Regulatory Compliance: EBA Reporting Framework

EBA published guidelines on April 9, 2024, for historical data resubmission to maintain regulatory efficiency. These emphasize proportionality, aiming to streamline processes and maintain data consistency. Precision adjustments aim to reduce resubmissions, ensuring high-quality data for authorities.

The European Banking Authority (EBA) published its final Guidelines on April 9, 2024, regarding the resubmission of historical data within the EBA reporting framework, in an effort to expedite regulatory reporting procedures. This action is a component of EBA's continuous efforts to improve the efficacy and efficiency of financial sector regulatory compliance.

The objective of these guidelines is to furnish financial institutions with a uniform methodology for addressing errors, inconsistencies, or modifications in submitted data, in conformity with the supervisory and resolution reporting systems instituted by the European Bank for Advocates. These guidelines are designed to minimize the burden on financial institutions while maintaining the consistency and dependability of submitted data.

They do this by providing clarity on resubmission methods and placing emphasis on the idea of proportionality. Notably, changes like the EBA's filing regulations' improved precision criteria highlight the organization's dedication to lowering needless resubmissions and enhancing data correctness. This breakthrough is a significant step toward creating a regulatory framework that benefits financial firms and regulatory agencies equally by placing a premium on thorough, accurate, and high-quality data.

Data Integrity: Guidelines for Historical Data Resubmission

New recommendations have been developed by the European Banking Authority (EBA) to support the efficacy and efficiency of regulatory reporting regimes. In the case that submitted data contains mistakes, inaccuracies, or revisions, these recommendations provide a uniform procedure for financial institutions to resubmit historical data to competent and resolution authorities. The standards require the correction of both current and historical data, usually covering a calendar year, and are tailored to the frequency of original reporting and the reference dates that are affected.

They also describe situations in which it might not be required to resubmit past data. Crucially, the guidelines define, with flexibility based on supervisory needs, the duties of competent authorities, resolution authorities, and the EBA in managing changes to reported data. Although financial institutions still have a primary responsibility to report accurate, consistent, and complete data, these guidelines are a useful tool for ensuring that reporting requirements are met even in the event of errors or inaccuracies, which in turn makes it easier for regulatory bodies to carry out their statutory duties.

Data Consistency and Fairness

All financial institutions must resubmit their historical data in order to preserve data consistency and make regulatory responsibilities easier for the EBA, resolution agencies, and competent authorities. The EBA highlights the need for a unified and consistent strategy to guarantee fair competition throughout the EU.

The EBA has chosen to lower the precision requirement in monetary data filings rather than creating new materiality thresholds for resubmission, in line with proportionality principles that are already ingrained in reporting standards. For data resubmissions across all institution types, inherent and explicit proportionality is still crucial, even though small and non-complex institutions (SNCIs) provide fewer data points. This strategy emphasizes how crucial it is to keep regulatory compliance activities equitable and effective.

EBA Guidelines Overview

The European Banking Authority (EBA) has made notable progress in enhancing the efficacy and productivity of regulatory reporting systems in the financial industry. The recently created standards, which give financial institutions a uniform method to resubmit past data to competent or resolution authorities, are essential to this endeavor. The objective of these rules is to ensure data quality and consistency by streamlining reporting processes across different types of financial institutions. They are a response to recommendations made in the EBA Report on compliance costs with supervisory reporting requirements. We examine the main features of these principles in this review, emphasizing their significance in promoting data integrity and streamlining regulatory compliance:

- Common Approach to Historical Data Resubmission: In accordance with the EBA's supervisory and resolution reporting system, the recommendations set forth a uniform procedure for financial institutions to resubmit historical data to competent or resolution authorities in the event of mistakes or inaccuracies.

- Reaction to Recommendations of the EBA Report: The EBA's commitment to improving regulatory reporting procedures is reflected in these guidelines, which address a recommendation made in the study on the cost of compliance with supervisory reporting obligations.

- Applicability Across Institution Types: At the individual, sub-consolidated, or consolidated levels, the common methodology is applicable to all forms of supervisory and resolution reporting that are required from financial institutions, such as credit, investment, or payment organizations.

- Exceptional Cases: If specified in the reporting framework, unique requirements for data resubmission may differ from the standard procedure, especially when taking into account reporting area specifics or rectification requirements.

- Focus on Data Corrections: Although the rules mostly deal with historical data corrections, financial institutions are also required to swiftly repair and resubmit any inaccuracies in their most current reference date data that they have submitted.

- Preservation of Reporting Quality: These guidelines serve as a tool to ensure compliance with reporting requirements and to facilitate statutory tasks for the EBA, competent and resolution authorities, and financial institutions. They also reinforce the obligation of financial institutions to provide high-quality, consistent, and complete data.

- Exclusion of Master Data Corrections: Corrections to master data are not included in the common approach described in the recommendations. The need of precise master data in identifying reporting requirements and maintaining dependable IT systems for data submission is emphasized to financial organizations.

- Directive Sections: There are two main sections in the guidelines: General requirements for financial institutions to resubmit historical data are outlined in Section 4, and procedures for competent authorities and resolution authorities to evaluate resubmitted data in conjunction with the EBA are outlined in Section 5.

Comprehensive rules have been published by the European Banking Authority (EBA) to make it easier for past data to be resubmitted within its reporting system. The purpose of these rules is to guarantee data correctness and adherence to supervisory and resolution reporting specifications. Apart from providing a broad framework, the guidelines also tackle particular situations where a resubmission is necessary.

Scenarios when resubmission of historical data is required:

- Frequency-based Approach: The number of previous reference dates varies depending on the reporting frequency. Financial institutions are required to resubmit updated data for the current reference date and historical data impacted by mistakes or inaccuracies for previous reference dates.

- Quarterly Reporting: Financial institutions are required to submit data for four previous reference dates in addition to the current data for quarterly reporting.

- Monthly Reporting: Depending on when the current data was collected in relation to the prior year's conclusion, a monthly reporting scenario will determine how many reference dates need to be resubmitted.

- Cross-Frequency Corrections: Corresponding data for the same time period must also be updated and resubmitted if mistakes or corrections in monthly reporting data also impact data reported with various frequency (such as quarterly).

- Retroactive Resubmissions: When errors impact solely historical data, financial institutions must resubmit updated historical data for all reference dates up to the current data or until the data are determined to be accurate, starting from the reference date where the error occurred.

- Supervisory Discretion: Depending on supervisory needs, competent authorities, resolution authorities, or the EBA may request extra historical data resubmissions above and beyond what is specified in the guidelines.

- Technical Capabilities: Financial institutions need to make sure they have the capacity to submit pertinent data in the format that resolution authorities or competent parties want, both once and again.

Determining Data Resubmission: Exemptions and Tolerance

Under the EBA reporting paradigm, financial institutions might not always be required to resubmit past data. It is essential to comprehend these tolerance limits and exclusions in order to ensure regulatory reporting procedures are efficient and compliant.

Scenarios when resubmission of historical data is not required:

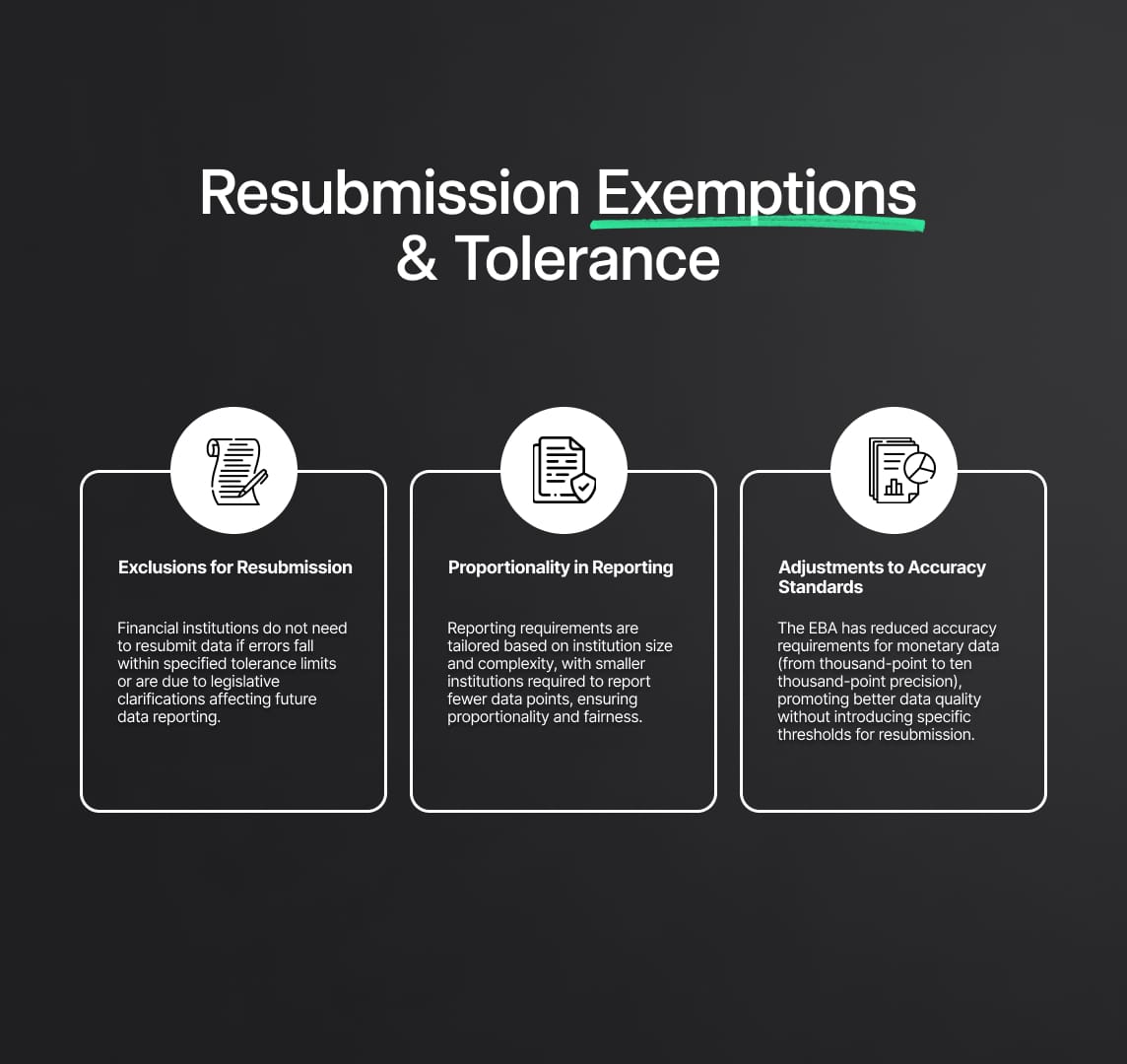

- Legislative Clarifications: Financial institutions only need to apply pertinent changes to future data after the publication of clarifications if the EBA's Questions and Answers on the Single Rulebook indicate that legislative provisions or reporting requirements have been deemed inaccurate and the clarifications provided will affect reported data.

- Tolerance Limits: Errors that do not need to be corrected or resubmitted if they fall under tolerance limits or thresholds specified in agreed-upon filing rules that are available via the EBA Reporting Frameworks webpage.

Balancing Proportionality and Precision

For all financial institutions, resubmitting historical data is essential to ensuring data consistency and enabling regulatory examination by the EBA, resolution authorities, and competent authorities. Maintaining fair playing conditions within the EU requires establishing a unified and consistent strategy. Within this framework, the recommendations prioritize substance and proportionality while avoiding the introduction of explicit resubmission thresholds. Rather, changes to the precision standards are intended to improve the quality of the data while maintaining regulatory compliance. Main Regulatory Requirements Highlighted in the report:

- Principle of Proportionality: The standards emphasize the significance of proportionality in regulatory reporting, taking into account the varying reporting requirements contingent upon the size and complexity of the institution. The legislative structure and reporting standards are ingrained with this innate proportionality, which guarantees that smaller institutions report fewer data points than larger ones.

- Adjustment to the accuracy Requirement: The EBA filing guidelines will lower the thousand-point accuracy requirement for monetary data to ten thousand points instead of creating specified materiality levels for resubmission. The goal of this adjustment is to preserve proportionality while improving data quality and reliability.

- Consistent Approach: The recommendations support a uniform approach for all kinds of financial institutions, making sure that the EBA and competent resolution authorities obtain accurate and trustworthy data that they need to carry out their mandated duties. We do not intend to provide exemptions depending on the size of the institution or the type of reporting, as this could impede regulatory supervision.

- Relevance of Proportionality in Resubmissions: When it comes to data resubmissions, the proportionality that is ingrained in reporting frameworks is still applicable. The extent and character of an organization's operations persist in shaping its supervisory reporting responsibilities, underscoring the continuous significance of proportionality assessments.

Regulatory Compliance: EBA's Guidelines

To sum up, the instructions issued by the European Banking Authority regarding the resubmission of historical data are a crucial step in improving data integrity and regulatory compliance in the financial industry. These recommendations are intended to maintain uniformity among all kinds of financial institutions and to expedite reporting procedures by offering a standardized methodology that takes into account proportionality and materiality. Financial institutions can efficiently fulfill their reporting responsibilities by carefully following these standards, and competent authorities, resolution authorities, and the EBA can rely on accurate and trustworthy data to carry out their mandated duties. In general, these rules represent a noteworthy progression in regulatory reporting structures, cultivating openness, effectiveness, and confidence in the European banking industry.

Reduce your

compliance risks