TLAC/MREL Eligibility Criteria and AT1 Instruments

The European Banking Authority (EBA) ensures the integrity of own funds and eligible liabilities in the EU, per CRR Article 80(1). On June 27, 2024, the EBA updated its report on AT1, Tier 2, TLAC, and MREL instruments.

The European Banking Authority (EBA) is mandated to ensure the quality and integrity of own funds and eligible liabilities instruments issued by financial institutions across the European Union. This mandate is articulated in Article 80(1) of Regulation (EU) No 575/2013, commonly referred to as the Capital Requirements Regulation (CRR). The EBA's responsibilities include evaluating these instruments against strict regulatory standards and notifying the European Commission if any instruments fail to meet the prescribed eligibility criteria. This regulatory oversight is crucial in maintaining the resilience and stability of the EU’s financial system, particularly in times of economic stress.

On 27 June 2024, the EBA published an updated report, continuing its essential monitoring work. This comprehensive report provides the latest findings and guidance on Additional Tier 1 (AT1), Tier 2, Total Loss-Absorbing Capacity (TLAC), and Minimum Requirement for Own Funds and Eligible Liabilities (MREL) instruments. The report builds on the EBA's extensive evaluation of these instruments, ensuring they meet the necessary standards for loss absorbency and financial robustness.

Source

[1]

Alessandro Micagni

Alessandro Micagni

[2]

Alessandro Micagni

TLAC/MREL iRegulation: Purpose of the Report

The primary goal of this report is to keep external stakeholders well-informed about the EBA's continuous monitoring activities related to AT1, Tier 2, and TLAC/MREL instruments. This updated report from June 2024 enhances the previous report issued in July 2023. By integrating insights from earlier AT1 and TLAC/MREL monitoring reports, the EBA aims to highlight the commonalities in eligibility criteria and loss absorbency features across these instruments. This consolidation facilitates a clearer understanding and ensures consistent application of regulatory standards.

TLAC/MREL Eligibility Criteria and AT1 Instruments: Technical Analysis

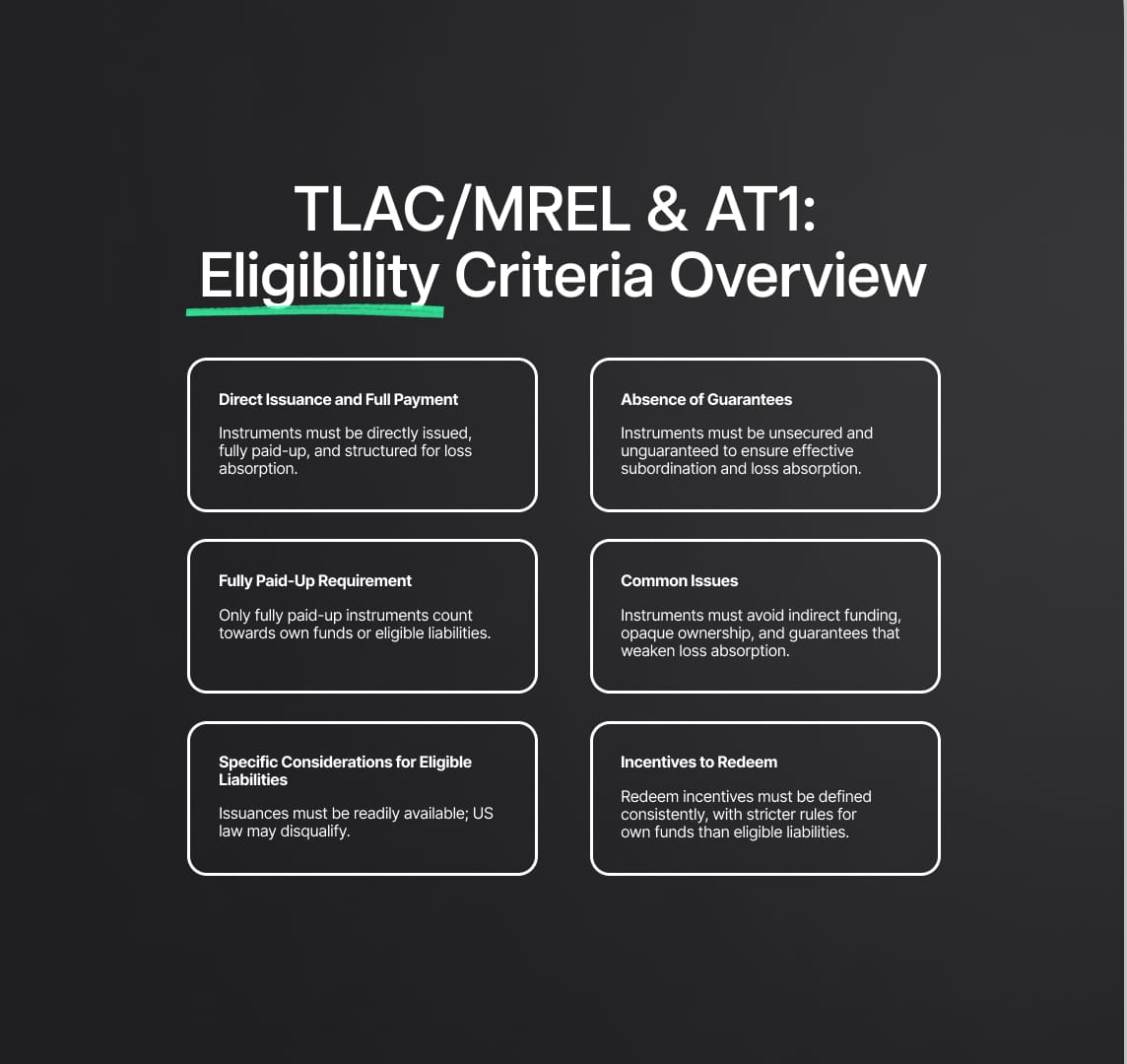

Direct Issuance and Full Payment: Instruments must be issued directly by the financial institution or its resolution entity and must be fully paid up. This ensures that the instruments are genuinely available to absorb losses when needed. Detailed provisions stipulate that these instruments cannot be owned by the issuing institution or its subsidiaries, which extends to entities within the same resolution group under Article 88a of the CRR and Article 45b(3) of the BRRD.

Absence of Guarantees: According to Articles 52(1)(e), 63(e), and 72b(2)(e) of the CRR, eligible instruments must not be secured or enhanced by any form of guarantee that increases the seniority of the claims. This provision ensures that the instruments maintain their subordinated status, crucial for effective loss absorption.

Fully Paid-Up Requirement: Only the portion of the instruments that is fully paid up can be counted towards own funds or eligible liabilities. This requirement is reinforced by specific subparagraphs in Articles 52(1), 63, and 72b(2)(a) of the CRR, ensuring that financial institutions do not rely on partially paid instruments for their loss-absorbing capacity.

Common Issues in Terms and Conditions: The report addresses frequent issues in the terms and conditions of these instruments, such as indirect funding and ownership, guarantees in restructuring scenarios, and payment undertakings. Instruments must not be indirectly funded by the institution, and clear ownership restrictions should be outlined to avoid conflicts of interest. Additionally, any guarantees required during restructuring must be carefully assessed to ensure they do not undermine the loss-absorbing capacity of the instruments.

Specific Considerations for Eligible Liabilities Instruments: The report highlights specific regulatory considerations for eligible liabilities instruments, including the necessity for issuance by the resolution entity, stringent availability criteria, and the treatment of US law securities. The EBA maintains a firm stance on debt securities issued under certain US legal frameworks, which may not qualify as MREL due to potential legal conflicts.

Incentives to Redeem: The EBA emphasises that incentives to redeem must be consistently defined across own funds and eligible liabilities. For own funds, such incentives are strictly prohibited, whereas for eligible liabilities, they can result in a shortened maturity when combined with call options. This ensures that the instruments remain a stable funding source.

Tax Gross-Up Clauses and Interest Rate Reset Mechanisms: The inclusion of tax gross-up clauses and the structuring of interest rate reset mechanisms are also critically evaluated. Gross-up clauses should only relate to withholding tax on dividends or coupons and must not exceed distributable items. Interest rate reset mechanisms should avoid creating incentives to redeem, thus maintaining the stability and predictability of the instruments.

Regulatory Compliance and Supervisory Flexibility: Financial institutions must demonstrate to supervisors that their issuances do not contain incentives to redeem due to reset mechanisms. Additionally, the EBA may provide supervisory flexibility for small issuers in volatile market conditions, provided they demonstrate stable credit spreads.

AT1, Tier 2, and TLAC/MREL Eligible Liabilities Instruments

The European Banking Authority (EBA) places significant emphasis on monitoring Additional Tier 1 (AT1) and eligible liabilities instruments to ensure they adhere to the stringent regulatory standards outlined in the Capital Requirements Regulation (CRR). This oversight is critical for maintaining financial stability and ensuring that these instruments can effectively absorb losses. While the issuance of these instruments is largely standardized due to prescriptive provisions within the regulatory framework, certain institution-specific features, such as trigger levels, necessitate meticulous evaluation. This evaluation is crucial for validating the instruments' compliance and their capacity to support financial resilience in adverse conditions.

Status of the Notes – Absence of Guarantees and Notion of ‘Fully Paid-Up’

The eligibility criteria for AT1, Tier 2, and TLAC/MREL instruments are comprehensively detailed in Articles 52(1), 63, and 72b of the CRR. These criteria are designed to ensure that the instruments provide genuine loss-absorbing capacity, which is vital for the stability of financial institutions. Key requirements include:

Direct Issuance and Full Payment:

- Direct Issuance: Instruments must be issued directly by the financial institution or its designated resolution entity. This direct issuance requirement ensures that the instruments are unequivocally tied to the institution's ability to absorb losses.

- Full Payment: Instruments must be fully paid up. This means that the institution cannot count partially paid instruments towards its regulatory capital. The fully paid-up criterion guarantees that the entire amount of the instrument is available to absorb losses immediately when needed.

- Ownership Restrictions: The instruments must not be owned by the institution itself or its subsidiaries. For AT1 and Tier 2 instruments, this ownership restriction extends to all entities within the same resolution group. Similarly, for eligible liabilities instruments, this restriction applies to entities within the same resolution group as defined under Article 88a of the CRR and Article 45b(3) of the Bank Recovery and Resolution Directive (BRRD). These provisions prevent conflicts of interest and ensure that the instruments provide a genuine layer of financial protection.

Absence of Guarantees:

- No Enhancements: According to Articles 52(1)(e), 63(e), and 72b(2)(e) of the CRR, eligible instruments must not be secured or subject to any guarantees that could enhance the seniority of claims. This requirement is crucial to maintain the subordinated nature of the instruments, ensuring they can effectively absorb losses. The provisions should explicitly state that no security or guarantee of any kind is provided. This clarity helps prevent any potential elevation of the instrument's claim seniority, which could undermine its loss-absorbing capacity.

Fully Paid-Up Requirement:

- Capital Eligibility: Only the portion of the instruments that is fully paid up can be counted towards own funds or eligible liabilities. This requirement is reinforced by specific subparagraphs in Articles 52(1), 63, and 72b(2)(a) of the CRR. The fully paid-up status ensures that there is no contingent liability that could reduce the instrument's effectiveness in absorbing losses.

- Regulatory Compliance: Financial institutions must ensure that the instruments are fully funded with no pending payment obligations. This full funding is essential for the instruments to be recognised as regulatory capital, providing a robust buffer against financial distress.

TLAC/MREL instruments: Common Issues in Terms and Conditions

Several common issues frequently arise in the terms and conditions of these instruments, which can impact their eligibility and effectiveness:

Indirect Funding and Ownership:

- Conflict Prevention: Instruments should not be indirectly funded by the issuing institution. Clear ownership restrictions must be outlined to prevent any conflicts of interest and to ensure the genuine nature of the loss-absorbing capacity.

Guarantees in Case of Restructuring:

- Subordination and Specificity: Provisions that require an institution to provide a guarantee if a subsidiary takes over obligations must be carefully assessed. Such guarantees should be subordinated, specific to restructuring events, and must not cover canceled coupons for AT1 instruments. This ensures that the instruments remain subordinated and maintain their loss-absorbing capacity even during restructuring.

Payment Undertakings:

- Advanced Payments: Commitments to pay cash to the institution on demand or at a future date do not meet the fully paid-up requirement. Instruments must be fully paid in advance to qualify as eligible liabilities. This prepayment ensures that the full amount is immediately available for loss absorption without any delay.

Specific Considerations for Eligible Liabilities Instruments

Resolution Entity Issuance:

- Issuance Requirements: Eligible liabilities instruments must be issued by the entity subject to the requirement (i.e., the resolution entity). In some cases, derogations allow for issuance by subsidiaries under specific conditions. This requirement ensures that the instruments are directly tied to the entity responsible for absorbing losses.

Availability Criteria:

- Verification Needs: Provisions should state that notes constitute direct, unconditional, and unsecured obligations of the issuer. However, these criteria often require additional verification beyond the contractual language to ensure compliance with regulatory standards.

US Law Securities:

- Regulatory Stance: The EBA maintains that debt securities issued under Section 3(a)(2) of the US Securities Act of 1933 and guaranteed by a branch of an EU institution do not qualify as MREL. This position considers the complexity and potential conflicts with third-country laws, ensuring that only instruments that meet stringent EU standards are eligible.

Incentives to Redeem

Consistent Definitions:

- Stability Provisions: Incentives to redeem must be defined consistently across own funds and eligible liabilities despite triggering different consequences. Both categories are intended to provide stable funding. Incentives to redeem are strictly prohibited for own funds to maintain permanence, while for eligible liabilities, they can result in a shortened maturity when combined with a call option. This consistency ensures that the instruments remain a stable source of financial support.

Regulatory Compliance:

- Demonstration to Supervisors: Banks should be able to demonstrate to supervisors that issuances do not contain incentives to redeem as a result of reset mechanisms. This compliance is critical to maintaining the integrity and stability of the instruments as effective loss-absorbing tools.

MREL (Minimum Requirement for Own Funds and Eligible Liabilities) / TLAC (Total Loss Absorbing Capacity) Issues in Terms and Conditions

Avoidance of Conflicts of Interest: Instruments must not be indirectly funded by the issuing institution. This requirement ensures that the instruments' loss-absorbing capacity is genuine and unencumbered by internal financing mechanisms. Ownership restrictions must be clearly outlined in the terms and conditions to prevent any conflicts of interest. These restrictions help maintain the integrity and effectiveness of the instruments in providing financial stability.

Detailed Ownership Restrictions: The instruments should not be owned by the institution itself, its subsidiaries, or any entities within the same resolution group. This extends to both direct and indirect ownership. Clear documentation and contractual provisions must delineate these ownership restrictions to ensure compliance with regulatory standards.

Guarantees in Case of Restructuring

Subordination and Specificity: Provisions requiring an institution to provide a guarantee if a subsidiary takes over obligations must be carefully assessed to ensure they do not undermine the instrument's loss-absorbing capacity. Guarantees should be:

- Subordinated: They must be explicitly subordinated to ensure they do not elevate the seniority of the claims.

- Specific to Restructuring Events: Guarantees should be applicable only in specific restructuring events, not as a general security.

- Exclusion of Canceled Coupons: For AT1 instruments, guarantees must not cover canceled coupons to maintain their eligibility and compliance with regulatory requirements.

Payment Undertakings

Advance Payments Requirement: Commitments to pay cash to the institution on demand or at a future date do not satisfy the paid-up requirement. Instruments must be fully paid in advance to qualify as TLAC/MREL eligible liabilities. This requirement ensures that the full amount of the instrument is immediately available to absorb losses without any delay.

Implications for Compliance: Financial institutions must ensure that all payment undertakings are met prior to issuance. This involves rigorous internal controls and verification processes to confirm that instruments are fully funded and compliant with the regulatory framework.

TLAC/MREL requirement: Considerations for Eligible Liabilities Instruments

Entity-Specific Issuance Requirements: Eligible liabilities instruments must be issued by the entity subject to the TLAC/MREL requirement, typically the resolution entity. Derogations are permissible under specific conditions, allowing subsidiaries to issue these instruments if they meet stringent criteria set forth by the resolution authorities. This requirement ensures that the instruments are closely tied to the entity responsible for loss absorption.

Documentation and Verification: Issuing entities must maintain comprehensive documentation and verification processes to ensure that all issuances comply with the resolution entity requirement. This includes obtaining necessary approvals and maintaining records to demonstrate compliance during regulatory reviews.

Availability Criteria

Direct, Unconditional, and Unsecured Obligations: Provisions should clearly state that notes constitute direct, unconditional, and unsecured obligations of the issuer. This clarity is essential to meet the TLAC/MREL eligibility criteria. However, these contractual assertions often require additional verification to ensure they align with regulatory expectations.

Enhanced Verification Processes: Institutions must implement robust verification processes to confirm that their instruments meet these criteria. This may involve external audits, legal reviews, and ongoing monitoring to ensure continued compliance.

US Law Securities

Non-Qualification Under MREL: The EBA maintains that debt securities issued under Section 3(a)(2) of the US Securities Act of 1933, even if guaranteed by a branch of an EU institution, do not qualify as MREL. This position is based on the complexities and potential conflicts arising from third-country laws, which could undermine the enforceability and effectiveness of the instruments.

Impact on Issuance Strategy: Institutions issuing under US law must consider these regulatory limitations and explore alternative structures that comply with MREL requirements. This might include restructuring their issuance programs to ensure that all instruments meet the stringent criteria set forth by the EBA.

Tax Gross-Up Clauses

Activation and Limitations: Tax gross-up clauses are provisions that allow issuers to increase payments to cover taxes imposed on dividends or coupons. These clauses should be activated by a decision of the local tax authority of the issuer and must not exceed the issuer's distributable items. This means that gross-ups should only relate to withholding taxes on dividends or coupons, excluding any principal amounts.

Regulatory Requirements: Gross-up clauses ensure that investors receive the expected return on their investments net of any tax deductions. However, they must be carefully structured to comply with regulatory limitations, ensuring they do not inadvertently affect the financial stability of the institution or the effectiveness of the instruments in absorbing losses.

Interest Rate Reset Mechanism

Functionality and Structure: The interest rate reset mechanism allows instruments to switch from a fixed rate to a floating rate based on a benchmark rate plus a margin at a predetermined reset date. This date usually coincides with the first ordinary call date if the instrument is not called. The reset mechanism ensures that the interest rate reflects prevailing market conditions, thereby maintaining the attractiveness of the instrument to investors.

Technical Details: Typically, the margin is set as the difference between the initial yield of the instrument and a relevant swap rate. This keeps the credit spread consistent post-reset. However, some practices involve setting the margin in ways that could create an incentive to redeem the instrument early, which must be avoided to ensure regulatory compliance.

Demonstrating Compliance: Banks must be able to demonstrate to supervisors that the reset mechanism does not contain incentives to redeem, ensuring that the instrument continues to meet TLAC/MREL requirements.

Tap Issuances

Definition and Process: Tap issuances refer to subsequent issuances of an existing security, making the new issuances fully fungible with the original issuance. They share the same coupon, payment frequency, ISIN, and other characteristics.

New Issuance Consideration: Tap issuances are considered new issuances for regulatory purposes. If these issuances are priced at a lower credit spread due to favorable market conditions, they may create incentives to redeem the original bonds. This could potentially shorten the effective maturity of the instrument, impacting its regulatory treatment.

Regulatory Perspective: The EBA considers that if the reset mechanism of the original bonds applies more than five years after the tap issuance and if the credit spread for the tap issuance is lower than that of the original bond, there is an incentive to redeem. Institutions must carefully manage tap issuances to avoid these incentives and ensure compliance with TLAC/MREL requirements.

Supervisory Flexibility

Conditions for Flexibility: The EBA may allow some flexibility for small issuers in volatile market conditions. This flexibility is contingent on the issuer demonstrating that the credit spread for the tapped amount has remained stable compared to the initial issuance.

Regulatory Considerations: This supervisory flexibility aims to support smaller institutions in maintaining compliance with TLAC/MREL requirements without being adversely affected by short-term market fluctuations. However, issuers must provide clear evidence and robust documentation to justify any deviations from standard regulatory expectations.

Calls, Redemptions, and Repurchases

Calls Below Par

Definition and Regulatory Perspective: Calling instruments below par means the issuer redeems the debt security for less than its face value. This practice supports the principle of permanence, as it discourages issuers from redeeming the instruments prematurely. However, any write-ups linked to these calls should remain discretionary to avoid creating a contractual or statutory obligation that could undermine the instrument's loss-absorbing capacity.

Technical Considerations: The below-par call feature must be carefully structured to ensure it complies with regulatory requirements. This involves clear documentation that outlines the conditions under which the call can be exercised and ensures there are no implicit incentives that might prompt early redemption.

Calls with Long Notification Period

Impact on Permanence: Long notification periods for calls can undermine the perceived permanence of the instruments. The European Banking Authority (EBA) has expressed reservations about such provisions, emphasizing that they could lead to significant regulatory capital deductions during the notification period. This could affect the institution's stability and the effectiveness of its loss-absorbing instruments.

Mitigation Strategies: To address these concerns, institutions should consider shorter notification periods and ensure that any potential impact on regulatory capital is minimized. This could involve proactive communication with regulatory authorities and stakeholders to manage expectations and maintain confidence in the institution's financial stability.

Continuous Call Option

Regulatory Acceptance: Some issuances include a continuous call option that becomes exercisable after the first five years. The EBA notes that this is permissible if the instruments meet all other regulatory criteria related to permanence. Continuous call options provide flexibility for issuers but must be structured to avoid creating undue pressure to redeem, which could affect the instrument's effectiveness as a loss-absorbing tool.

Technical Implementation: Continuous call options should be documented with clear terms and conditions, ensuring they comply with all relevant regulatory standards. This includes specifying the exact conditions under which the call option can be exercised and demonstrating that the option does not incentivize early redemption.

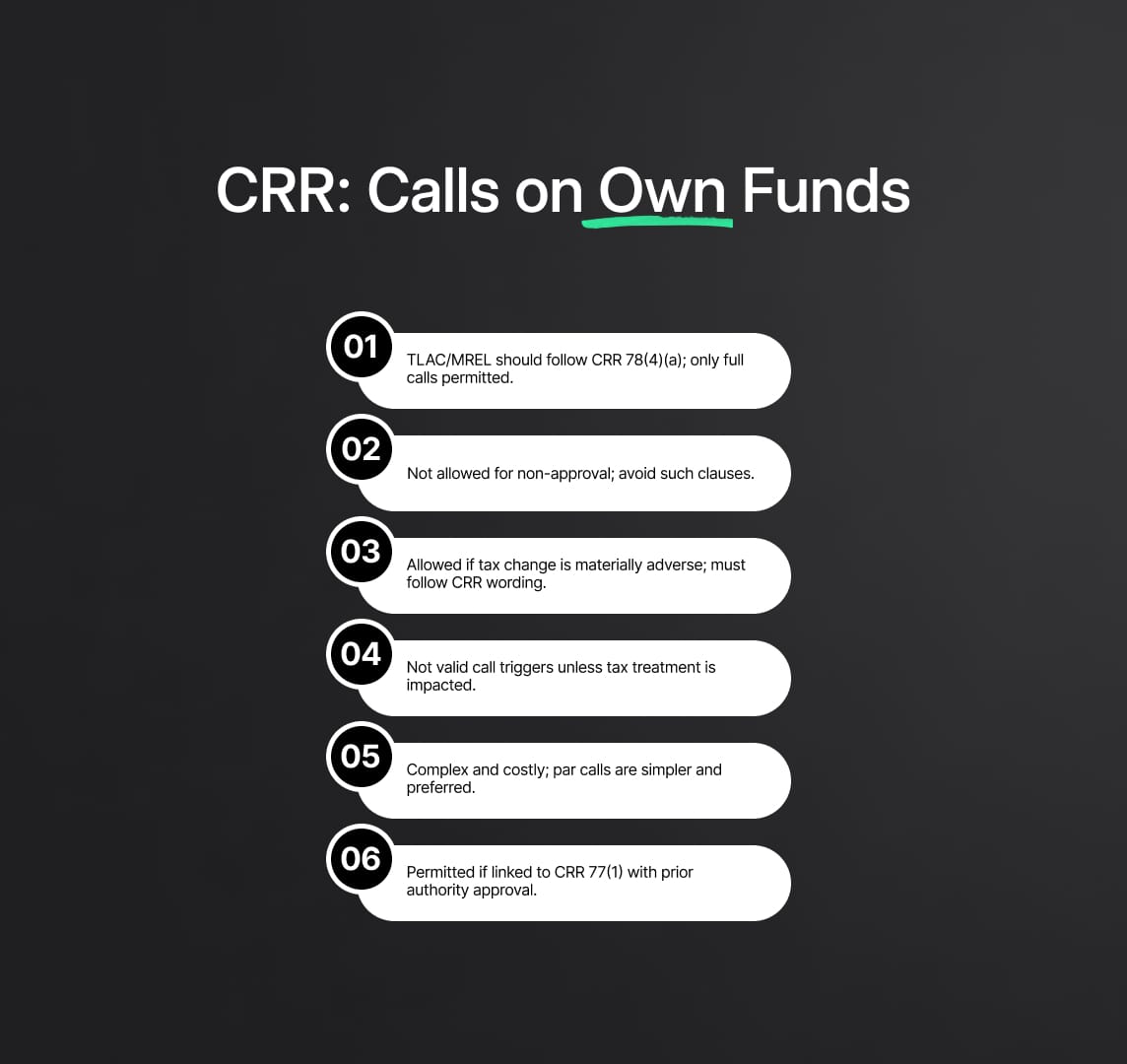

Capital Requirements Regulation (CRR): Regulatory and Tax Calls

Guidance and Compliance: The EBA provides detailed guidance on regulatory calls as outlined in Article 78(4)(a) of the Capital Requirements Regulation (CRR). Unlike own funds instruments, TLAC/MREL eligible liabilities do not have specific CRR/BRRD provisions for regulatory calls. However, institutions should apply similar principles to ensure consistency and prudence, demonstrating a robust understanding of regulatory expectations and maintaining compliance.

Partial Regulatory Calls

Restrictions and Requirements: Only regulatory calls for the full amount of instruments are acceptable, regardless of whether regulatory changes trigger a full or partial derecognition from AT1/Tier 2 capital. This ensures that the instruments continue to meet their intended regulatory purposes without creating loopholes that might weaken the financial system's resilience.

Implementation: Institutions must clearly document the conditions under which partial regulatory calls can be exercised, ensuring they align with CRR requirements and do not undermine the instrument's effectiveness.

Early Redemption Clauses

Discouragement and Rationale: Early redemption for reasons of non-approval is discouraged as it is not foreseen by CRR provisions. Standardization and ample guidance reduce the risk of non-approval, providing greater certainty and stability for issuers and investors alike.

Technical Details: Institutions should structure their instruments to avoid the need for early redemption clauses, focusing instead on meeting regulatory standards and maintaining robust communication with regulatory authorities.

Tax Calls

Conditions and Terminology: The condition for a tax call is a ‘material effect’ of the change in tax treatment. Partial calls are acceptable if the effect is material. Provisions should use precise terminology in line with CRR Article 78 to ensure clarity and compliance.

Implementation: Tax call clauses must be carefully drafted to reflect the specific tax circumstances that could trigger a call. This includes detailing the materiality threshold and the process for determining whether a tax change qualifies for a call.

Accounting Standards

Triggers and Validity: Changes in applicable accounting standards that do not trigger a change in tax treatment cannot be considered valid triggers for tax calls. This ensures that the instruments' tax treatment remains stable and predictable, reducing uncertainty for issuers and investors.

Regulatory Perspective: Institutions must stay informed about changes in accounting standards and assess their impact on the instruments' tax treatment, ensuring they continue to meet all regulatory requirements.

Make-Whole Clauses

Mechanism and Purpose: Make-whole provisions allow issuers to redeem bonds before maturity at a redemption amount representing the present value of the principal amount and remaining interest. These clauses are intended to compensate investors for the early redemption by making them whole for the remaining interest payments they would have received.

Complexity and Costs: Make-whole clauses are seen as complex and potentially more costly than par calls. They can complicate pricing and valuation, making the issuance process more challenging and increasing the overall cost.

Prudential Value: From a regulatory perspective, make-whole clauses do not bring additional prudential value and are not recommended for own funds and eligible liabilities instruments. Issuers should opt for par calls, which are simpler and more transparent.

Clean-Up Clauses

Definition and Execution: Clean-up clauses allow issuers to redeem outstanding notes if a specified threshold of instruments is redeemed. These clauses are primarily about the practical execution of calls rather than triggering conditions.

Regulatory Conditions: Clean-up clauses are acceptable if they are linked to actions referred to in Article 77(1) of the CRR and subject to the competent authority’s prior permission. They can be activated within the first five years as long as Articles 77 and 78 of the CRR are fully met.

Practical Considerations: Institutions should ensure that clean-up clauses are clearly defined and comply with all relevant regulatory requirements. This includes detailing the threshold for activation and the process for obtaining regulatory approval.

Calls Specific to TLAC/MREL Eligible Liabilities

Issuer Call Options

Impact on Residual Maturity: Issuer call options, when designed without incentives to redeem, have no effect on the residual maturity calculation of TLAC/MREL eligible liabilities. If an incentive to redeem exists, the first date at which the call option can be exercised will define the instrument’s residual maturity. This ensures that the instrument's eligibility is aligned with regulatory requirements, maintaining its intended function as a loss-absorbing capacity.

Technical Details: Issuer call options must be clearly documented with specific conditions under which they can be exercised. The absence of incentives to redeem is crucial, as it ensures that the instruments continue to serve their purpose of absorbing losses and maintaining financial stability.

Put Options

Definition and Impact on Maturity: Put options, which allow the holder to require the issuer to redeem the instrument, are permitted. However, the maturity of the instrument is defined as the first date the right to exercise the put option arises. No put option provisions have been observed in Medium-Term Note (MTN) programs reviewed, indicating a preference for maintaining instrument stability and predictability.

Regulatory Considerations: The implementation of put options must be carefully managed to avoid premature redemption, which could undermine the instrument’s role in providing financial stability. The terms should be clear and aligned with regulatory expectations to ensure compliance.

Regulatory Permission

Requirement for Redemption

CRR Article 78a Compliance: According to Article 78a of the CRR, any redemption of TLAC/MREL eligible liabilities requires permission from the resolution authority. This ensures that redemptions do not occur without regulatory oversight, maintaining the integrity and stability of the financial system.

Monitoring by the EBA: The EBA actively monitors the wording of call and redemption options to ensure they comply with regulatory requirements. This proactive approach helps prevent potential loopholes that could undermine regulatory objectives.

Regulatory Permission to Reduce Instruments

Avoiding Litigation and Ensuring Compliance: Instruments must explicitly reference regulatory conditions linked to prior permission for any reduction actions. This includes calls, redemptions, repayments, or repurchases. Such explicit language helps avoid potential litigation and ensures that all actions are in full compliance with regulatory requirements.

Documentation and Clarity: Clear documentation of these conditions is essential. It provides transparency and assurance to all stakeholders that the instruments will be managed in a way that maintains financial stability and regulatory compliance.

Prior Permission for TLAC/MREL

Acknowledgment in Terms: The terms of TLAC/MREL eligible liabilities must include an explicit acknowledgment of the requirement to obtain prior permission from resolution authorities for any call, redemption, repayment, or repurchase. This ensures that all actions are pre-approved and aligned with regulatory expectations.

Redemptions and Repurchases

Ordinary, Regulatory, and Tax Calls

Well-Defined Terms: The terms and conditions for redeeming or repurchasing instruments under ordinary, regulatory, and tax calls must be well-defined. This includes references to obtaining prior permission from competent authorities as per Articles 77, 78, or 78a of the CRR. Clear terms ensure transparency and regulatory compliance, preventing unauthorized actions that could affect financial stability.

Discretionary Repurchases

Protecting Regulatory Own Funds: Clauses that protect regulatory own funds and eligible liabilities, even if discretionary repurchases occur without prior permission, are welcomed. These clauses create an obligation for the holder to repay or return amounts received without proper authorization, safeguarding the institution’s regulatory capital and ensuring compliance.

Prohibition of Unrestricted Purchases

Regulation and Restrictions: Provisions should not imply that purchases of instruments are possible at any time. Under the CRR, such purchases are regulated and restricted to specific conditions and limits to maintain the instruments' intended function and regulatory compliance.

Detailed Provisions: The terms must explicitly state the conditions and limits under which purchases can occur, ensuring no ambiguity and full adherence to regulatory standards.

Liability Management Exercises (LMEs)

Exclusion from Terms and Conditions: LMEs should not be included in the terms and conditions of TLAC/MREL eligible liabilities. However, market making and exchanges with instruments of the same or higher quality are permissible under CRR Articles 78(1) and 78(4)(d) and (e), and Article 78a(1)(a) for eligible liabilities.

Permissible Activities: While LMEs are excluded, permissible activities such as market making and exchanges provide flexibility for institutions to manage their liabilities effectively within regulatory frameworks.

Purchases by Subsidiaries

Regulatory Permission for Early Purchases: Purchases by subsidiaries of the issuing institution before five years from issuance require prior permission. Such purchases qualify as repurchases under CRR Articles 52(1)(b) and 63(b), ensuring they are conducted within regulatory guidelines and do not undermine the financial stability and intended loss-absorbing capacity of the instruments.

Compliance and Monitoring: Continuous monitoring and compliance with these conditions are essential to ensure that all actions align with regulatory requirements and support the institution’s overall financial health and stability.

TLAC/MREL Disqualification Events for Own Funds Purposes

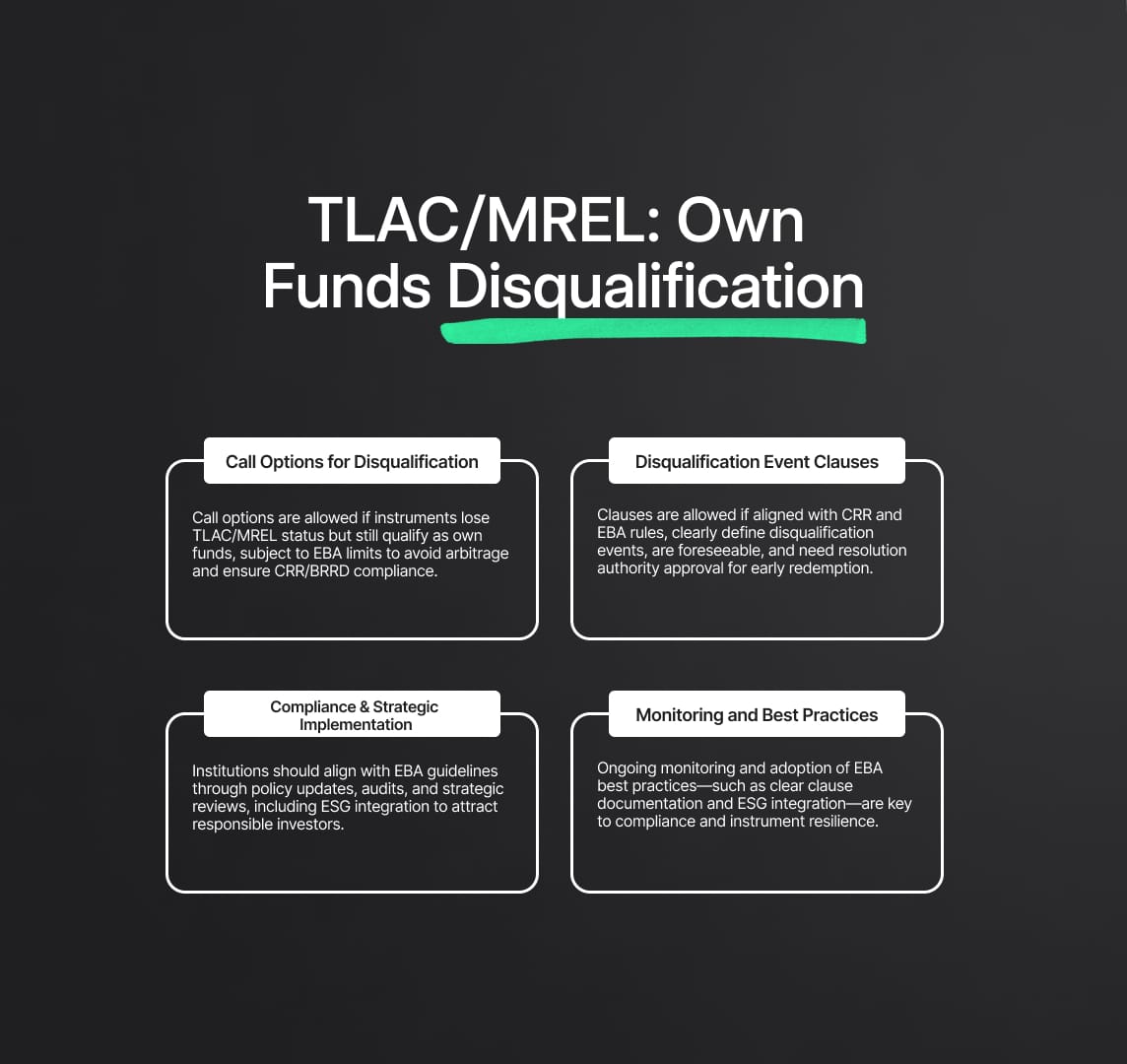

Call Options for Disqualification Events

Certain Additional Tier 1 (AT1) and Tier 2 issuances incorporate clauses allowing for call options if the instrument ceases to be eligible as TLAC/MREL while still qualifying as own funds. The European Banking Authority (EBA) maintains a restrictive stance on these new call options to ensure consistency across both own funds and TLAC/MREL frameworks. This stringent approach helps to avoid arbitrage opportunities and ensures that the instruments retain their loss-absorbing capacity, which is crucial for maintaining financial stability.

Technical Details: These call options must be explicitly detailed in the terms and conditions of the instruments. The clauses should outline the specific scenarios under which the instrument would cease to qualify as TLAC/MREL, while still being eligible as own funds. This includes clear definitions and conditions that align with the regulatory frameworks.

Regulatory Consistency: Ensuring that these options are in line with both the Capital Requirements Regulation (CRR) and the Bank Recovery and Resolution Directive (BRRD) is vital. This harmonization prevents discrepancies that could lead to regulatory arbitrage, thereby maintaining the integrity of the financial system.

Acceptance of Disqualification Event Clauses

Disqualification event clauses are deemed acceptable if they align with recent amendments to the CRR regarding eligible liabilities. These clauses must ensure consistency between own funds and TLAC/MREL frameworks. Under specific conditions outlined in Article 78(4)(d) of the CRR, redemptions can occur within the first five years of issuance, provided the changes were unforeseeable at the time of issuance.

Technical Conditions: For these clauses to be effective, they must include:

- Clear Definitions: Precise definitions of what constitutes a disqualification event.

- Regulatory Compliance: Alignment with CRR amendments and EBA guidelines.

- Foreseeability: Demonstration that the disqualification event was unforeseeable at issuance.

- Prior Permission: Requirement for prior permission from resolution authorities for any redemption actions.

Strategic Implications: Institutions need to strategically assess the inclusion of such clauses, ensuring they do not undermine the long-term stability and loss-absorbing capacity of their financial instruments.

Compliance and Strategic Implementation

EU financial institutions must rigorously comply with the updated EBA guidelines. This may involve revising internal policies, updating documentation, and conducting regular audits. Ensuring compliance with these guidelines not only maintains regulatory adherence but also supports the institution's financial stability and market confidence.

Internal Policy Revisions: Institutions may need to overhaul their internal policies to reflect the updated guidelines. This includes revising the terms and conditions of AT1, Tier 2, and TLAC/MREL instruments.

Documentation Updates: All relevant documentation must be updated to include the new regulatory requirements and to ensure transparency and compliance.

Regular Audits: Conducting regular audits helps institutions stay compliant with the evolving regulatory landscape and promptly address any issues.

Strategic Considerations: Institutions should also consider the strategic implications of these guidelines. For instance, the increasing importance of ESG (Environmental, Social, and Governance) capital bonds could be integrated into their strategic planning to attract socially conscious investors and enhance their reputation.

Continuous Monitoring and Best Practices

The EBA's findings and recommendations include policy views on existing or new provisions and identified best practices. Institutions must continuously monitor their compliance with these eligibility criteria and adopt best practices to ensure their instruments meet the required standards.

Continuous Monitoring: Ongoing monitoring is crucial to ensure compliance with EBA guidelines. This includes regular reviews of instruments and adherence to updated regulatory requirements.

Adoption of Best Practices: Institutions should adopt best practices identified by the EBA. This not only ensures compliance but also enhances the robustness and reliability of their financial instruments.

Best Practices Examples: Examples of best practices include clear documentation of call options, thorough assessments of disqualification event clauses, and strategic integration of ESG considerations.

Reduce your

compliance risks