The Bank Recovery and Resolution Directive (BRRD) ITS

The BRRD is vital to EU financial stability, managing bank failures without taxpayer bailouts. Recent updates to the Implementing Technical Standards (ITS) enhance data reporting, improving accuracy, consistency, and detail.

The Bank Recovery and Resolution Directive (BRRD) is a cornerstone of the European Union’s financial regulatory framework, meticulously designed to manage bank failures in a manner that maintains financial stability and avoids the need for taxpayer-funded bailouts. Born out of the lessons from the 2008 financial crisis, the BRRD provides a robust, structured approach to addressing financial distress in banks, ensuring that the financial system remains resilient even in the face of severe disruptions. As financial markets have become more complex and interconnected, the necessity for more detailed, standardised, and harmonised data collection has intensified, leading to significant updates in the Implementing Technical Standards (ITS) proposed by the European Banking Authority (EBA).

Source

[1]

Alessandro Micagni

Alessandro Micagni

[2]

Alessandro Micagni

Evolution and Importance of the BRRD

The BRRD has been instrumental in laying down the essential requirements for resolution planning across the European Union, setting a precedent for how financial crises are managed at a systemic level. The directive mandates that banks within the EU prepare detailed resolution plans, which are subject to rigorous review by resolution authorities. These plans are not merely procedural checklists but are comprehensive strategies designed to ensure that a failing bank can be wound down or restructured without causing widespread economic harm or requiring public financial support.

However, the financial landscape has not remained static since the BRRD was first introduced. The increasing complexity of financial institutions, coupled with the evolving nature of global financial markets, has necessitated a reevaluation and enhancement of the technical standards that underpin the BRRD. On 30 July 2024, the EBA issued a consultation paper proposing significant revisions to the ITS, which are central to the implementation of the BRRD. These proposed changes are critical as they aim to enhance the quality, usability, and consistency of the data that banks are required to report.

Data Quality, Usability, and Consistency

The proposed updates to the ITS are fundamentally about improving the granularity and relevance of the data that banks must submit. The EBA’s focus is on ensuring that resolution authorities have access to data that is not only accurate and timely but also detailed enough to allow for precise and effective decision-making in times of crisis.

One of the key enhancements is the move towards more granular data reporting. This shift recognizes that broad, aggregate data can mask critical details that are vital for assessing a bank’s true financial health and its interconnectedness with the broader financial system. By requiring banks to report data at a more detailed level, the EBA aims to provide resolution authorities with a clearer picture of the risks within the financial system. This includes detailed reporting on liability structures, such as the distinction between secured and unsecured liabilities, the identification of intragroup exposures, and the exact terms of financial instruments that could affect a bank’s solvency.

BRRD: Addressing the Complexity of Crisis Management

The growing complexity of financial institutions—characterized by diverse financial products, intricate organizational structures, and extensive cross-border operations—has made crisis management increasingly challenging. The updated ITS aim to address these challenges by ensuring that the data collected is comprehensive and reflects the multi-faceted nature of modern banking.

For instance, the revised ITS place a stronger emphasis on understanding the interconnections between different parts of a banking group. This includes detailed reporting on intragroup transactions and exposures, which are critical for assessing the potential for contagion within a banking group. Such data allows resolution authorities to determine whether the failure of one part of a banking group could trigger a broader systemic crisis.

Additionally, the ITS revisions address the need for better data on the financial markets infrastructures (FMIs) that banks rely on, such as clearinghouses and payment systems. Understanding a bank’s dependencies on these FMIs is crucial for resolution planning, as disruptions in these infrastructures could have far-reaching consequences for financial stability.

Key Enhancements in the Proposed ITS for the Bank Recovery and Resolution Directive (BRRD)

1. Defining the Relevant Legal Entity: A New Precision in Reporting Obligations

The Bank Recovery and Resolution Directive (BRRD) places a strong emphasis on the identification and classification of "relevant legal entities" within banking groups. The latest Implementing Technical Standards (ITS) proposed by the European Banking Authority (EBA) provide a more precise and comprehensive definition of what constitutes a relevant legal entity, which is pivotal for determining the specific reporting obligations of entities within a banking group.

This redefinition is crucial because it directly influences which entities must report detailed financial and operational data, a key requirement for effective resolution planning. The criteria outlined in the proposed ITS are designed to capture entities that are not only significant in terms of size and risk but also critical to the functioning of the broader financial system. The inclusion of entities based on the following criteria ensures that those with the most potential to impact financial stability are closely monitored:

- Provision of Critical Functions: This criterion targets entities that provide services indispensable to the operation of the financial system. These functions could include payment processing, clearing and settlement operations, and other essential services that, if disrupted, could have significant adverse effects on the financial system. Identifying these entities allows resolution authorities to prioritize their resolution plans, ensuring that critical functions are maintained even in the event of a bank failure.

- Risk Exposure: Entities with total risk exposure exceeding 2% of the group’s consolidated risk exposure are flagged as relevant legal entities. Risk exposure here encompasses the potential losses a bank might face due to its various financial activities, including lending, investment, and trading operations. By focusing on entities with substantial risk exposure, the ITS ensure that those with the highest potential to affect the financial health of the group are included in resolution planning.

- Total Exposure Measure: Similar to risk exposure, this measure looks at the total exposure of an entity in relation to the group’s consolidated total exposure. Entities meeting or exceeding 2% of this measure are considered significant. Total exposure includes all on-balance-sheet and off-balance-sheet items, providing a comprehensive view of an entity's potential impact on the financial stability of the group.

- Operating Income: Entities that contribute significantly to the group’s financial performance—specifically those with operating income equal to or exceeding 2% of the group’s total—are also included. Operating income is a crucial indicator of an entity’s ongoing financial viability and its importance within the group. High operating income signals that the entity plays a major role in generating revenue for the group, making its stability and resolution a priority.

- Total Assets: Entities with assets exceeding €5 billion are automatically considered relevant legal entities. The asset size is a direct indicator of the entity’s scale and the potential systemic risk it poses. Larger entities typically have more complex operations and a broader reach, which can complicate resolution processes if not properly managed.

- Financial Stability Impact: This criterion identifies entities deemed critical to the financial stability of at least one Member State. This assessment is vital for cross-border banking groups, where the stability of the financial system in one country can have significant ripple effects throughout the EU. Including these entities ensures that resolution plans are tailored to maintain stability not just within the banking group, but across the entire EU financial system.

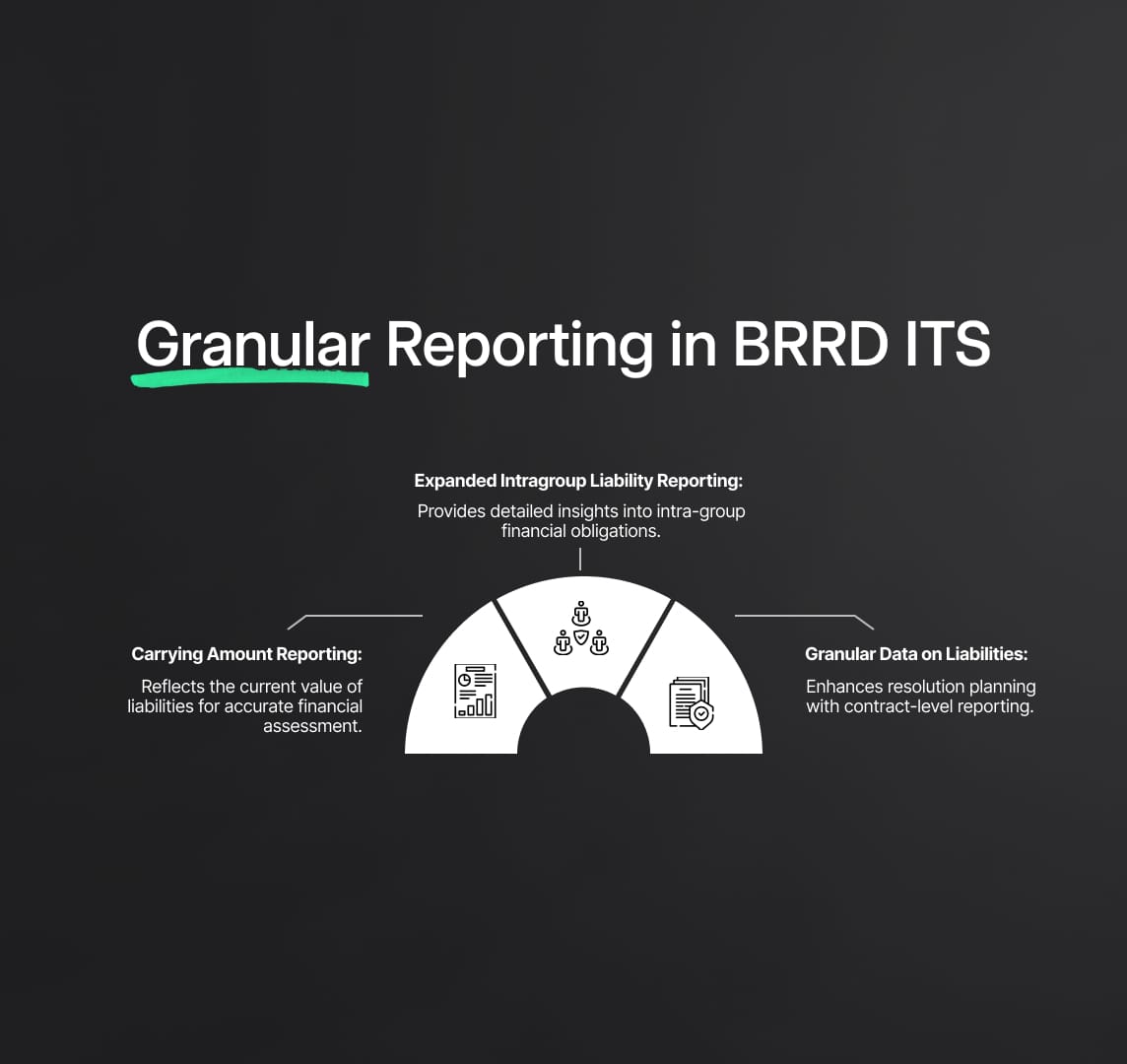

2. Granular Liability Data: Expanding Transparency and Reporting Scope

The EBA’s proposed updates to the ITS introduce significant changes to how banks report their liability structures, marking a pivotal step towards greater transparency and enhanced regulatory oversight under the BRRD. Traditionally, banks were required to report the "Outstanding Amount" of their liabilities—a broad measure that, while useful, often lacked the granularity needed for detailed risk assessment and resolution planning. The EBA’s new proposal to include the "Carrying Amount" in these reports significantly enriches the data available to resolution authorities.

The Carrying Amount provides a more accurate reflection of the current value of liabilities on a bank’s balance sheet, taking into account adjustments for factors like amortization, impairments, and fair value changes. This measure is critical for understanding the real-time financial position of a bank, particularly in volatile markets where the nominal value of liabilities may differ significantly from their carrying value. By requiring banks to report both the outstanding and carrying amounts, the ITS ensure that resolution authorities have a clearer, more accurate picture of a bank’s obligations, which is essential for evaluating the bank's solvency and overall financial health.

In addition to this, the scope of intragroup liability reporting has been expanded. Intragroup liabilities—financial obligations between entities within the same banking group—are now required to be reported in greater detail, including those liabilities excluded from the bail-in process. This is a crucial development because it addresses the potential for intra-group contagion, where the financial difficulties of one entity could quickly spread to others within the same group. By expanding this reporting requirement, the ITS enable resolution authorities to better understand the financial interconnections within a banking group, which is essential for making informed decisions about the appropriate resolution strategy, whether it be a Single Point of Entry (SPE) or Multiple Point of Entry (MPE) approach.

The inclusion of granular, contract-level data on various liability types further enhances the resolution planning process. Banks are now required to provide detailed reports on:

- Intragroup Liabilities: This includes not just the amounts owed but also the specific terms of these liabilities, such as maturity dates, interest rates, and conditions for repayment. This level of detail is vital for assessing the risks associated with intragroup financing arrangements and for determining how these obligations should be handled in a resolution scenario.

- Securities: Detailed reporting at the ISIN (International Securities Identification Number) code level allows resolution authorities to track specific financial instruments and their associated risks. This includes understanding the nature of the securities, their market value, and the exposure they represent to the bank and its stakeholders.

- Deposits: Reporting at the contract level for deposits provides insights into the bank’s liability structure, including the distribution of deposit types (e.g., retail vs. corporate), maturity profiles, and the potential impact of a depositor run in times of financial distress. This information is crucial for assessing the bank’s liquidity position and its ability to meet short-term obligations.

- Secured Financing: Detailed data on secured financing transactions, including the collateral used and the terms of these agreements, are essential for understanding the bank’s reliance on secured funding sources. This is particularly important in a resolution scenario, where the availability and value of collateral can significantly influence the outcome.

- Other Financial and Non-Financial Liabilities: By expanding the reporting scope to include various other liabilities, the ITS provide a comprehensive view of the bank’s obligations. This is critical for assessing the full range of risks that the bank faces and for planning how these liabilities will be managed in the event of a resolution.

The granular data now required under the ITS is indispensable for assessing the bail-in-ability of liabilities—essentially, determining which liabilities can be written down or converted into equity to absorb losses in a resolution. This is a key element of the BRRD’s strategy to protect taxpayers and maintain financial stability by ensuring that shareholders and creditors bear the costs of bank failures, not the public.

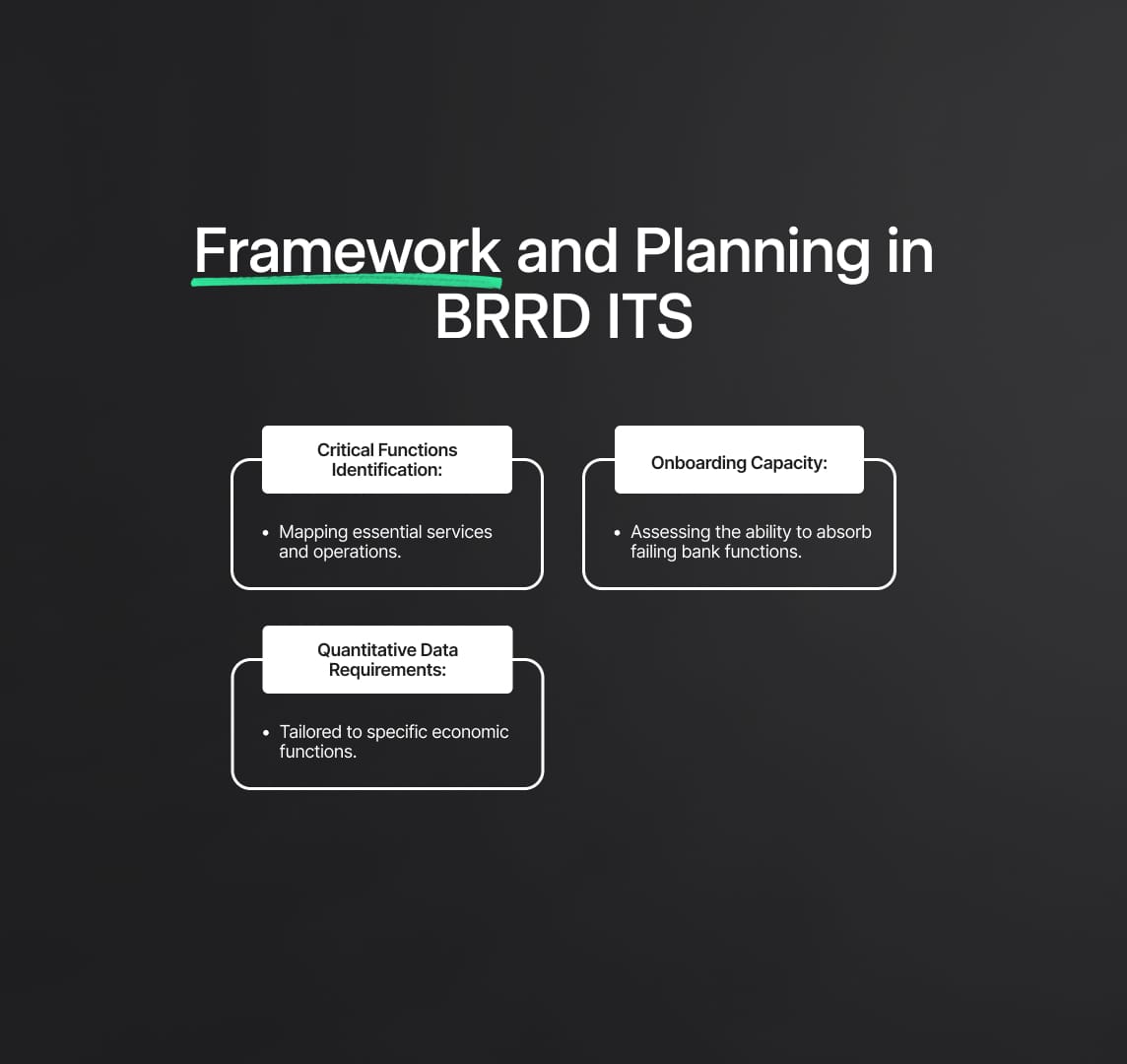

Critical Functions and Core Business Lines: Ensuring Continuity in Financial Stability

Under the Bank Recovery and Resolution Directive (BRRD), the identification and preservation of critical functions and core business lines are paramount to maintaining financial stability during the resolution of a bank. These components are crucial because they represent the essential services and operations that, if disrupted, could lead to significant systemic risks across the financial system. The BRRD mandates that banks meticulously identify, map, and assess these functions and lines, ensuring that they can continue operating even in the event of severe financial distress.

BRRD: Identification and Mapping of Critical Functions

The BRRD requires institutions to carry out a detailed mapping of their critical functions. These functions typically include vital services such as payment systems, lending, deposit-taking, and operations within the capital markets. The identification process is rigorous and involves evaluating the role these functions play in the broader financial system, their importance at various levels—regional, national, and EU-wide—and their potential impact on financial stability if interrupted.

Onboarding Capacity: Absorbing Functions of a Failing Bank

The revised BRRD introduces the concept of Onboarding Capacity—a critical assessment of an entity’s ability to absorb and continue the critical functions of a failing bank. This concept is essential in ensuring that when a bank fails, its vital operations can be seamlessly transferred to another entity without causing systemic disruption. Onboarding Capacity metrics evaluate how quickly and effectively these critical functions can be adopted by another institution, focusing on the operational readiness, technological infrastructure, and legal frameworks required to maintain continuity.

The analysis of Onboarding Capacity involves specific quantitative assessments, such as the number of customer applications that can be processed over various timeframes (e.g., 1, 7, and 14 working days), which serves as a proxy for the institution's ability to scale operations quickly in the event of a bank failure. This evaluation ensures that the resolution plans are not just theoretical but actionable and effective in real-world scenarios.

Quantitative Data Requirements for Economic Functions

The BRRD’s updated Implementing Technical Standards (ITS) also introduce detailed quantitative data requests tailored to specific underlying economic functions, enhancing the depth of the criticality assessment. These data requirements include:

- Deposits: Institutions must report on the value of deposit accounts, including the proportion of uninsured deposits and those associated with recurrent accounts. Additionally, cross-border activity indicators, such as the number of accounts and transaction volumes, are required. This data helps authorities assess the liquidity risks and potential impact of a depositor run.

- Lending Activities: Banks are required to provide data on risk-weighted assets per economic function, outstanding amounts, and cross-border lending activities. This information is crucial for understanding the bank's exposure to credit risks and its ability to continue lending operations during a resolution.

- Payments Function: Detailed reporting on the value of transactions processed through recurrent accounts, along with cross-border payment activity, provides insights into the bank’s role in the payment system. This is vital for assessing the systemic importance of the bank in ensuring the smooth flow of transactions within the economy.

- Capital Markets: The ITS require detailed reporting on the number of counterparties, transaction volumes, and cross-border values related to capital market activities. This data helps in evaluating the potential systemic risks posed by the bank’s trading and investment operations.

- Wholesale Funding: Institutions must report on (reverse) repurchase agreements, cross-border funding activities, and values at credit institutions. This information is essential for assessing the bank's reliance on wholesale funding markets and its liquidity risk profile.

BRRD Focus: Reporting on Relevant Services and Financial Market Infrastructures (FMIs)

The BRRD’s focus on relevant services and Financial Market Infrastructures (FMIs) reflects the growing complexity and interconnectedness of the financial system. FMIs are crucial for the execution, clearing, and settlement of transactions, and their stability is integral to the broader financial ecosystem. The updated ITS significantly expand the reporting requirements for these entities, ensuring that resolution authorities have a clear understanding of their roles, operations, and potential points of failure.

Detailed Reporting on Relevant Services

Institutions are now required to identify and map relevant services that support critical functions and core business lines. This mapping includes linking these services to specific operational assets and roles within the organization. The objective is to ensure that all elements essential to maintaining these critical functions are identified and safeguarded during a resolution.

For example, the ITS require banks to report on services related to IT infrastructure, human resources, and logistical support that are necessary for the continued operation of critical functions. This detailed reporting helps resolution authorities understand the dependencies within a bank's operations and plan accordingly to prevent disruptions.

Substitutability and Metrics for Financial Market Infrastructures

The updated ITS introduce more granular reporting on Financial Market Infrastructures (FMIs), particularly focusing on the substitutability of central counterparty (CCP) segments and other critical services. FMIs play a pivotal role in the financial system by ensuring the smooth execution of trades and the stability of settlement processes.

Banks are required to provide detailed data on the contracts managed by FMIs, including notional amounts for derivatives and other financial instruments. This information is critical for assessing the risks associated with these contracts and the potential impact of their disruption. Additionally, the ITS require institutions to evaluate the availability of alternative FMIs that could take over these functions in the event of a failure, ensuring that resolution plans include contingency measures to maintain market stability.

Proportionality and the Modular Reporting Approach

The BRRD’s principle of proportionality is central to its regulatory framework, ensuring that the reporting requirements are tailored to the size, complexity, and risk profile of each institution. The updated ITS introduce a modular reporting approach that categorizes institutions based on their significance and risk, assigning different levels of reporting obligations accordingly.

Core Reporting Requirements

All entities, regardless of size, are subject to Core Reporting Requirements. These requirements focus on essential data needed for resolution planning, such as basic organizational structures, key financial metrics, and a high-level overview of critical functions. This ensures that all institutions contribute to the overall resolution planning process, providing a baseline of information that resolution authorities can use to develop and refine their strategies.

Supplemental Reporting Requirements

For larger or more complex institutions, the ITS impose Supplemental Reporting Requirements. These institutions are required to provide more detailed and granular data, enabling resolution authorities to develop intricate resolution strategies that address the specific risks and challenges posed by these entities. This approach ensures that the reporting burden is proportional to the institution's potential impact on financial stability, avoiding unnecessary compliance costs for smaller, less complex entities while ensuring that larger institutions are thoroughly assessed and prepared for resolution scenarios.

Simplification and Deletion of Redundant Templates

In an effort to streamline the reporting process and reduce the burden on institutions, the EBA has identified certain templates that are no longer necessary for effective resolution planning. For example, templates that primarily provide information on IT systems, such as Z 10.01 and Z 10.02, have been deemed redundant and are proposed for deletion. These templates were found to offer limited value in assessing the resolvability of institutions, and their removal is expected to simplify the reporting process without compromising the quality of the data collected.

Impact Assessment and Cost-Benefit Analysis Under the Bank Recovery and Resolution Directive (BRRD)

The European Banking Authority (EBA) undertook a meticulous impact assessment and cost-benefit analysis as a crucial component of the regulatory process for the new Implementing Technical Standards (ITS) under the Bank Recovery and Resolution Directive (BRRD). This analysis is pivotal in understanding the broad implications of the updated ITS on both financial institutions and the wider financial system. By examining the challenges posed by the current framework and the strategic enhancements proposed in the new standards, the EBA aims to ensure that the BRRD remains effective in maintaining financial stability while minimizing the regulatory burden on institutions.

A. Problem Identification and Background

The existing ITS framework, initially designed to meet the needs of the financial system post-2008, has become increasingly inadequate in addressing the complexities of modern banking crises. The dynamic nature of financial markets, coupled with the lessons learned from recent crises, highlighted several shortcomings in the current reporting and resolution planning processes. These gaps primarily relate to the lack of granularity in data collection, inconsistencies in reporting practices across jurisdictions, and the challenges posed by ad hoc data requests during periods of financial distress.

The EBA identified that the existing ITS framework was struggling to keep pace with the evolving landscape of financial risks. Specifically, the framework's limited scope in capturing detailed liability structures and critical functions posed significant risks to effective resolution planning. Without the necessary depth and breadth in data, resolution authorities faced difficulties in developing and executing plans that could withstand the complexities of a modern financial crisis.

B. Policy Objectives

The updated ITS have been crafted with specific policy objectives in mind, all geared towards enhancing the overall effectiveness of the BRRD framework. The primary objective is to align resolution planning templates and reporting instructions with the latest developments in resolution strategies, ensuring that the data collected is not only comprehensive but also relevant to the current financial environment.

One of the key policy goals is to foster greater harmonisation across different Resolution Authorities (RAs) within the EU. Discrepancies in reporting practices and data standards have historically led to inefficiencies and challenges in cross-border resolution efforts. By standardising these practices, the ITS aim to streamline the resolution process, making it more cohesive and coordinated across member states. This is particularly crucial given the interconnected nature of financial markets, where the failure of a single institution can have ripple effects across multiple jurisdictions.

C. Options Considered and Preferred Choices

In the development of the updated ITS, the EBA considered several policy options, each with its own set of implications for financial institutions and resolution authorities. The evaluation of these options was guided by the need to balance the thoroughness of data collection with the practicalities of implementation and compliance costs.

- Relevant Legal Entity (RLE) Thresholds: The existing criteria for identifying Relevant Legal Entities (RLEs) were deemed insufficient for capturing the full scope of entities that could pose significant risks in a resolution scenario. The preferred option involved expanding these criteria by incorporating thresholds used by the Single Resolution Board (SRB), such as total risk exposure, total assets, and the impact on financial stability.The introduction of a financial stability criterion ensures that entities crucial to the stability of the financial system are identified and included in resolution planning. This approach mitigates the risk of overlooking entities that, while not large in terms of assets, play a critical role in the financial ecosystem. By lowering the RLE threshold from 5% to 2% of the group's total exposure, the ITS cast a wider net, ensuring that more entities are brought under the scrutiny of resolution authorities. This expansion is essential for comprehensive resolution planning and for avoiding gaps in the data that could undermine the effectiveness of resolution strategies.

- Granular Liability Data: The requirement for granular liability data reporting was another significant consideration in the ITS development. The preferred option mandates the collection of detailed, contract-level data on various types of liabilities, including intragroup liabilities, securities, and deposits not excluded from bail-in.This granularity is critical for several reasons. Firstly, it enhances transparency, providing resolution authorities with a clear view of the financial obligations of institutions. Understanding the specific liabilities, including their contractual terms and conditions, allows authorities to accurately assess the institution's financial health and its ability to absorb losses through bail-in mechanisms. Secondly, granular data facilitates better risk assessment and decision-making, particularly in determining the appropriate resolution strategy, whether it be a Single Point of Entry (SPE) or Multiple Point of Entry (MPE) approach.The standardization of liability data across institutions also reduces the variability in reporting, ensuring that all entities are assessed on a level playing field. This uniformity is essential for the comparability of data, which is a cornerstone of effective resolution planning in a multi-jurisdictional context.

Implementation Timeline and Next Steps: A Detailed Exploration Under the Bank Recovery and Resolution Directive (BRRD)

The implementation timeline for the new Implementing Technical Standards (ITS) under the Bank Recovery and Resolution Directive (BRRD) is a critical phase that will shape the future of bank resolution planning and reporting across the European Union. The European Banking Authority (EBA) has outlined a clear and structured approach to ensure that these standards are seamlessly integrated into the operational frameworks of financial institutions, providing sufficient time for adaptation while maintaining a rigorous focus on enhancing financial stability.

Finalisation and Endorsement Process

Following the consultation period, during which key stakeholders—including banks, resolution authorities, and other financial entities—are expected to provide feedback on the draft ITS, the EBA will undertake a thorough review of all submissions. This review process is crucial for refining the standards, ensuring that they are both comprehensive and practical in their application. The feedback will be meticulously analyzed to address any concerns or suggestions, with the aim of optimizing the ITS for effectiveness and feasibility.

Once the feedback has been incorporated, the EBA will finalize the draft ITS and submit them to the European Commission for endorsement. This step is pivotal as it transitions the ITS from a consultative framework to a binding regulatory requirement across the EU. The European Commission's endorsement will formalize the standards, ensuring that they align with broader EU regulatory objectives and legal frameworks.

Upon endorsement, the ITS will be published in the Official Journal of the European Union, making them legally binding across all Member States. This publication marks the official start of the countdown to the compliance deadlines, signaling to financial institutions the urgency and importance of adapting their systems to meet these new requirements.

Operationalisation Timeline: Preparing for Compliance

The new reporting framework outlined in the ITS is scheduled to become operational in 2026, with the first reporting reference date set for 31 December 2025. This timeline is strategically designed to provide banks with sufficient lead time to implement the necessary changes to their reporting systems and processes.

This transition period is not merely a buffer but an essential phase for institutions to undertake significant updates to their data management infrastructure. Banks will need to focus on enhancing their internal systems to capture the granular data required under the new ITS, including detailed liability data, information on critical functions, and comprehensive ownership structures. These updates are not trivial; they involve overhauling existing data collection processes, integrating new reporting templates, and ensuring that data accuracy and consistency meet the high standards set by the ITS.

Reduce your

compliance risks