MiFIR/MiFID Regulation: AFME on Implementation Challenges

AFME supports ESMA’s MiFIR and MiFID regulations, tailored bond transparency, fair CTP standards, and consistent market data pricing to ensure balanced market stability and fair access for all participants.

AFME (Association for Financial Markets in Europe) has provided a detailed response to the European Securities and Markets Authority (ESMA), highlighting the challenges and complexities of implementing MiFIR regulation (Markets in Financial Instruments Regulation) and MiFID regulation (Markets in Financial Instruments Directive). AFME’s insights focus on critical issues such as Bond Transparency, Consolidated Tape Provider (CTP), and Reasonable Commercial Basis. Emphasizing the need for a carefully balanced approach within MiFIR and MiFID regulations, AFME advocates for data-driven transparency standards that maintain market stability while addressing the practical realities of trading, particularly for less liquid assets.

Source

[1]

The Role of MiFIR and MiFID in European Financial Markets

MiFIR and MiFID regulations are crucial in shaping the European financial landscape. MiFID II, the latest iteration of MiFID, together with MiFIR, aims to strengthen the regulatory framework by introducing robust measures that ensure market transparency, improve investor protection, and enhance the efficiency of financial markets. MiFIR specifically focuses on trading transparency and reporting requirements, while MiFID covers a broader scope, including market structure, investor protection, and organizational requirements for firms.

Key amendments introduced under the recent MiFIR regulation review include provisions for the establishment of CTPs and revised data reporting obligations to enhance market data transparency. The regulations now mandate a more stringent framework for data quality, transmission standards, and synchronisation of business clocks among trading venues and other market participants, aligning with international standards to ensure a seamless flow of information. These changes are aimed at removing existing obstacles that have hindered the development of a unified European consolidated tape, which is essential for a transparent and efficient market.

AFME's response to ESMA’s consultations highlights the complexities and challenges involved in implementing these regulations effectively, particularly in the context of bond market transparency, the development of consolidated tape solutions, and the enforcement of reasonable commercial basis for market data. AFME has underscored the importance of a well-calibrated approach that balances transparency with market functionality, particularly for instruments that trade infrequently or in lower volumes.

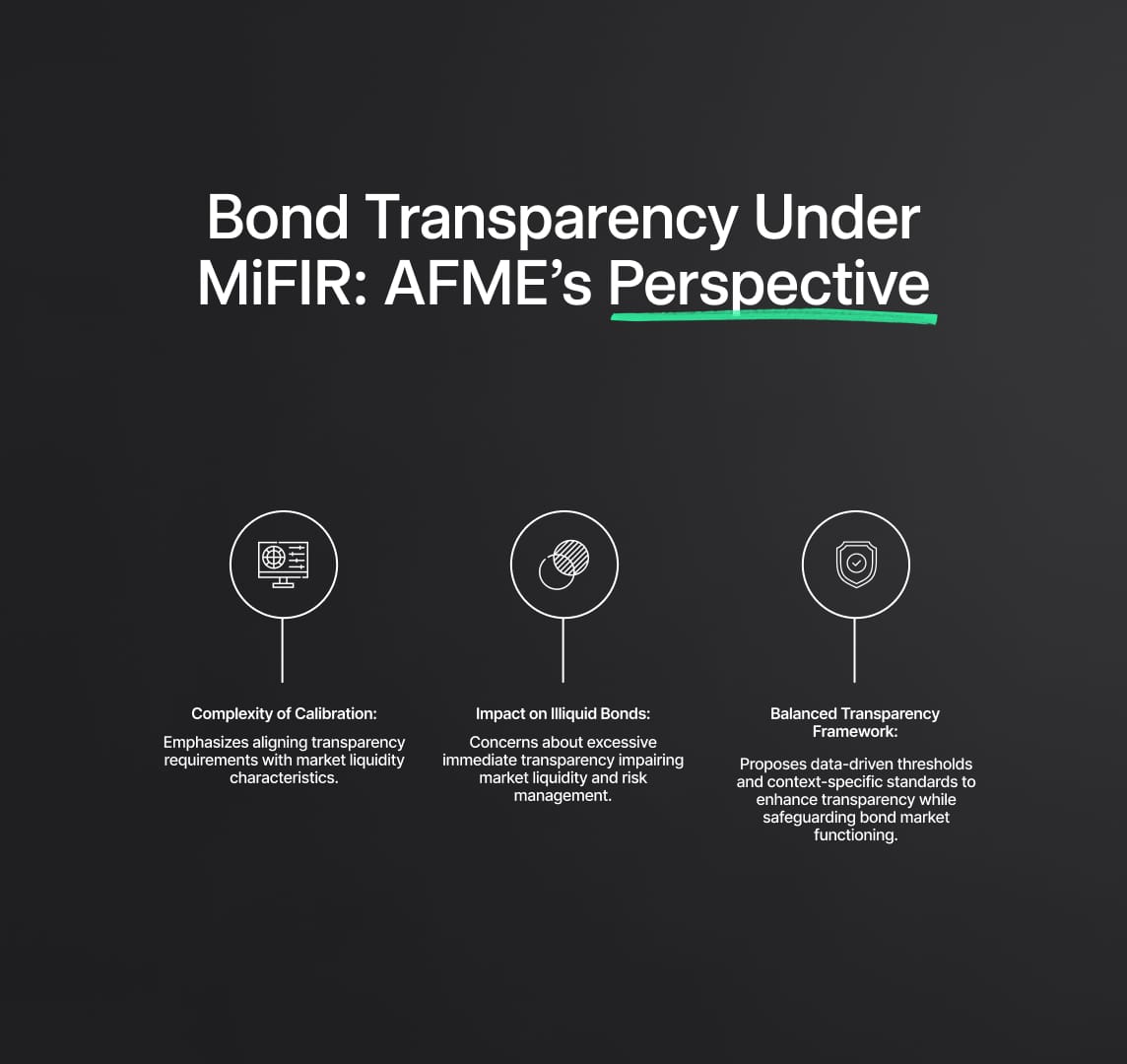

Bond Transparency Under MiFIR: AFME’s Perspective

One of the critical components of MiFIR regulation is the requirement to enhance transparency in bond markets, which is facilitated through the Regulatory Technical Standards (RTS 2). AFME has acknowledged the difficulty ESMA faces in calibrating appropriate transparency thresholds for bonds, especially in a market where liquidity varies significantly across different instruments. Under the revised MiFIR regulation, ESMA is tasked with defining clear criteria for data quality and the conditions under which market data must be published in near real-time, addressing challenges associated with delayed reporting and inconsistent data standards across various market participants.

Key Concerns:

- Complexity of Calibration: AFME appreciates ESMA's efforts to achieve an adequate level of transparency through data analysis. However, it emphasizes that similar scrutiny should be applied to assess the associated risks. AFME argues that transparency requirements should be aligned with market liquidity characteristics, avoiding a one-size-fits-all approach that could expose certain bonds, particularly illiquid ones, to undue risk. ESMA’s data quality measures and enforcement standards must ensure that transparency obligations do not inadvertently destabilize the market by compelling excessive disclosures that could impair trading activity.

- Impact on Illiquid Bonds: AFME is particularly concerned about the treatment of illiquid bonds under the current framework, which could lead to excessive immediate transparency. This, in turn, can impair market makers' ability to manage risk effectively, thereby reducing market liquidity. MiFIR’s requirement for near-real-time data transmission needs careful implementation, especially for bonds with lower trading frequency. AFME’s expanded analysis on Average Daily Volume (ADV) provides a more nuanced understanding of how long it typically takes for market makers to offload risk positions, highlighting the need for a more tailored approach that considers these dynamics.

The revised MiFIR regulation mandates ESMA to implement data transmission protocols that minimize latency, ensuring that data is transmitted “as close to real-time as technically possible.” For bonds, this requirement must be balanced against the need to protect market liquidity, particularly in scenarios where immediate transparency could expose market participants to adverse trading conditions. AFME’s proposed adjustments aim to strike this balance, advocating for data-driven thresholds that enhance market transparency while safeguarding the functioning of the bond market.

This focused analysis of the MiFIR regulation’s impact on bond market transparency underscores the broader regulatory challenge of implementing MiFID and MiFIR standards in a way that maintains market stability, promotes fair access to information, and avoids unintended consequences that could harm investor confidence and market efficiency.

Proposed Solutions:

Balanced Transparency Framework: AFME has proposed a refined framework that ensures high levels of immediate transparency while safeguarding the liquidity and competitiveness of bond markets. This approach aims to align with MiFIR’s objectives by carefully balancing transparency requirements with the practical realities of trading less liquid bonds. Specifically, MiFIR regulation mandates ESMA to develop detailed Regulatory Technical Standards (RTS) that define the scope and conditions under which bond market data should be disclosed. AFME emphasizes the need for these standards to be data-driven and context-specific, considering factors such as the Average Daily Volume (ADV) and the typical time for market makers to trade out of positions, thereby preventing the potential adverse impact of excessive transparency on illiquid bonds.

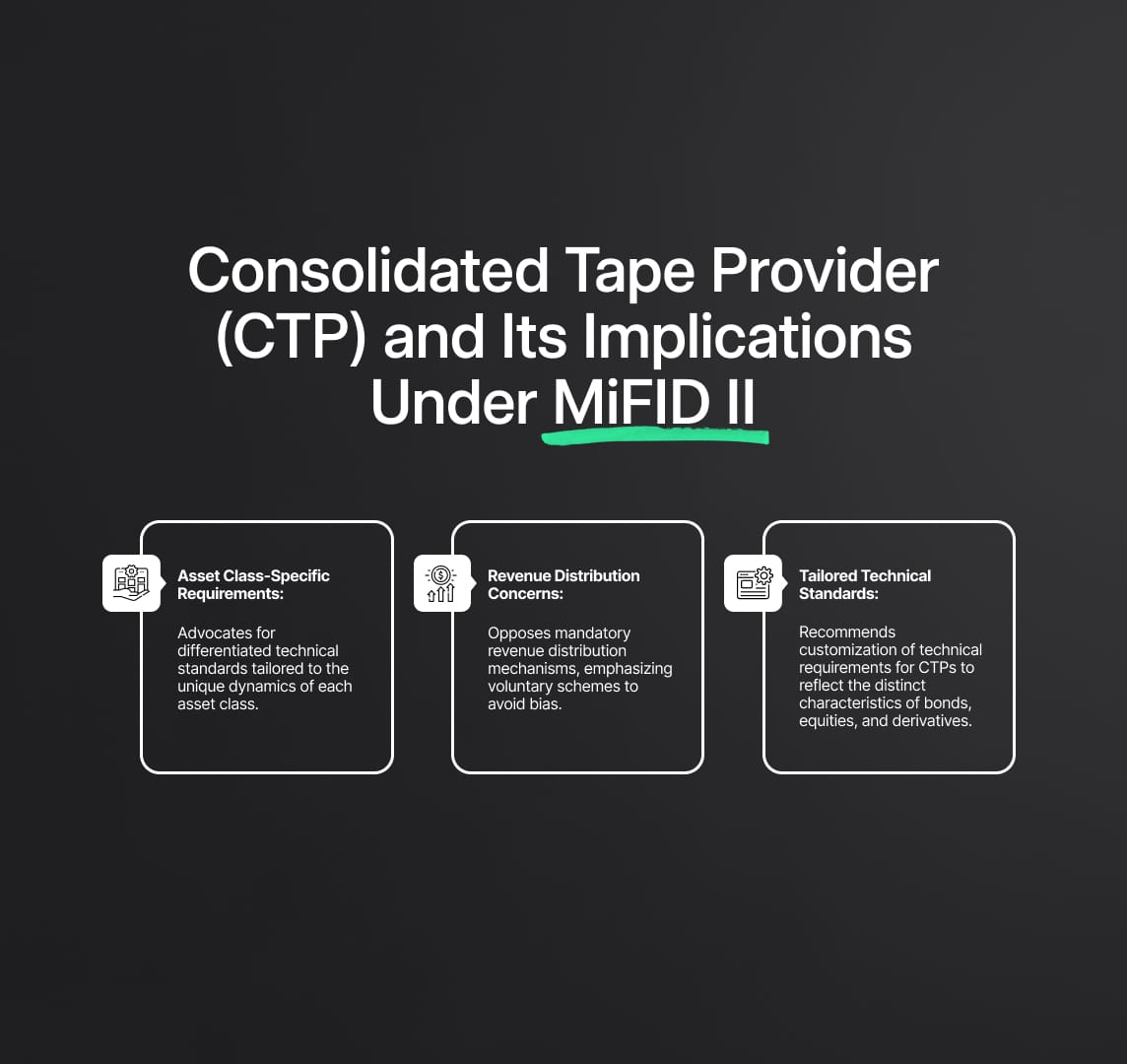

Consolidated Tape Provider (CTP) and Its Implications Under MiFID II

The concept of a Consolidated Tape Provider (CTP) is a significant aspect of MiFID regulation, aiming to consolidate market data across various asset classes, including bonds, equities, and derivatives. A CTP provides a unified view of trading data, which is crucial for improving market transparency and price discovery. Under the revised MiFID and MiFIR regulations, ESMA is tasked with setting minimum quality standards for data transmission protocols, the consistency of input and output data formats, and the timing of data dissemination to ensure that the consolidated tape operates effectively across different asset classes.

Challenges Highlighted by AFME:

- Asset Class-Specific Requirements: AFME stresses that a ‘one-size-fits-all’ approach to technical requirements is inappropriate due to the diverse nature of different asset classes. For instance, overly aggressive latency thresholds for bond CTPs could result in disproportionately high costs for users, undermining the utility of the consolidated tape. The MiFID regulation outlines the need for ESMA to establish differentiated standards that reflect the unique trading dynamics of each asset class. AFME advocates for a framework that tailors technical requirements such as latency, data format, and protocol compatibility to the specific needs of bonds, equities, and derivatives, rather than imposing uniform standards that could lead to inefficiencies and increased operational burdens.

- Revenue Distribution Concerns: AFME has consistently opposed revenue distribution mechanisms for data contributors to bond CTPs, arguing that these should remain voluntary and not influence the tender selection process. This stance aligns with MiFID’s broader objectives of fair access and competition in market data provision. The revised MiFID regulation mandates that any revenue distribution scheme must be transparent and equitable, without creating biases in the selection of CTPs. AFME’s position is that financial incentives should not skew the competitive landscape, and the regulatory focus should remain on the quality and accessibility of consolidated market data.

Recommendations:

Tailored Technical Standards: AFME recommends that technical requirements for CTPs be customized for each asset class to avoid unnecessary costs and operational complexities. This approach would better reflect the distinct characteristics of bonds, equities, and derivatives, enhancing the effectiveness of consolidated tape solutions. The MiFID regulation requires that the technical standards consider factors such as data transmission speed, accuracy, and format compatibility, ensuring that CTPs can cater to the specific needs of their respective markets without imposing undue costs on data contributors or end-users.

Reasonable Commercial Basis: Addressing Market Data Pricing under MiFIR

MiFIR regulation mandates that market data providers offer pre- and post-trade data on a reasonable commercial basis, ensuring non-discriminatory access to market data. Despite this, high market data costs have been a persistent issue, prompting legislative revisions to strengthen these requirements. The updated MiFIR regulation introduces stricter obligations for data providers, including enhanced transparency in pricing models, standardized methodologies for calculating fees, and clear guidelines on what constitutes a reasonable commercial basis, aiming to prevent price discrimination and ensure fair access to essential market data.

AFME’s Observations:

- Ineffectiveness of Non-Binding Guidelines: AFME recognizes that previous non-binding guidelines on reasonable commercial basis were insufficient in addressing discriminatory pricing practices. The new approach of converting these guidelines into binding legal obligations is a step forward, as it prevents market data providers from charging clients based on the perceived value of the data to individual users. Under the revised MiFIR regulation, these legal obligations are reinforced by stricter enforcement mechanisms, including penalties for non-compliance and the requirement for market data providers to regularly report their pricing structures to ESMA for review.

- Concerns Over Draft RTS: Although AFME supports the progress made by ESMA, it remains concerned that the current drafting of the RTS could undermine the intended objectives. AFME has proposed amendments to the draft RTS to close gaps that could allow discriminatory pricing to continue, advocating for more precise legal definitions to ensure consistent application across the EU. Key areas of concern include the need for clearer criteria on what constitutes discriminatory pricing practices and the inclusion of detailed enforcement standards that compel market data providers to adhere to the principles set out in MiFIR regulation. AFME's feedback highlights the importance of robust regulatory oversight and the continuous refinement of technical standards to safeguard the integrity of the European financial market.

Strategic Recommendations:

- Strengthening Enforcement Mechanisms: To uphold MiFIR’s reasonable commercial basis requirements, AFME recommends that ESMA incorporate market participants’ feedback into the final drafting of the RTS (Regulatory Technical Standards). The MiFIR regulation mandates ESMA to develop robust enforcement measures that include clear guidelines on monitoring compliance, sanctions for non-compliance, and specific requirements for data providers to ensure fair pricing. AFME emphasises the importance of defining precise criteria and enforcement protocols that prevent discriminatory pricing practices, thereby fostering a competitive market environment where all participants can access market data on equitable terms. The revised MiFIR regulation specifically calls for enhanced transparency in pricing models and obliges data providers to adhere to standardised reporting and fee structures, which are essential to maintaining market integrity.

- Enhanced Data Quality Standards: AFME has also highlighted the need for ESMA to establish stringent data quality measures as part of the MiFIR regulation’s broader framework. These measures include mandatory checks on the completeness, accuracy, and timeliness of market data submitted by trading venues and APAs (Approved Publication Arrangements) to CTPs (Consolidated Tape Providers). AFME argues that such standards will not only improve the overall quality of market data but also support the enforcement of reasonable commercial basis provisions by ensuring that market data is reliable and consistently meets regulatory requirements. Under MiFIR, ESMA is empowered to define these data quality requirements through detailed RTS, enhancing the accountability of market data providers.

- Incorporation of Stakeholder Feedback: The MiFIR regulation’s emphasis on stakeholder engagement is crucial for the effective implementation of its provisions. ESMA is required to consult with market participants, including trading venues, data providers, and end-users, to ensure that the regulatory framework reflects the practical realities of the market. AFME stresses the importance of integrating this feedback into the final RTS to address potential gaps and ambiguities in the regulations, particularly around pricing transparency and non-discriminatory access. This approach aligns with MiFID’s objectives to enhance investor protection and market efficiency by creating a more inclusive and responsive regulatory environment.

- Strengthening Transparency and Accountability: AFME’s recommendations include reinforcing the transparency obligations for CTPs and other data providers under MiFID and MiFIR regulations. ESMA is tasked with developing technical standards that require CTPs to publish clear, consistent, and timely market data, allowing market participants to have a complete view of trading activities across asset classes. These transparency standards are intended to improve price discovery and reduce information asymmetries, which are fundamental to the functioning of fair and efficient markets. AFME advocates for stricter monitoring of compliance with these obligations, including routine audits and public reporting requirements that hold data providers accountable for their market data practices.

- Reinforcing Legal Definitions and Compliance: AFME’s feedback also calls for the reinforcement of legal definitions within the RTS to ensure consistency across the EU. The MiFIR regulation emphasizes the need for clear, legally binding standards that prevent ambiguities and ensure uniform application across all market participants. AFME has proposed specific amendments to the draft RTS, aimed at clarifying the definitions of reasonable commercial basis and discriminatory pricing, thus providing regulators with a stronger legal foundation to enforce these rules effectively. By tightening these definitions, MiFIR aims to create a more predictable and transparent regulatory environment, which is critical for fostering market confidence.

Ensuring Consistent Application Across the EU: A key element of MiFIR regulation is the consistent application of rules across the European Union, aimed at preventing regulatory arbitrage and ensuring a level playing field. AFME stresses that ESMA’s enforcement mechanisms should be designed to apply uniformly across all jurisdictions, ensuring that market data providers comply with MiFIR’s reasonable commercial basis requirements regardless of their location. This consistency is vital for maintaining the integrity of the single market and ensuring that all participants, from small firms to large institutions, have fair access to high-quality market data.

Reduce your

compliance risks