Macroprudential Risk Management: EBA Supports DNB

EBA supports Nederlandsche Bank’s macroprudential risk measures targeting high LTV loans, emphasizing the need for robust capital requirements to mitigate systemic vulnerabilities and enhance the resilience of financial institutions

The European Banking Authority (EBA) has conducted a comprehensive evaluation of the macroprudential risk measures proposed by the Central Bank of the Netherlands (DNB), highlighting their essential role in managing macroprudential risk within the Dutch housing market. These targeted measures specifically address macroprudential risks associated with high Loan-To-Value (LTV) loans and the low-risk weights assigned by Internal Ratings-Based (IRB) institutions. EBA's support emphasizes the critical importance of robust capital requirements to bolster banks' resilience against macroprudential risks, particularly those linked to high household debt and market overvaluation.

Source

[1]

Design and Structure of the Macroprudential Risk Measure

Initially activated in January 2022, the extended macroprudential risk measure imposes a minimum average risk weight on mortgage exposures not fully covered by the Dutch National Mortgage Guarantee scheme (NHG). This measure specifically targets IRB institutions, ensuring that they maintain sufficient capital buffers to manage macroprudential risks associated with high-LTV loans effectively.

Key Components of the Macroprudential Risk Measure

- Risk Weight Calibration: The measure assigns a 12% risk weight to the loan portion up to 55% of the property’s market value and a 45% risk weight to the remaining portion above this threshold. This tiered approach reflects the property's macroprudential risk, with higher weights applied to portions exceeding the safer 55% LTV level. The exposure-weighted average risk weight acts as a dynamic risk floor, progressively increasing with the LTV ratio—from 12% for loans with an LTV up to 55% to approximately 26.85% for loans with an LTV of 100%. This calibration minimizes cliff effects and aligns risk weights closely with macroprudential risk, directly linking default risk to higher LTV ratios. Continuous adjustment smoothens regulatory impacts, better capturing the actual risk profile and addressing systemic vulnerabilities in high-LTV lending.

- Minimum Average Risk Weight: A portfolio-level minimum average risk weight ensures that institutions maintain capital levels proportionate to macroprudential risks associated with high-LTV loans. Banks calculate the exposure-weighted average risk weights across all qualifying mortgage loans, maintaining a floor that prevents capital shortfalls in riskier market conditions. By directly linking LTV calculations to real-time market valuations of collateral, the measure dynamically adjusts capital requirements based on current market risks, enhancing the macroprudential risk framework’s responsiveness to adverse market movements.

- Duration: The measure’s extension from 1 December 2024 to 30 November 2026 reflects DNB’s ongoing assessment of sustained macroprudential risks in the Dutch housing market. This extension allows DNB to address persistent risks, such as overvalued property prices and elevated household indebtedness, while providing a regulatory buffer against potential market corrections. Continuous regulatory oversight ensures that capital requirements stay aligned with the evolving macroprudential risk landscape.

Macroprudential Risk Context and Economic Rationale

The Dutch housing market faces significant macroprudential risk due to high household debt levels and the prevalence of high-LTV loans. These systemic vulnerabilities are intensified by a tightening monetary policy environment, rising interest rates, and declining real household incomes, which increase repayment burdens and amplify the likelihood of negative equity scenarios. By maintaining stringent macroprudential risk measures, the DNB aims to safeguard financial stability and prevent the systemic risks associated with an overleveraged housing market.

Rising Systemic Risk and Market Overvaluation: Understanding Macroprudential Risk

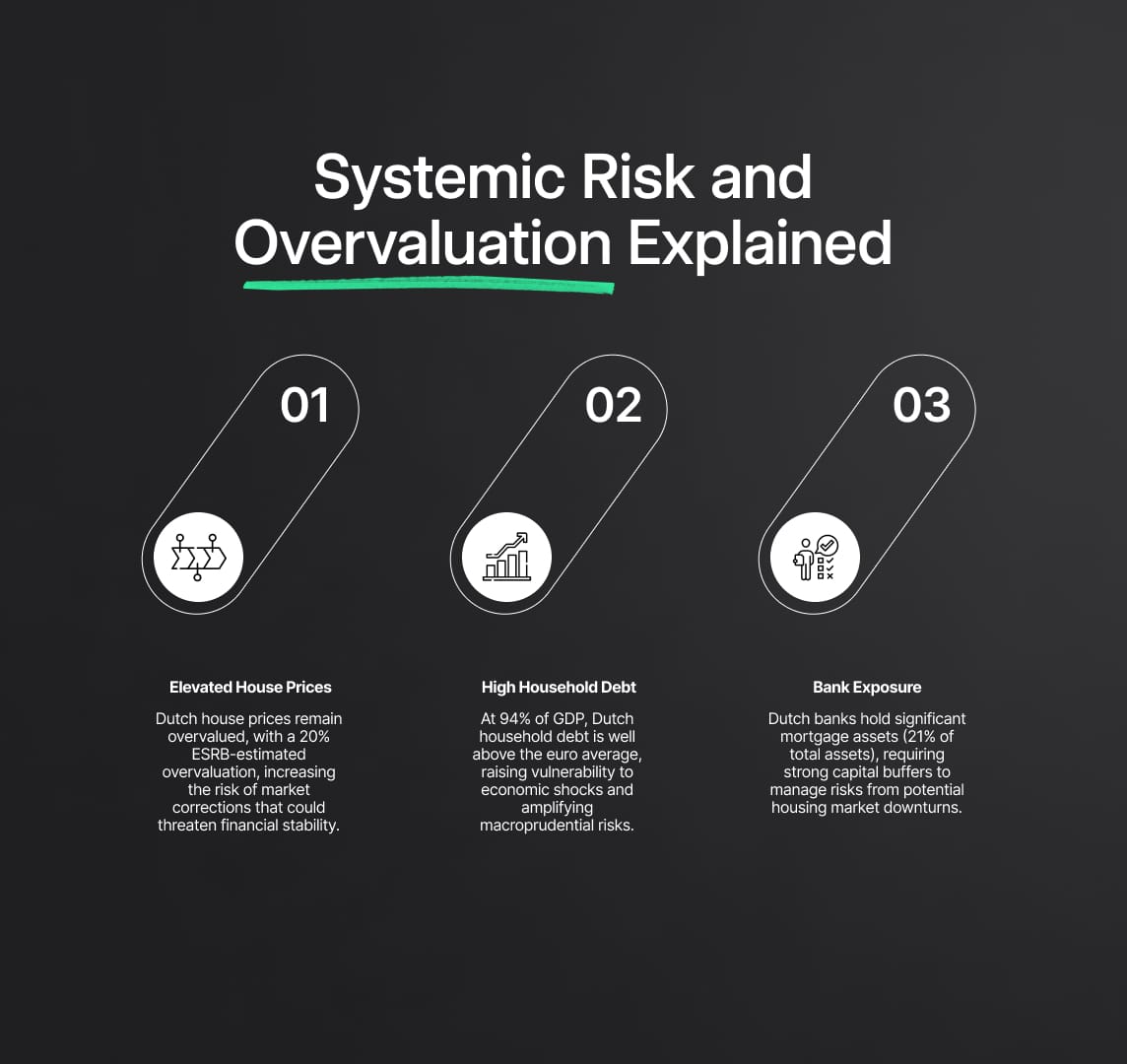

- Elevated House Prices and Macroprudential Risk: House prices in the Netherlands have shown volatile growth, peaking at 21.1% year-on-year in January 2022. Despite a temporary decline, prices rebounded by 8.6% in May 2024, surpassing previous highs and highlighting ongoing overvaluation. The European Systemic Risk Board (ESRB) estimates a 20% overvaluation, driven by a high price-to-income ratio significantly above the euro area average. This sustained overvaluation increases macroprudential risk, heightening the likelihood of market corrections that could destabilize financial institutions heavily exposed to the real estate sector.

- High Household Debt Intensifies Macroprudential Risk: Dutch household debt reached 94% of GDP by the end of 2023, far exceeding the euro area average of 54%. This substantial leverage elevates macroprudential risk by making households more vulnerable to economic shocks, such as rising interest rates and employment downturns. High debt-to-income ratios can significantly reduce consumer spending during market corrections, deepening economic vulnerabilities and adversely affecting banks' asset quality and risk-weighted exposures.

- Bank Exposure and Macroprudential Risk Management: Dutch banks are heavily exposed to residential mortgages, which constitute over 21% of their total assets and approximately 70% of the national mortgage market. This concentrated exposure underscores the critical need for strong capital buffers to manage macroprudential risks. A housing market downturn could lead to substantial credit losses, reinforcing the necessity of robust macroprudential measures to maintain financial stability and prevent systemic disruptions.

Stress Testing, Systemic Risk Assessment, and Calibration Concerns in Macroprudential Risk Frameworks

To validate the measure’s extension, DNB conducted a comprehensive top-down stress test using the 2023 EU-wide adverse scenario, confirming that the capital needed to absorb unexpected losses remained consistent with initial projections. Historical scenario analyses also demonstrated severe cumulative losses over three years, highlighting that systemic macroprudential risk remains significantly elevated, thereby justifying the continuation of stringent macroprudential measures.

Regulatory Concerns and Technical Observations on Macroprudential Risk Measures

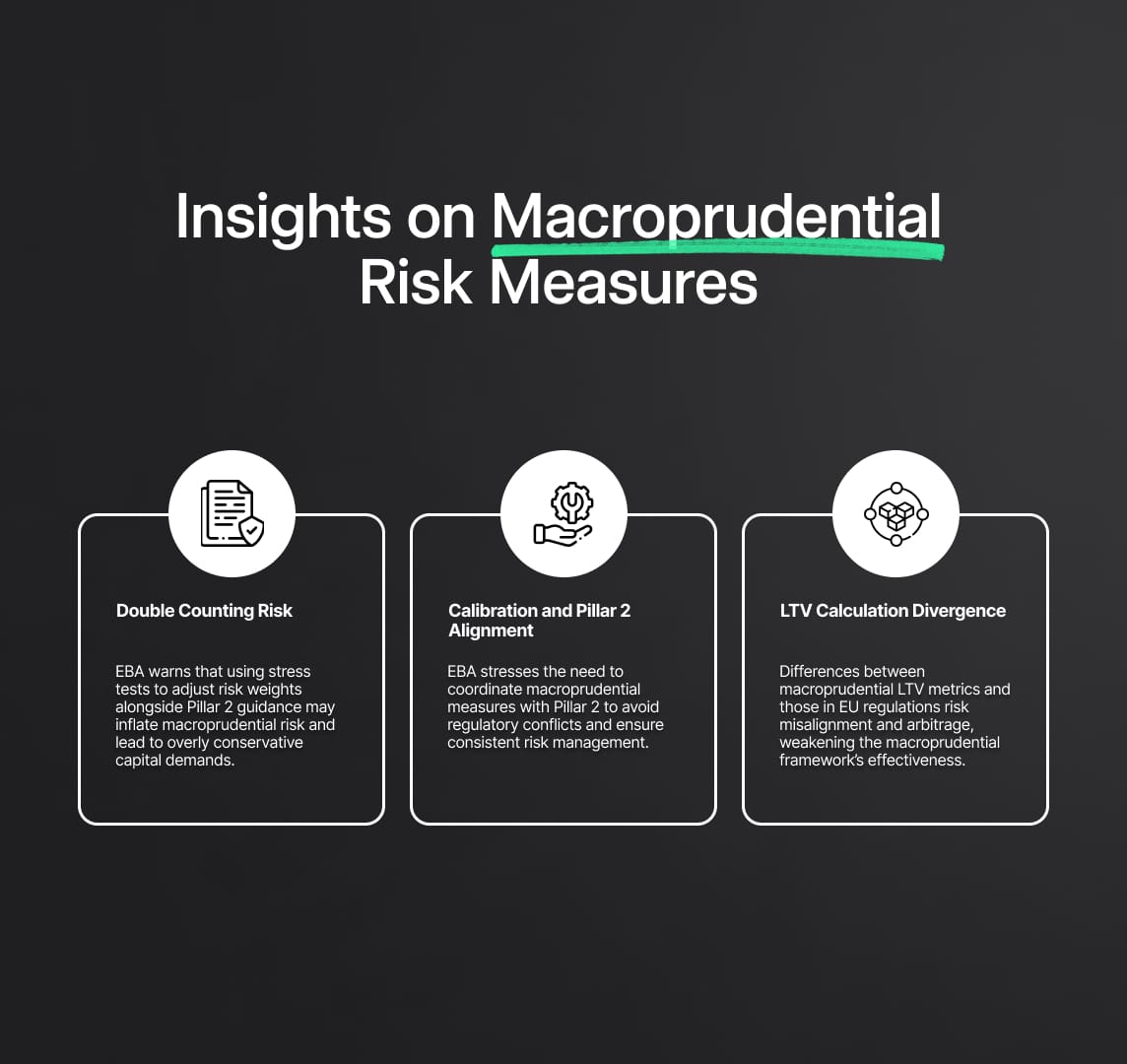

- Double Counting of Risks: The EBA has raised concerns about potential double counting when stress tests are used to adjust risk weights, especially when these adjustments overlap with Pillar 2 guidance. This can result in an inflated assessment of macroprudential risk and lead to excessively conservative capital requirements, complicating regulatory alignment and compliance efforts within the banking sector.

- Calibration Consistency and Pillar 2 Overlaps: The EBA emphasizes the importance of monitoring interactions between the extended macroprudential risk measure and existing Pillar 2 requirements to prevent conflicts within the broader regulatory framework. Ensuring proper alignment is crucial for maintaining a coherent and effective macroprudential risk management strategy across the regulatory spectrum.

- Divergence in LTV Calculations: The EBA identifies potential inconsistencies in the Loan-To-Value (LTV) metrics used in macroprudential risk measures compared to those stipulated in Article 229 of Regulation (EU) 575/2013, as amended by Regulation (EU) 2024/1623. Variances in market value determination and collateral valuation practices could result in regulatory misalignment and open opportunities for arbitrage, potentially undermining the effectiveness of the macroprudential risk framework.

These detailed evaluations underscore the necessity for continued vigilance and adaptation in managing macroprudential risk within the Dutch housing market to safeguard financial stability and prevent systemic vulnerabilities from escalating.

Suitability, Proportionality, and Broader Market Impacts in Macroprudential Risk Management

The Dutch Central Bank (DNB) asserts that the current macroprudential risk measure is suitable, effective, and proportionate in managing macroprudential risk by specifically targeting high Loan-To-Value (LTV) loans, which are a significant source of systemic vulnerability. By implementing differentiated risk weights, this measure discourages banks from high-risk lending, thus enhancing the resilience of systemically important financial institutions. This approach aligns with DNB’s broader macroprudential strategy to mitigate risks associated with excessive leverage and inflated asset valuations in the Dutch housing market.

Specific Regulatory Insights on Macroprudential Risk:

- Targeted Focus on High-Risk Segments: The measure directly impacts Internal Ratings-Based (IRB) institutions, which handle 96% of mortgage lending in the Netherlands, ensuring that macroprudential risk measures are effectively applied where they are most needed. By focusing on IRB institutions that use internal models for risk weight calculations, the measure addresses discrepancies in risk assessments that often underestimate macroprudential risk in high-LTV segments. This targeted approach ensures that systemic risk is accurately captured in capital requirements, reinforcing the stability of the financial sector.

- Impact on Market Dynamics and Competitive Balance: Despite the increased risk weights, the overall levels remain lower compared to other EU Member States, reducing the potential for market distortions and competitive disadvantages. This balance minimizes negative cross-border impacts as Dutch IRB institutions operate under a stringent yet proportionate risk-weighting framework that addresses macroprudential risks effectively. The nuanced calibration of the measure helps avoid disproportionate capital burdens, maintaining a level playing field in the European financial market while prioritizing macroprudential stability.

- Enhanced Resilience of Financial Institutions: By requiring higher capital buffers for high-risk exposures, the measure strengthens the resilience of critical financial institutions against economic downturns. This is particularly important given the interconnectedness of the Dutch financial system within the broader EU market, where macroprudential risks can lead to systemic spillovers with widespread impacts. The focus on IRB banks, which hold significant market share and systemic importance, helps prevent macroprudential risks from destabilizing the financial ecosystem.

Rationale Against Alternative Macroprudential Measures

DNB has consistently argued that alternative macroprudential measures under Regulation (EU) No 575/2013 and Directive 2013/36/EU are inadequate for addressing the specific macroprudential risks in the Dutch housing market. The European Banking Authority (EBA) supports this view, emphasizing the necessity for targeted regulatory actions specifically designed to mitigate systemic vulnerabilities. This focus on tailored macroprudential risk strategies underscores the critical need for precise interventions that directly address the structural risks inherent in high-LTV lending and overleveraged financial practices within the housing market.

Limitations of Standardized Approaches in Addressing Macroprudential Risk

- Insufficiency of Article 124 Measures: The measures under Article 124 of Regulation (EU) No 575/2013, which apply to institutions using the standardized approach, are deemed insufficient for managing macroprudential risk. These institutions represent only a small fraction of the Dutch mortgage market. While standardized approaches apply higher risk weights by default, they fail to capture the lower, potentially understated macroprudential risks assessed under Internal Ratings-Based (IRB) models. Consequently, relying on Article 124 measures would leave significant macroprudential risks within the dominant IRB segment unaddressed, failing to manage systemic vulnerabilities effectively.

- Increased LGD Floors Under Article 164: DNB has evaluated measures that adjust Loss Given Default (LGD) floors under Article 164 but found them less effective in managing macroprudential risk. These measures disproportionately impact lower-LTV loans, inadvertently penalizing conservative lending practices while failing to curb high-LTV, high-risk lending behaviors. Adjusting LGD floors could distort internal risk models, leading to perverse incentives where institutions might align with higher, less prudent risk profiles, thus undermining the overall sensitivity to macroprudential risk.

- Systemic Risk Buffers and Countercyclical Buffers: Systemic Risk Buffers (SyRBs) and Countercyclical Capital Buffers (CCyBs) lack the precision needed to tackle specific macroprudential risks associated with high-LTV loans. Although these buffers are designed to enhance resilience during periods of excessive credit growth, they do not effectively differentiate between high-risk and low-risk mortgage segments. The targeted risk-weight floor approach directly influences institutional risk-taking by pricing in the macroprudential costs linked to high-LTV exposures, making it a more effective tool for mitigating systemic vulnerabilities.

Broader Implications of the Macroprudential Risk Strategy

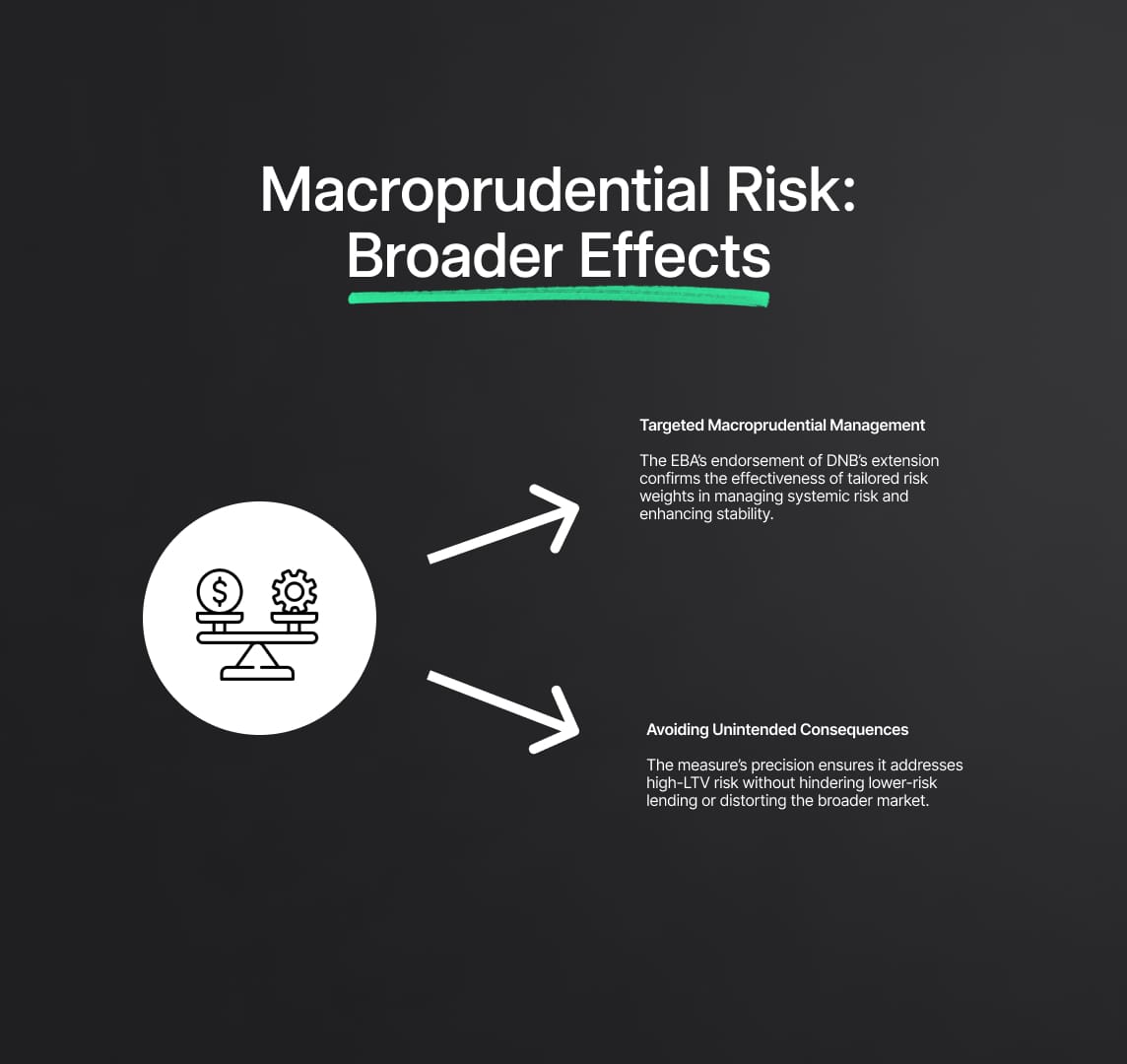

- Consistency with Macroprudential Objectives: The EBA’s endorsement of DNB’s extension of macroprudential measures underscores the effectiveness of targeted, data-driven tools in managing systemic risks. By differentiating risk weights according to LTV ratios, these measures serve as a precise mechanism to curb excessive risk-taking, ensuring that capital requirements align with the actual macroprudential risk profile of mortgage exposures. This approach not only bolsters financial stability in the Netherlands but also sets a benchmark for effectively managing macroprudential risk through carefully tailored interventions.

- Avoidance of Unintended Market Consequences: By refining risk weights to accurately reflect the macroprudential risk inherent in high-LTV loans, the measure avoids the broad, often blunt impacts of less targeted regulatory instruments. This ensures that the macroprudential framework remains adaptable to the specific dynamics of the Dutch housing market, without imposing unnecessary constraints on lower-risk lending activities. The targeted approach mitigates systemic risk without stifling healthy market operations, supporting a balanced and resilient financial environment.

Reduce your

compliance risks