Market Abuse Regulation (MAR) Compliance Guide

The Market Abuse Regulation (MAR), Regulation (EU) No 596/2014, ensures EU financial market integrity and investor protection by addressing insider dealing, unlawful information disclosure, and market manipulation.

Introduction

Introduction to Market Abuse Regulation (MAR)

Market Abuse Regulation (MAR) is the primary framework that preserves market integrity across the European Union and the United Kingdom. In force since 3 July 2016, MAR replaced the Market Abuse Directive (MAD) to create a single rule-set against insider dealing, unlawful disclosure of inside information and market manipulation. By harmonising these standards, MAR helps protect investors, reduce trading costs and promote transparent, efficient capital markets.

Compliance teams on both sides of the Channel must master MAR’s technical requirements to avoid hefty fines, criminal liability and reputational damage. This guide explains the EU and UK regimes, highlights recent enforcement actions, and outlines practical steps for building a resilient compliance programme rooted in strong governance.

What Is MAR and Why It Matters

Regulation (EU) 596/2014 applies directly in every EU member state and, post-Brexit, has been on-shored into UK law with amendments overseen by the Financial Conduct Authority (FCA). Its goal is simple: deter any conduct that distorts price formation or erodes investor confidence.

Who is in scope?

- Issuers of securities listed or traded on an EU or UK venue

- Directors and senior managers with access to inside information

- Intermediaries such as brokers, advisers and other market participants

A single breach, whether intentional or caused by a control failure, can trigger multi-million-euro penalties, criminal prosecution and lasting reputational harm. Conversely, demonstrating robust MAR compliance showcases effective governance and strengthens credibility with regulators, investors and clients alike.

Regulatory Scope of Market Abuse Regulation (MAR)

Market Abuse Regulation (MAR) casts a deliberately wide net: it targets behaviours and financial instruments, not a particular class of person or firm. As a result, any individual or entity—from retail day-traders to listed issuers—can breach MAR if their conduct distorts price formation or undermines investor confidence.

1. Financial Instruments in Scope

- Primary markets: shares, bonds and other securities admitted to trading on an EU or UK regulated market.

- Secondary venues: instruments traded on multilateral trading facilities (MTFs) or organised trading facilities (OTFs).

- Derivatives and linked contracts: options, futures, contracts for difference (CFDs), credit-default swaps and any contract whose price depends on an in-scope instrument.

- Emission allowances and their derivatives.

- SME Growth Markets: a sub-category of MTFs designed for small and mid-cap issuers; MAR applies with proportionate obligations to encourage capital-raising on these venues.

2. Geographical Reach

MAR’s prohibitions apply world-wide if the conduct affects the price of an instrument admitted to trading in the EU or UK.

Example: an insider trade executed in Singapore on shares listed in Frankfurt will still violate EU MAR; the same logic applies to UK MAR for London-listed securities.

3. Who Must Comply

| Stakeholder | Key MAR Duties |

|---|---|

| Issuers and their boards | Disclose inside information promptly, maintain insider lists, implement sound disclosure controls. |

| Investment firms / intermediaries | Monitor, detect and report suspicious orders and transactions (STORs); maintain robust surveillance systems. |

| Investors & traders | Refrain from insider dealing, unlawful disclosure or market manipulation—liability can extend to family members and social-media tippees. |

| Third-party professionals (lawyers, auditors, advisers) | Safeguard any inside information received in the course of their work; misuse is punishable. |

A single breach, intentional or accidental, can trigger administrative fines that run into millions of euros, criminal prosecution and lasting reputational harm.

4. EU vs UK MAR After Brexit

Since 31 December 2020, two parallel regimes exist:

- EU MAR (Regulation 596/2014) continues unchanged within the Union.

- UK MAR is the on-shored version, administered by the Financial Conduct Authority (FCA).

Companies with dual listings (e.g., London Stock Exchange and an EU venue) must satisfy both frameworks simultaneously. Although the rulebooks were identical at the point of separation, the EU and UK are now pursuing incremental reforms—for example, different thresholds for insider-list exemptions and divergences in regulatory reporting format—so compliance teams need ongoing horizon-scanning to keep policies aligned.

Core Offences Under Market Abuse Regulation (MAR)

Market Abuse Regulation (MAR) targets three headline offences that threaten price integrity and investor confidence. Every compliance programme should be built around detecting and preventing these behaviours.

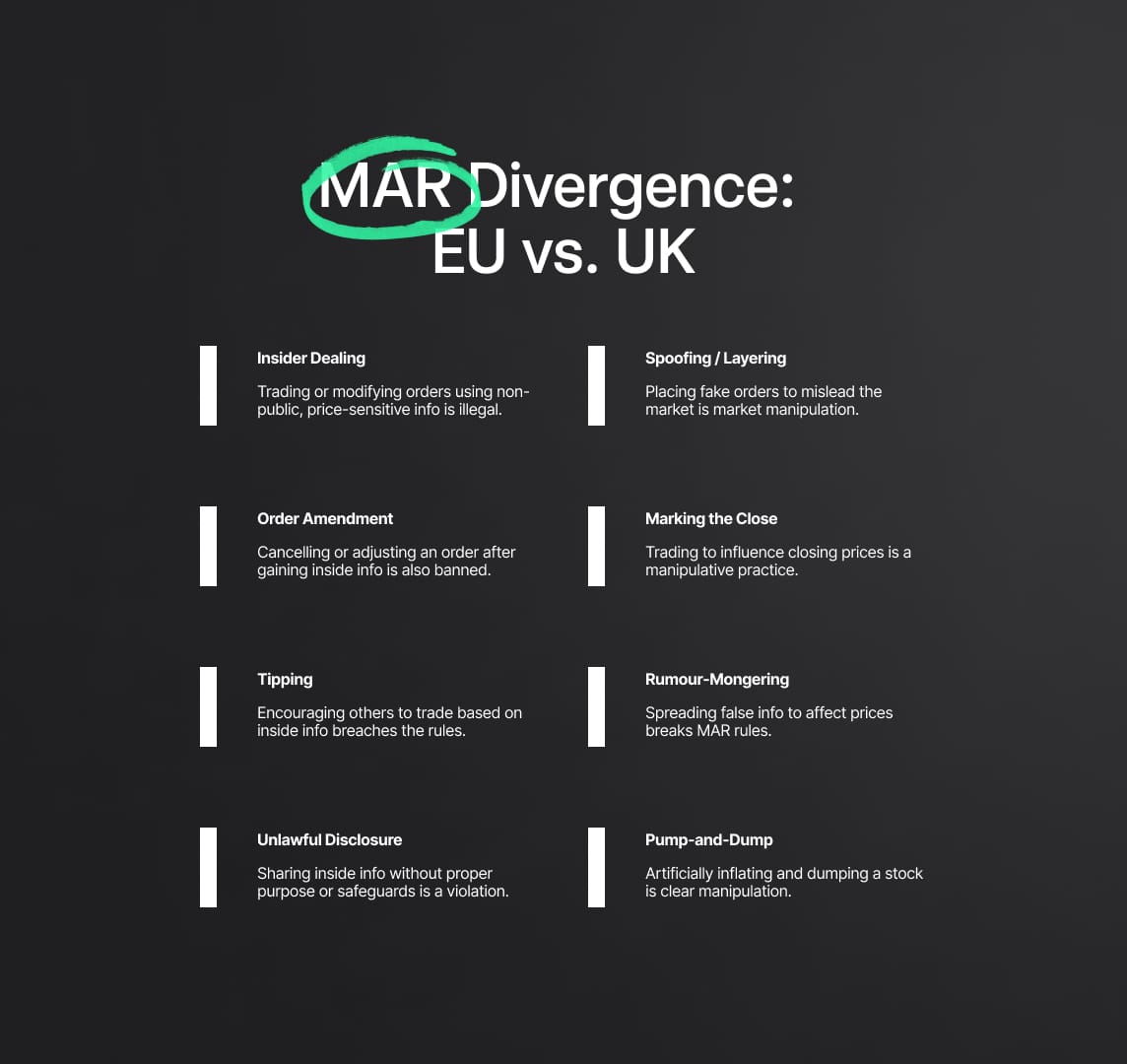

1 | Insider Dealing (Insider Trading)

Trading, amending or cancelling an order while in possession of inside information, information that is precise, non-public and price-sensitive, is strictly prohibited. The ban covers:

- Direct trading: buying or selling securities, emission allowances or related derivatives.

- Order amendment: changing or cancelling an order after learning inside information to limit loss or boost gain.

- Tipping: encouraging or inducing another person to trade on inside information.

Examples of inside information

| Category | Illustrative scenarios |

|---|---|

| Corporate events | Unpublished earnings, merger talks, management changes |

| Regulatory milestones | Pending drug-trial results, licence approvals |

| Macroeconomic data | Imminent rate-setting decisions relevant to bonds or FX |

Example: A biotech executive who purchases shares before disclosing successful Phase III results, or tips a friend who then trades, commits insider dealing.

2 | Unlawful Disclosure of Inside Information

Possessing inside information imposes a duty of confidentiality. Disclosing it to any unauthorised person, whether a colleague, family member or journalist, breaches MAR, unless the disclosure is:

- Made in the normal exercise of employment and

- Subject to appropriate safeguards (e.g., market-sounding procedures with written records).

Example: A director casually revealing an upcoming profit warning over dinner, even without any trade, violates the unlawful-disclosure provisions.

3 | Market Manipulation

Any act that gives false or misleading signals about the supply, demand or price of an instrument, or secures an abnormal price level, constitutes manipulation. Common red flags include:

- Spoofing / layering: placing orders with no intent to execute to mislead others.

- Marking the close: executing trades near market-close to influence the official price.

- Rumour-mongering: disseminating false information via media or social networks.

- Pump-and-dump rings: coordinating to inflate a small-cap price before dumping holdings.

Attempted manipulation is punishable even if the scheme fails to move the market.

Example: A trader submits large buy orders moments before the close to elevate a stock’s benchmark price that determines a derivatives payoff, clearly manipulation under MAR.

Why These Offences Matter for Compliance

MAR empowers EU and UK regulators to impose multi-million-euro administrative fines and, in severe cases, criminal sanctions. Effective controls against insider dealing, unlawful disclosure and market manipulation are therefore mission-critical to:

- Protect market integrity and client trust.

- Avoid financial and reputational damage.

- Demonstrate strong governance.

Issuers, intermediaries and individual insiders alike bear responsibility for proactive prevention, through surveillance, insider-list management, staff training and clear escalation pathways, discussed in the next section on compliance obligations.

EU MAR vs UK MAR: How the Two Regimes Now Differ

Although the Market Abuse Regulation (MAR) began as a single EU-wide framework, Brexit has left firms juggling EU MAR and UK MAR, two rulebooks with shared DNA but growing divergences.

1 | EU MAR Framework

- Legal basis: Regulation (EU) 596/2014 applies directly in every Member State, supplemented by the Criminal Sanctions for Market Abuse Directive (CSMAD) for serious offences.

- Supervision & enforcement: Each national competent authority (e.g., AMF in France, BaFin in Germany) polices compliance, while ESMA issues Q&As and coordinates cross-border cases.

- Enforcement record: ESMA’s 2022 annual report logged 366 sanctions worth €54 million across the bloc, proof that regulators actively wield their powers.

2 | UK MAR Framework

- On-shored law: The European Union Withdrawal Act 2018 preserved MAR in UK legislation, modified by the Market Abuse (Amendment) (EU Exit) Regulations 2019. The FCA is the sole enforcement body.

- Continued alignment: Insider dealing, unlawful disclosure, market manipulation, insider-list duties and Suspicious Transaction & Order Reports (STORs) remain substantively unchanged.

- Independent tweaks: Because UK MAR now sits outside EU law, London can refine its regime without Brussels’ approval.

3 | Key Divergences Compliance Teams Must Track

| Compliance topic | EU MAR rule | UK MAR variation | Why it matters |

|---|---|---|---|

| PDMR trade reporting | PDMRs notify and issuers disclose within 3 business days of the transaction. | PDMRs notify within 3 working days; issuers then get 2 more working days to publish. | Adds breathing room for UK issuers but not EU-listed companies. Dual-listed firms must respect both clocks. |

| Insider-list responsibility | Primarily on the issuer; third-party advisers’ duties less explicit. | Obligation extends to any person acting on the issuer’s behalf (e.g., law firms, PR agencies). | Law firms and consultants must maintain their own lists and cooperate with issuers. |

| Criminal sentences | Most Member States cap insider-dealing jail terms at 4–8 years. | Raised to 10 years under the Financial Services Act 2021. | Signals the UK’s tougher stance and aligns penalties with fraud and money-laundering offences. |

4 | Emerging Policy Drift

- EU Listing Act (in force 4 Dec 2024): Amends MAR to ease disclosure burdens—e.g., tighter conditions for delaying inside-information release, with a major timing change slated for mid-2026.

- UK “Edinburgh Reforms”: A wider capital-markets package that may recast UK MAR, but no concrete changes have been legislated yet.

Result: compliance manuals that once mirrored each other will need jurisdiction-specific chapters as the gap widens.

Take-aways for Cross-Border Firms

- Map your venue footprint: Securities admitted to an EU venue trigger EU MAR even if traded elsewhere; UK-listed instruments invoke UK MAR, often both.

- Dual rulebook surveillance: Configure trade-surveillance systems to apply the strictest obligation where deadlines or definitions diverge.

- Update policies yearly: Track ESMA Q&As, FCA Market Watch newsletters and pending reforms to stay ahead of incremental changes.

- Train frontline staff: Emphasise jurisdiction-specific timelines (e.g., PDMR reporting) and heightened UK criminal exposure.

Compliance Obligations Under the Market Abuse Regulation (MAR)

For compliance teams, Market Abuse Regulation (MAR) compliance hinges on putting active controls in place to prevent, detect and report market-abuse risks, not merely steering clear of prohibited behaviours.

Timely Disclosure of Inside Information (Article 17)

Issuers must release price-sensitive information “as soon as possible” via a regulatory news service. Disclosure may be delayed only if three conditions hold: immediate release would harm a legitimate interest, confidentiality can be safeguarded, and no one trades on the information. Boards should minute every delay decision, keep supporting evidence, and notify the regulator once the news is published. A standing “inside-information committee” with clear playbooks for assessment, delay, and record-keeping helps avoid enforcement action for late or improper disclosure.

30-day closed periods: PDMRs (directors and senior managers) are barred from trading for thirty days before annual or interim results. Compliance should maintain blackout calendars and pre-clearance procedures so senior executives never trade, nor appear to trade, on earnings information.

Insider Lists and Confidentiality Controls

Every issuer must keep an up-to-date insider list recording who has access to inside information, why, and when. Under UK MAR this duty also reaches advisers such as law firms and auditors. Good practice includes:

- automatic prompts to add or remove names as projects start and finish

- written acknowledgments from insiders confirming they understand trading and tipping bans

- safeguards, encryption, code names, need-to-know access and information barriers, to prevent leaks

From 2028, issuers will also file public disclosures to the European Single Access Point (ESAP) on the day of release, so systems should be upgraded now.

Trade Surveillance and STOR Reporting (Article 16)

Banks, brokers and trading venues must monitor orders and trades, then file a Suspicious Transaction & Order Report (STOR) without delay whenever there are reasonable grounds to suspect insider dealing or manipulation, even if no profit was made. Technology is critical, but governance is decisive:

- calibrate alerts to business-specific patterns (e.g., layering or pre-announcement price spikes)

- investigate promptly, document findings, and escalate when in doubt

- limit knowledge of filed STORs to curb the risk of tipping off wrongdoers

Regulators act where firms fall short. In 2025 the Central Bank of Ireland fined Cantor Fitzgerald Ireland €452,790 for missing numerous STORs over six years. Since 2018, the UK FCA has levied over £19.5 million in fines for surveillance failures—often for poorly tuned alerts or untrained reviewers.

Common Surveillance Pitfalls (and How to Fix Them)

- Over-broad or under-tuned alerts drown reviewers in false positives or miss red flags. Run periodic model-risk reviews and back-testing.

- Lack of skilled staff means alerts go uninvestigated. Provide ongoing MAR-focused training and documented escalation paths.

- Poor documentation undermines later defence. Maintain a complete audit trail from alert through decision, including rationale for “no-STOR” conclusions.

Managers’ Transactions (PDMR Dealings)

Under Market Abuse Regulation (MAR), senior executives and directors—Persons Discharging Managerial Responsibilities (PDMRs)—plus their closely associated persons must notify both the issuer and the competent authority of any trade in the company’s shares, debt or related derivatives.

- Deadline: three business days under EU MAR; three working days under UK MAR.

- Issuer disclosure: the company must publish the trade shortly after receiving notice (within two working days in the UK).

- De-minimis exemption: no report is needed for annual dealings below €5,000 in the EU (a rise to €20,000 is under discussion).

Director-dealing reports bolster market transparency; missing a deadline is a strict-liability breach that can trigger fines. A practical control framework combines:

- a dealing code that blocks trading in 30-day closed periods and requires pre-clearance;

- automated reminders keyed to results-season calendars;

- an insider-holdings register so Compliance can track cumulative activity.

Timely communication with PDMRs, especially when trading windows reopen, prevents innocent oversights from becoming enforcement cases.

Market Soundings Safe Harbour

Article 11 MAR lets issuers and banks “sound out” selected investors before launching block trades or new issues, but only if a strict script is followed:

- Evaluate whether the information is inside information.

- Obtain the investor’s consent to receive it and warn them of insider status and trading prohibitions.

- Record and store every communication—for at least five years—on recorded lines or in written minutes.

Deviating from these steps removes the safe harbour and re-classifies the contact as unlawful disclosure. Firms should keep concise checklists, train deal teams and audit calls to ensure protocols are watertight; regulators have fined brokers for lax processes that led to leaks.

Investment Recommendations and Information Dissemination

Anyone who produces or circulates investment recommendations, analyst notes, newsletters, even monetised blog posts, falls under the MAR rules on fair presentation and conflict disclosure. Key expectations:

- clearly separate analysis from trading functions (reinforced by MiFID II “Chinese wall” requirements);

- flag material interests such as holdings, market-making roles or investment-bank mandates;

- avoid sensational language that could mislead investors.

Social-media commentators who post trade ideas for commercial gain should likewise disclose positions and stick to verifiable facts to avoid inadvertent market manipulation.

Whistleblowing and Compliance Culture

Regulators now host confidential hotlines, but MAR expects firms to foster their own speak-up channels. An effective whistleblowing framework:

- protects employees from retaliation;

- channels market-abuse concerns to an independent function;

- logs, investigates and remediates issues promptly.

Embedding these elements in an insider-trading policy, supported by regular, role-specific training, creates a culture where employees recognise, escalate and mitigate market-abuse risks before regulators step in.

Enforcement and Penalties: How Market Abuse Regulation (MAR) Is Applied in the EU and UK

Regulators on both sides of the Channel now treat market abuse regulation (MAR) breaches as a top-tier enforcement priority, using a blend of administrative fines, supervisory actions and, where the facts warrant, criminal prosecutions.

Administrative Sanctions in the European Union

Each EU Member State empowers its own competent authority (AMF in France, CONSOB in Italy, CNMV in Spain, etc.) to police MAR. The harmonised rule-set provides a common sanctioning toolkit:

- Fines up to €5 million for individuals and €15 million, or 15 % of annual turnover, for firms.

- Ancillary measures such as profit disgorgement, trading bans, asset freezes and director disqualifications.

Enforcement is vigorous and growing: the latest ESMA statistics show 366 MAR sanctions in a single year, totalling more than €54 million across the bloc. France routinely tops the activity tables, but Italy and Spain have also issued multi-million-euro penalties for pump-and-dump schemes and other forms of manipulation.

Enforcement Landscape in the United Kingdom

The UK Financial Conduct Authority (FCA) retained the EU standard but wields its own, essentially unlimited, fining powers. Market abuse featured in 26 % of all FCA cases closed in 2022-23, and several hundred investigations remained open through 2023. Recent trends include:

- Firm-level control failings: the FCA fines banks and brokers whose trade-surveillance or disclosure controls fall short, even when no insider dealing is proven.

- Thematic scrutiny: the regulator samples STOR quality, insider-list maintenance and timeliness of price-sensitive disclosures, publicising shortcomings in its Market Watch newsletters.

Because UK Listing Rules embed MAR obligations, a disclosure lapse can attract penalty under two parallel regimes.

Case in Point: Control Failure, Not Insider Trading

Cantor Fitzgerald Ireland Ltd (2025)

Over six years, the firm’s own systems flagged numerous suspicious orders, yet few were reported. The Central Bank of Ireland imposed a €452,790 fine for breaching Article 16(2) MAR—proof that regulators expect firms to serve as the first line of defence by filing Suspicious Transaction and Order Reports (STORs) promptly and documenting every decision.

Take-aways for Compliance Teams

- Match EU and UK thresholds: keep sanction ceilings and enforcement trends on the radar when sizing potential exposure.

- Prioritise controls as much as conduct: regulators penalise weak surveillance, poor insider-list hygiene and late disclosures even where no abuse occurs.

- Audit STOR processes: ensure alerts are calibrated, investigations documented and every reasonable suspicion reported without delay.

- Monitor regulator messaging: ESMA’s annual enforcement report and the FCA’s Market Watch give clear signals on evolving expectations.

A robust, well-documented MAR compliance framework is therefore not optional; it is the surest defence against the escalating penalty landscape governing market abuse regulation across Europe and the United Kingdom.

Criminal Prosecution Under Market Abuse Regulation (MAR)

Administrative fines deter most misconduct, yet the gravest breaches of market abuse regulation, deliberate insider dealing or sophisticated market manipulation, can trigger full-scale criminal proceedings.

Dual Criminal Tracks

- United Kingdom – Insider dealing has carried criminal liability since the Criminal Justice Act 1993; market-manipulation offences sit in the Financial Services Act 2012. The Financial Conduct Authority (FCA) chooses whether to pursue a civil fine, a criminal charge, or both. Maximum prison sentences were lifted to 10 years, aligning market abuse with fraud and money-laundering penalties.

- European Union – Criminal enforcement depends on national law. Many states, such as France, Italy and Spain, prosecute insider trading alongside MAR’s administrative regime, while others rely chiefly on regulator fines. Cooperation among Member-State prosecutors—and with the UK post-Brexit—remains close.

Rising UK Convictions

The FCA’s shift to “assertive action” is evident: in fiscal year 2023/24 it secured 11 criminal convictions for insider dealing, up from a single conviction the year before. Recent examples include:

- Five-person conspiracy (charges filed 2023) – alleged co-ordinated trading across multiple stocks; trial scheduled for 2024.

- Two traders prosecuted October 2024 – accused of £110 000 profit from insider dealing in four shares, illustrating that even mid-five-figure gains draw criminal scrutiny.

- Mohammed Zina (2022 conviction) – former analyst jailed after exploiting confidential M&A information over 17 months.

A 2019 UK case—where a bank compliance officer fed deal tips to a day-trader friend, netting £1.4 million—shows that gatekeepers themselves face jail when controls are subverted.

Continental Trends

Italy has jailed participants in insider-trading rings that reached into the Vatican; France frequently imposes multi-year trading bans alongside custodial sentences. Energy-market manipulation under REMIT, and forthcoming crypto-asset rules under MiCA, reflect regulators’ willingness to extend criminal treatment to evolving asset classes.

Penalties and Industry Fallout

Convicted individuals risk:

- Imprisonment (up to 10 years in the UK; similar terms in several EU states)

- Confiscation of illicit gains

- Lifetime industry bans and indelible reputational damage

Firms implicated in the wrongdoing, or found with inadequate controls, face multimillion-euro fines and supervisory restrictions.

Best-Practice Blueprint for Market Abuse Regulation (MAR) Compliance

Robust MAR compliance blends written controls, technology, training and culture. The guidelines below preserve every regulatory nuance while presenting them in a streamlined structure.

1. Write and Maintain a Living Insider-Trading Policy

A credible policy should:

- Define inside information precisely and prohibit trading or tipping until disclosure.

- Codify pre-clearance for PDMR and staff trades, incorporating the 30-day closed-period rule and any EU or UK threshold changes (e.g., a future EU €20 000 de-minimis for PDMR reports).

- Map information-barrier controls, code names, “need-to-know” access, project encryption, and set out breach-reporting lines.

- Undergo annual review so new instruments (cryptoassets under MiCA, for example) or altered EU/UK deadlines flow straight into procedures.

2. Deliver Tailored, Tested Training

Hold sessions on hire and at least yearly. Adapt the syllabus:

- Front-office teams: patterns of manipulation, STOR triggers, order-book abuse.

- Executives: timely disclosure duties, PDMR notification deadlines (three business vs three working days).

- Support staff: how to recognise and quarantine inside information.

Embed quizzes or attestations to evidence understanding and foster a culture where market integrity is part of professional identity.

3. Deploy Surveillance That Works

Modern MAR systems must cover every asset class your firm touches and reach into communications, voice, email, chat, while respecting privacy law. Calibrate alerts to strike the right balance between false positives and missed risk. Document tuning cycles; regulators increasingly ask how alerts are set, not just whether you bought software.

4. Perfect the STOR Lifecycle

Create a low-friction path from alert to Suspicious Transaction and Order Report:

- Initial triage by surveillance analysts.

- Documented investigation with clear rationale for each decision.

- Escalation to senior compliance for borderline calls.

- Prompt filing where suspicion remains, even for failed attempts at abuse.

Schedule periodic “look-back” reviews of unreported alerts; gap-analysis after the Cantor Fitzgerald fine shows regulators expect it.

5. Master Insider-List Governance

Maintain real-time, project-level lists noting: identity, role, access timestamp, and when information ceases to be inside information. Under UK MAR, advisers must keep their own lists, capture that duty in engagement letters. Email tagging, auto-notifications when insiders are “cleared,” and signed acknowledgements demonstrate tight control.

6. Control Market Soundings and Wall-Crossings

Follow Article 11 safe-harbour steps every time:

- Assess materiality → obtain recipient consent → give statutory warnings → record the call.

Keep five-year archives and audit samples. If you receive a sounding, flag Compliance immediately so trading can be restricted.

7. Enforce Closed-Period Blackouts

Align blackout calendars to reporting timetables; notify PDMRs at both start and end. Document any MAR-permitted exceptions (hardship sales, certain share-plan exercises) and secure legal sign-off.

8. Track Regulatory Guidance Proactively

Monitor ESMA Q&As, FCA Market Watch newsletters and consultation papers. Incorporate updates, such as evolving inside-information definitions for prolonged processes, before they become exam questions in an inspection.

9. Prepare an Incident-Response Playbook

When leaks or rogue trades occur:

- Freeze the situation: halt trading, secure systems.

- Investigate quickly with Legal/Compliance and external counsel.

- Self-report if warranted; cooperative behaviour can halve penalties.

- Remediate through disciplinary action, system fixes and follow-up training.

10. Foster a Speak-Up Culture

Confidential hotlines, anonymous web portals and an unwavering anti-retaliation stance turn employees into early-warning sensors. Acting on near-misses proves to regulators.

Real-World Case Studies: How Market Abuse Regulation (MAR) Plays Out

Examining enforcement files helps translate MAR’s black-letter law into practical lessons. The two examples below, one continental, one British, show how market abuse regulation is applied, the penalties it attracts and the red-flags compliance teams should monitor.

Case Study 1: Insider Dealing Through Tipping: the AirTech Merger Leak (EU)

In 2023, the securities regulator of Country X spotted unusual buying in AirTech Co. shares days before the aerospace group announced a transformational merger. Trade-surveillance algorithms had highlighted two retail accounts that had never previously shown interest in the sector but were suddenly accumulating stock.

The investigation revealed a simple chain of misuse:

- Source of the leak – A senior AirTech engineer learned confidentially about the pending merger (clearly “inside information” under Article 7 MAR).

- Tipping – He passed the news to a friend, who bought shares and tipped a third associate.

- Profit realisation – When the deal became public, the price jumped 20 % and both tippees sold, realising about €200 000.

Outcome under EU MAR:

- Engineer: €500 000 fine plus a five-year director ban for unlawful disclosure.

- Each tippee: disgorgement of profit and a €300 000 administrative penalty for insider dealing.

Key compliance lesson: leaks often originate well below the C-suite. Insider lists should cover non-executive staff with access to sensitive projects, and surveillance must review all spikes in the issuer’s stock, even activity by accounts with no prior history, against the insider list timeline.

Case Study 2: Social-Media Pump-and-Dump: XYZ Plc (UK)

A group of retail traders quietly built positions in AIM-listed XYZ Plc at low prices. They then launched a coordinated hype campaign on Twitter and an online forum, falsely claiming to have “inside knowledge” of a forthcoming multi-million-pound contract that would “triple the share price.” The rumour went viral; volume and price surged. Within 48 hours the orchestrators dumped their stock at a hefty profit, and the price collapsed once the claims were exposed as fiction.

The Financial Conduct Authority treated the conduct as market manipulation under UK MAR (dissemination of false or misleading information):

- Ringleader: £1 million fine and lifetime trading ban.

- Co-conspirators: fines of £100 000 - £200 000 and trading bans of five to ten years.

Key compliance lesson: modern market abuse often unfolds online. Issuers should monitor social-media chatter for false rumours that could distort price formation, and intermediaries must flag unusual order-flow spikes linked to digital hype. For individuals, anonymity on social platforms offers no shelter, digital forensics can and will link aliases to real identities.

Conclusion

Market Abuse Regulation, both in the EU and UK, forms a critical compliance area for anyone involved in the financial markets. By outlawing insider trading, improper disclosures, and manipulative behaviors, MAR seeks to ensure that markets remain fair and trustworthy for all participants. The regulatory frameworks in the EU and UK are highly aligned in purpose, though minor divergences are emerging as each jurisdiction refines its regime. Compliance professionals must keep a finger on the pulse of these changes, ensure robust internal controls are in place, and foster a corporate culture that prioritizes integrity over short-term gains.

The real-world cases and enforcement trends discussed illustrate that regulators have both the will and the tools to clamp down on market abuse – whether through multi-million euro fines, industry bans, or even jail sentences. In this environment, precision and proactivity in compliance are non-negotiable. Firms that invest in strong compliance systems (surveillance technology, staff training, clear policies) not only mitigate their risk of regulatory action, but also enhance their reputation as trustworthy, well-governed institutions. Meanwhile, firms that neglect these duties face not just legal penalties but also erosion of client and investor trust.

In summary, MAR compliance is about safeguarding market integrity. By adhering to the rules and embracing best practices, financial firms and their professionals demonstrate expertise, authority, and trustworthiness – qualities that are invaluable in the eyes of regulators, customers, and search engines alike. As the regulatory landscape evolves (with new guidelines, technologies, and cross-border considerations), staying informed and agile is key. Ultimately, a strong grasp of the Market Abuse Regulation and a commitment to ethical conduct will position firms to thrive in a fairer, more transparent financial marketplace.

Frequently Asked Questions on the Market Abuse Regulation (MAR)

1. Does the Market Abuse Regulation still apply in the UK after Brexit?

Answer: Yes. The United Kingdom retained the rule-set by “on-shoring” it as UK MAR, enforced by the Financial Conduct Authority. UK MAR mirrors the EU text as it stood on 31 December 2020; however, small divergences have already appeared (for example, the UK gives issuers two extra working days to publish PDMR trades, whereas the EU has introduced broader Listing Act reforms). Firms active in both areas must meet each jurisdiction’s nuances, but day-to-day obligations—insider-dealing ban, market-manipulation ban, disclosure duties—remain largely identical.

2. What penalties can follow a MAR breach?

Answer: Sanctions escalate quickly. Administratively, regulators can fine individuals up to €5 million and firms up to €15 million or 15 % of annual turnover; they may also disgorge profits, freeze assets or issue director bans. In many EU states and in the UK, serious insider dealing or manipulation is a criminal offence that carries custodial sentences of up to 10 years and unlimited fines. A recent uptick in UK criminal cases, eleven convictions in a single year, shows prosecutors’ willingness to jail offenders.

3. What counts as “inside information”?

Answer: Information must be (i) precise, (ii) non-public and (iii) price-sensitive, meaning a reasonable investor would use it when making a trading decision. Examples: unpublished earnings, a confidential merger, a regulator’s forthcoming product approval or an imminent bond-rating downgrade.

4. Can issuers ever delay disclosing inside information?

Answer: Yes, but only if three strict conditions are met: immediate release would harm the issuer’s legitimate interests; confidentiality can be maintained; and no insider deals on the information. The decision must be documented, and the regulator informed once disclosure occurs.

5. How quickly must PDMRs report their own trades?

Answer: Under EU MAR: within three business days of the transaction, and the issuer must publish the notice within the same window. Under UK MAR: PDMRs still have three working days, but issuers receive an extra two working days to publish.

6. Who is responsible for filing Suspicious Transaction and Order Reports (STORs)?

Answer: Any investment firm, trading venue or broker that detects a reasonable suspicion of insider dealing or manipulation in an order or trade it handles must file a STOR to its national regulator without delay, even if the suspicious activity was unsuccessful.

7. Do MAR rules cover crypto-assets?

Answer: Only if the token is already classified as a financial instrument under EU or UK securities law. The forthcoming EU MiCA regime will introduce a parallel market-abuse framework for many crypto-assets not caught by MAR.

8. How do market soundings stay within the law?

Answer: The disclosing party must: (i) assess materiality; (ii) gain the investor’s consent to be “wall-crossed”; (iii) issue statutory warnings about insider status; and (iv) record the conversation. Follow these steps and the sounding enjoys MAR’s safe harbour.

9. Our surveillance system flags many false positives: should we still report?

Answer: Regulators prefer over-reporting to silence. If, after documented analysis, reasonable grounds for suspicion remain, file the STOR. Failure to report is itself a breach, even if no abuse ultimately occurred.

10. Could a social-media post trigger a MAR investigation?

Answer: Absolutely. Spreading false or misleading statements that influence a listed security’s price is market manipulation, whether the medium is a press release, a WhatsApp chat or a viral tweet. Regulators now employ digital-forensics teams to trace anonymous accounts to real individuals.

Reduce your

compliance risks