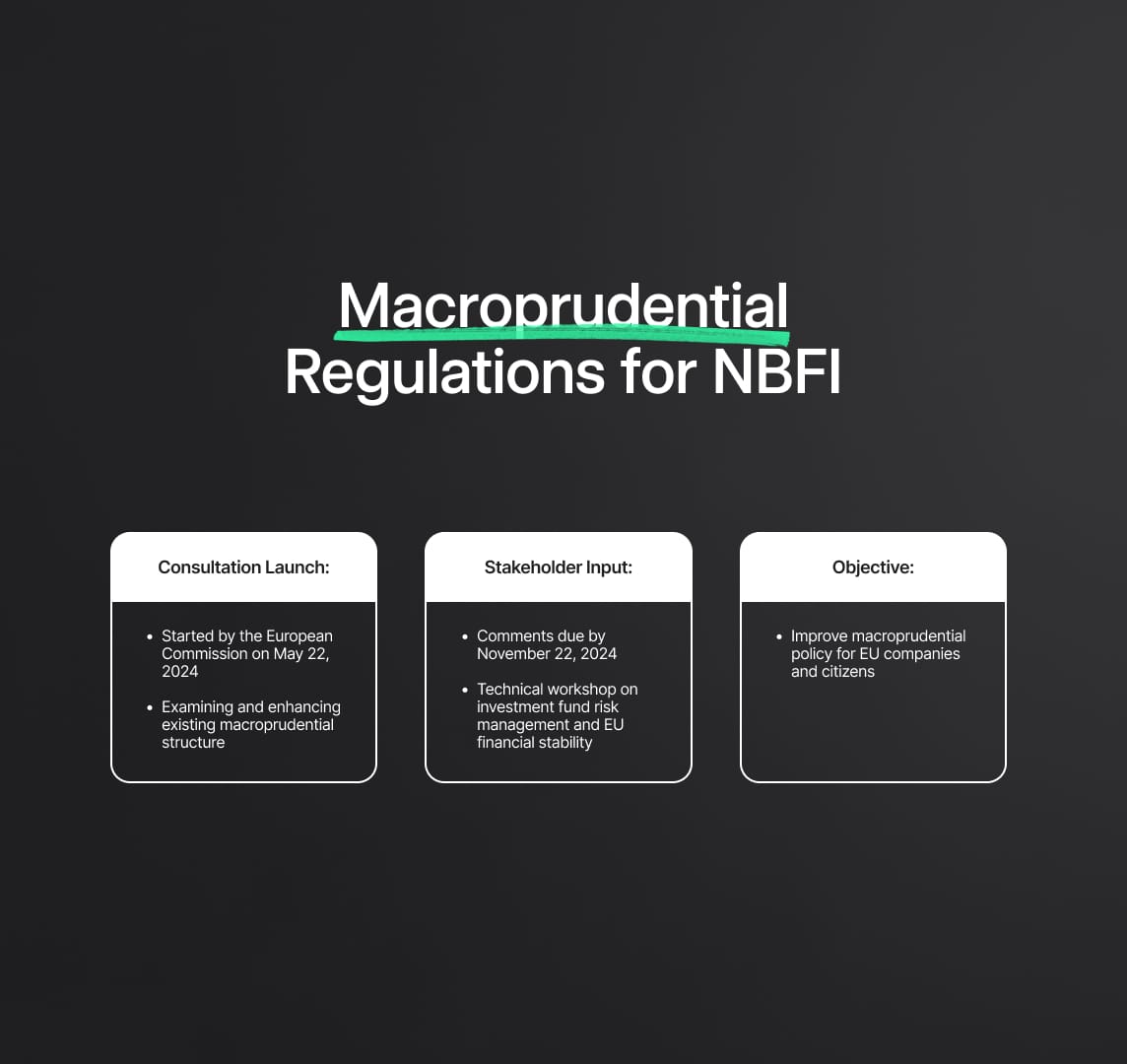

A consultation on macroprudential regulations for non-bank financial intermediation (NBFI) was launched by the European Commission on May 22, 2024. The objective of this endeavor is to examine and enhance the existing macro prudential structure. Numerous regulated and uncontrolled financial sectors are included in NBFI. As of the third quarter of 2023, traditional banks controlled 36% of the total financial assets in the EU, or roughly EUR 38 trillion, while non-bank financial intermediaries had about 42.9 trillion, or 41% of the total.

In its Consultation Paper, the Commission lists hazards facing the NBFI industry and requests input on difficulties with supervision. The deadline for comments is November 22, 2024. In addition, a technical workshop on macroprudential policy with an emphasis on investment fund risk management and EU financial stability will be held. Commissioner for Financial Stability Mairead McGuinness stressed the value of a broad financial sector for stability and lowering reliance on traditional banking, as well as the role NBFI plays in advancing the EU's sustainability and digital goals. The purpose of the consultation is to improve macroprudential policy for the benefit of EU companies and citizens.

The Role and Regulation of Non-Bank Financial Intermediation (NBFI) in the EU

A wide range of financial industries, including asset management firms, investment funds, pension funds, insurance companies, family offices, and supply chain finance companies, are included in non-bank financial intermediation, or NBFI. NBFIs had roughly €42.9 trillion, or 41%, of the total financial assets of the EU as of Q3 2023, whereas banks controlled about €38 trillion, or 36%.

Concerns over NBFI's financial viability have grown in the wake of events like the UK gilt crisis in 2022 and the cash crunch in March 2020. This has prompted talks about global policy as well as a number of regulatory actions. Important international bodies like the International Organization of Securities Commissions (IOSCO) and the Financial Stability Board (FSB), in conjunction with US and UK authorities, have been attempting to fill in the gaps in the macroprudential framework pertaining to non-bank financial institutions.

Notwithstanding the dangers, NBFIs support resilience and financial diversification. They are essential to the Capital Markets Union (CMU) because they provide tools for risk management and funding sources to go along with traditional bank lending. Tighter banking restrictions implemented after the 2008 financial crisis have made it possible for NBFIs to grow into previously bank-dominated areas. The stability and integration of the capital markets have been improved by the EU's introduction of several regulations to control NBFI activity.

European Commission Consultation on Enhancing the Macroprudential Framework for NBFI

In order to assess and enhance the macroprudential framework for non-bank financial intermediation (NBFI), the European Commission has opened public consultations. This project does not address recent legislative agreements such as the EMIR 3 and Solvency II review; instead, it solicits feedback from stakeholders regarding the sufficiency and efficacy of present macroprudential policies:

- Examine the Macroprudential Tools Available Now: Evaluate how well the current supervisory structures and macroprudential instruments are serving their intended aims.

- Examine and Reuse Current Tools: Think about modifying or repurposing the present microprudential and reporting instruments, taking into account their activation triggers and layout.

- Describe New Instruments and Enhance Collaboration: Examine the possibility of implementing fresh macroprudential techniques and instruments to improve cooperation throughout the EU.

The data acquired from this consultation will help the College of Commissioners in 2024–2029 outline its policies. All interested parties are encouraged to engage, although the NBFI industry, national authorities, central banks, and EU institutions are the targeted stakeholders.

Key Vulnerabilities and Risks in Non-Bank Financial Intermediation (NBFI)

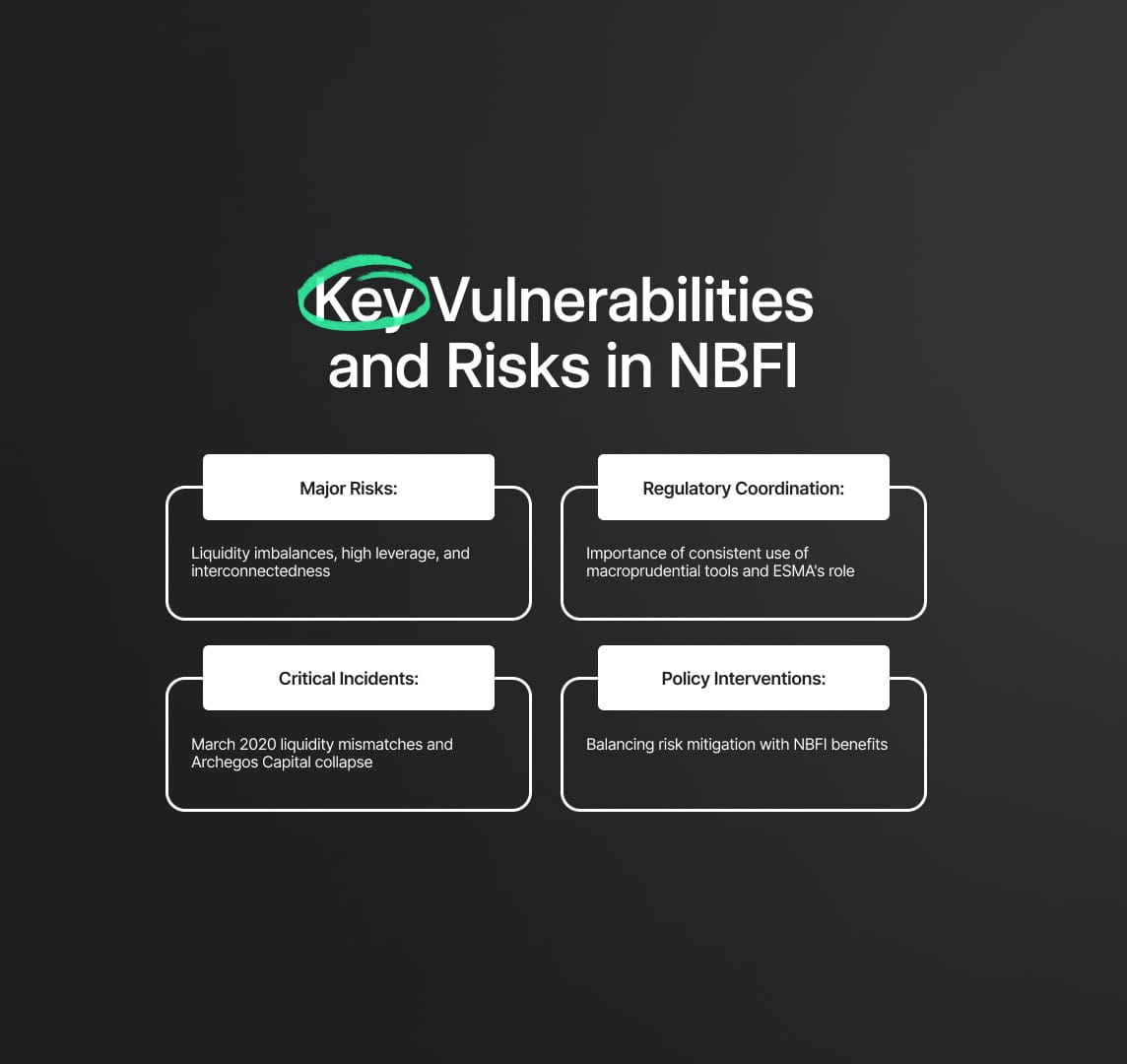

A new report from the European Commission identifies a number of significant risks and vulnerabilities related to non-bank financial intermediation (NBFI). Unrestricted liquidity imbalances, high leverage, and connections between NBFIs and banks as well as inside NBFI sectors are a few of them. These vulnerabilities may be made worse by the EU's macroprudential frameworks' inconsistent and disorganized design, which could result in systemic risks such counterparty, liquidity, concentration, and spillover hazards.

When the market was stressed in March 2020 and several Money Market Funds (MMFs) saw large outflows, the ECB intervened as a result of liquidity mismatches. The demise of Archegos Capital Management serves as evidence that excessive leverage carries serious dangers for lenders and the larger financial system. Although interconnectedness increases market efficiency, it can also mask systemic risks and exacerbate financial instability, as seen by the 2022 energy price surge and in growing crypto assets market.

Different supervisory mandates and inconsistent use of macroprudential tools might result in regulatory arbitrage and impair the ability to identify systemic concerns. The importance of coordination is demonstrated by ESMA's involvement in the management of liquidity risks in the investment fund industry during the COVID-19 crisis.

Notwithstanding these flaws, NBFIs offer significant funding options that promote capital market accessibility and the stability of the financial system. Interventions in policy should mitigate these risks without unreasonably limiting the advantages that NBFIs offer the financial system.

Macroprudential Tools and Supervisory Architecture in EU Legislation

In order to mitigate systemic risks in the Non-Bank Financial Intermediation (NBFI) sectors, a strong macroprudential framework is necessary. The EU has strengthened its regulatory framework since the 2008 financial crisis, incorporating macroprudential and microprudential supervision for banks as well as important NBFI industries like insurance and investment funds:

- The ESFS, or European System of Financial Supervision: Ensuring financial stability and effective functioning inside the EU is the goal of the European Supervisory Authorities (ESAs) and the European Systemic Risk Board (ESRB), among other agencies that are part of the ESFS. At the EU level, macroprudential monitoring is managed by the ESRB, and systemic risks are observed by ESAs in particular NBFI sectors.

- The function of ESAs: EBA is in charge of major asset-referenced and e-money token issuers under MiCAR, while ESMA and EIOPA monitor systemic risk in particular NBFI sectors. These ESAs support uniform oversight and regulation throughout the European Union.

- Tools for Macroprudential Analysis: Distinct macroprudential mechanisms designed for distinct NBFI sectors are incorporated into EU legislation. The direct mitigation of vulnerabilities and systemic event protection of the financial system is the goal of these instruments.

- Supervisory Control and Guidance: The correct application of macroprudential measures depends on efficient oversight, coordination, and reporting systems. Since NBFIs are cross-border in nature, effective systemic risk mitigation necessitates oversight at both the national and EU levels.

The EU's commitment to strengthening the stability of its financial system and addressing systemic risks within the NBFI sectors is reflected in these regulatory developments. Maintaining financial stability throughout the EU requires a continued focus on strengthening macroprudential supervision and coordinating measures.

Regulation of Asset Management and Open-Ended Funds (OEFs) in the EU

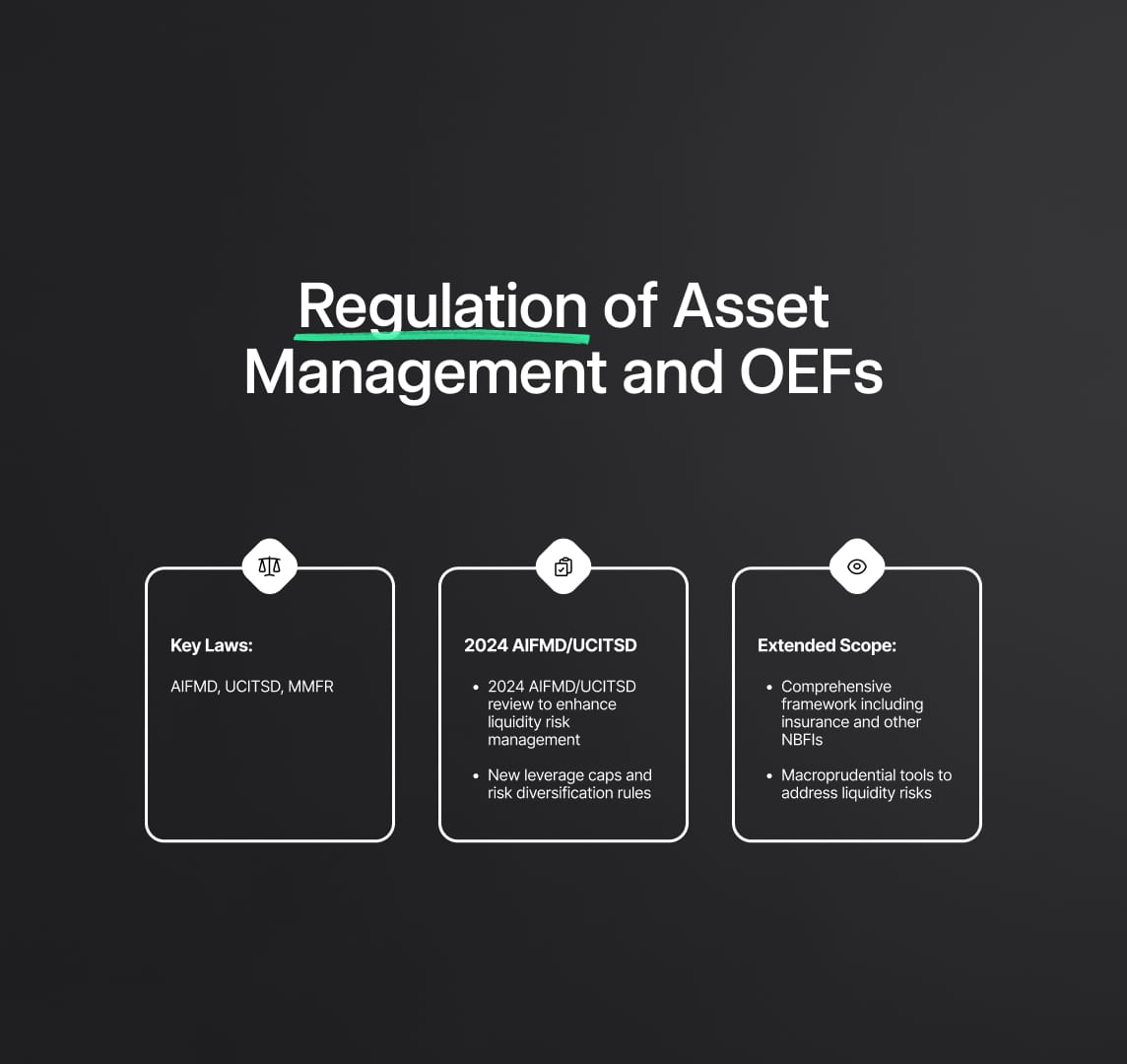

Key laws like the AIFMD, UCITSD, and MMFR regulate the EU's regulatory framework for the investment fund industry, specifically for asset management and open-ended funds (OEFs). These rules cover a range of specifications related to portfolio concentration, transparency, leverage, and liquidity risk management.

The goal of recent regulatory developments, such as the AIFMD/UCITSD review in 2024, is to improve the capacity of UCITS and open-ended AIFs to handle liquidity risks by standardizing the definitions and applications of liquidity management tools, or LMTs. New structural leverage caps and risk diversification regulations also help to improve the sector's risk management skills.

Extending its reach beyond the investment fund business, the insurance sector functions within a comprehensive regulatory framework. Notably, recent modifications have incorporated a macroprudential toolset to mitigate liquidity risks. These modifications provide supervisory agencies more authority to take actions to preserve insurers' capital and liquidity, such as limiting capital distributions in extraordinary situations and temporarily freezing redemption options.

Regulations also apply to other Non-Bank Financial Intermediaries (NBFIs) and markets; among the measures are limits on procyclical effects in collateral haircut calculations and modifications to capital coefficients for major investment enterprises.

Reduce your

compliance risks