Capital Requirements Regulation 3 (CRR III) for Market Risks

On July 24, 2024, the European Commission adopted a Delegated Regulation amending the Capital Requirements Regulation (CRR) regarding the application date of market risk requirements. This amendment, effective January 1, 2026, gives financial institutions more time to adapt to new standards.

On July 24, 2024, the European Commission adopted a Delegated Regulation amending the Capital Requirements Regulation (CRR) concerning the application date of the own funds requirements for market risk. This regulation marks a crucial shift in the regulatory landscape for financial institutions operating within the European Union. This article delves into the technical details and implications of this amendment, focusing on its impact on the market risk framework under the CRR III.

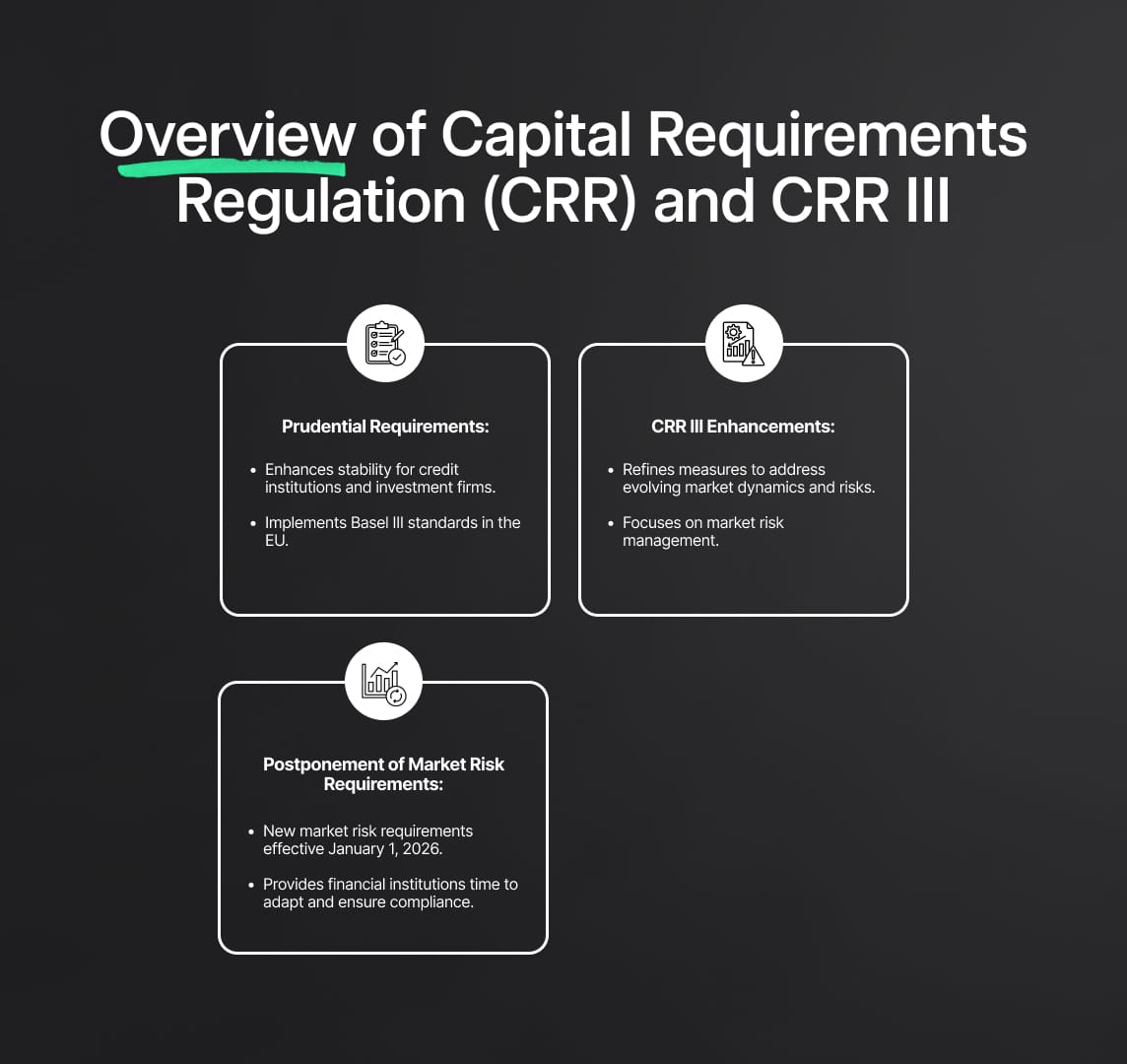

Overview of the Capital Requirements Regulation (CRR)

The Capital Requirements Regulation (CRR) is a cornerstone of the European Union's financial regulatory framework. It establishes prudential requirements for credit institutions and investment firms, aiming to enhance the stability and resilience of the financial system. The CRR, along with the Capital Requirements Directive (CRD IV), implements the Basel III standards in the EU, covering aspects such as capital, liquidity, leverage, and risk management.

The CRR ensures that financial institutions hold adequate capital to cover their risks, thereby protecting depositors and maintaining financial stability. The regulation includes various parts and titles, each addressing specific risk areas and requirements. The CRR III, an iteration of these regulations, introduces refined measures to address evolving market dynamics and risks, particularly in the realm of market risk.

Key Changes Introduced by the Delegated Regulation

Postponement of Market Risk Requirements

The primary focus of the Delegated Regulation adopted on July 24, 2024, is to postpone the entry into application of the new market risk requirements by one year. Originally set to be binding from January 1, 2025, these requirements will now take effect on January 1, 2026. This postponement is significant for several reasons:

- Operational Adaptation: Financial institutions are granted additional time to adapt their internal systems, processes, and risk management frameworks to the new regulatory standards. This is crucial for ensuring that all necessary adjustments are effectively implemented without undue pressure.

- Regulatory Compliance: The postponement allows institutions to ensure full compliance with the updated framework, reducing the risk of non-compliance due to rushed implementations. This is particularly important for smaller institutions that may have limited resources for rapid adaptation.

- Alignment with International Standards: Delaying the application date aligns the EU’s regulatory framework with the implementation timelines in other major jurisdictions, such as the United States. This helps maintain a level playing field and avoids competitive disadvantages for EU institutions.

Amendments to the Capital Requirements Regulation 3 (CRR III)

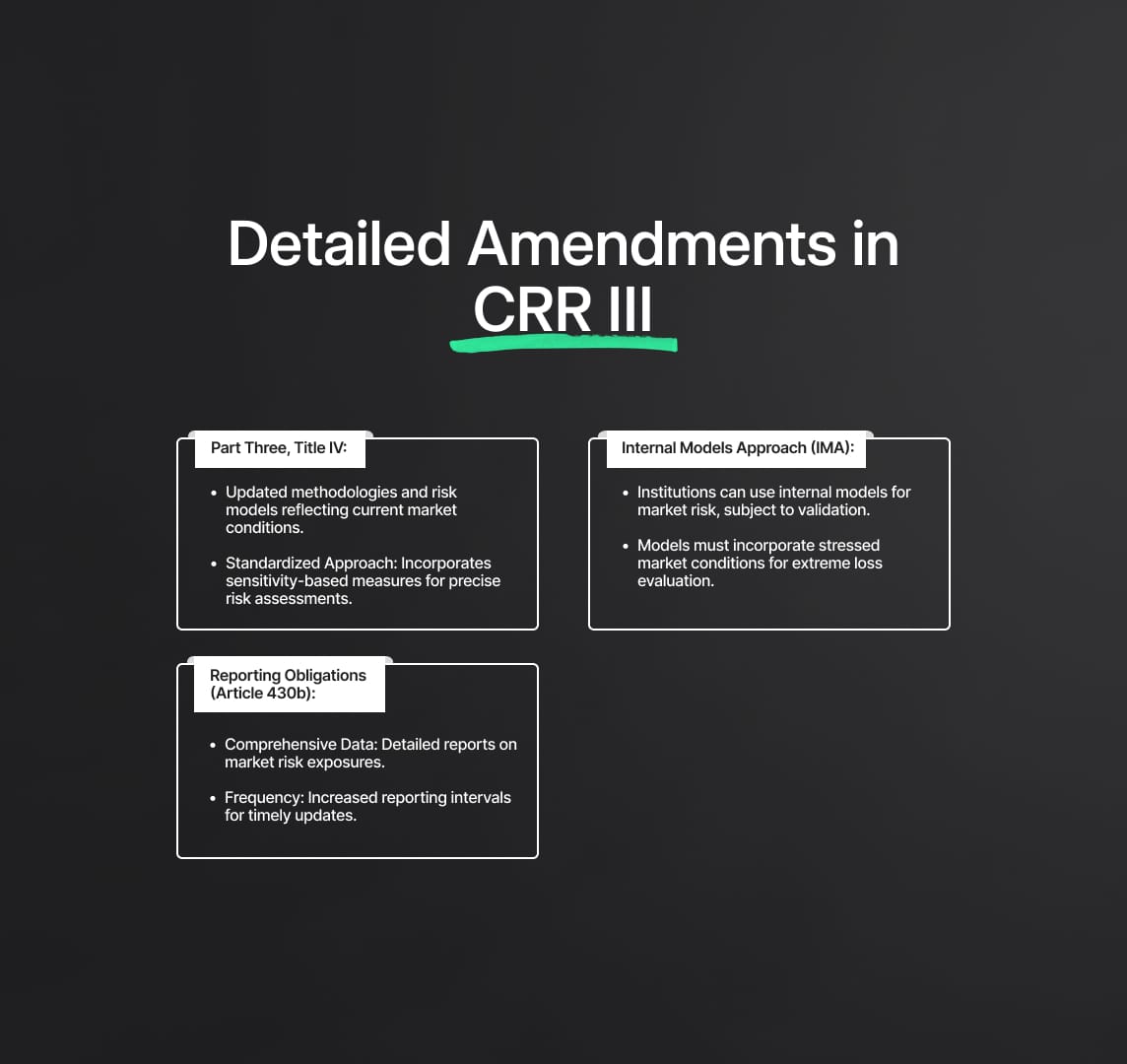

The amendments introduced by the Capital Requirements Regulation 3 (CRR III) specifically address the market risk framework, aiming to enhance the robustness, accuracy, and transparency of market risk management. These changes are detailed in Part Three, Title IV of the CRR, as well as in Articles 430b, 445, and 455. The amendments focus on refining the calculation of own funds requirements for market risk, improving market risk reporting, and updating disclosure requirements to align with current market conditions and regulatory expectations.

Part Three, Title IV of the CRR

Part Three, Title IV of the CRR outlines the general requirements for calculating market risk. The amendments in CRR III introduce updated methodologies and risk models that better reflect current market conditions and the evolving nature of financial markets. Key elements include:

- Standardized Approach for Market Risk: The CRR III mandates a more granular standardized approach to market risk, incorporating sensitivity-based measures that account for various risk factors such as interest rates, equity prices, foreign exchange rates, and commodity prices. This approach enhances the precision of risk assessments by considering specific risk exposures and their potential impacts on the trading book.

- Internal Models Approach (IMA): Institutions are allowed to use internal models to calculate market risk capital requirements, subject to regulatory approval. The CRR III amendments require these models to undergo rigorous validation and back-testing processes to ensure their accuracy and reliability. Additionally, the models must incorporate stressed market conditions to evaluate potential extreme losses effectively.

Article 430b: Reporting Obligations

Article 430b of the CRR III addresses the reporting obligations of financial institutions concerning market risk. The amendments emphasize the need for detailed and accurate reporting to enhance transparency and supervisory oversight. Key requirements include:

- Comprehensive Data Submission: Institutions must provide detailed reports on their market risk exposures, including the composition of their trading book, the methodologies used for risk assessment, and the outcomes of these assessments. This data allows regulators to monitor the institution's risk profile and its adherence to regulatory standards.

- Frequency and Timeliness: The reporting frequency is increased to ensure that supervisory authorities receive up-to-date information on an institution's market risk exposure. Timely reporting is crucial for early identification of emerging risks and prompt regulatory intervention when necessary.

Article 445: Disclosure Requirements

Article 445 focuses on the disclosure requirements related to market risk. The updated provisions aim to ensure that stakeholders, including investors and regulators, have access to relevant and timely information on an institution's market risk exposure and management practices. Key aspects include:

- Public Disclosure of Risk Information: Institutions are required to publicly disclose comprehensive information about their market risk exposures, including the methodologies and assumptions used in risk calculations, the sensitivity of their trading book to various risk factors, and the outcomes of stress testing scenarios. This transparency fosters market discipline and allows stakeholders to make informed decisions.

- Qualitative and Quantitative Disclosures: The CRR III mandates both qualitative and quantitative disclosures. Qualitative disclosures include descriptions of the risk management framework, governance structures, and policies for mitigating market risk. Quantitative disclosures provide numerical data on risk exposures, capital requirements, and the results of internal and regulatory stress tests.

Article 455: Supervisory Review and Evaluation Process (SREP)

Article 455 covers the supervisory review and evaluation process (SREP) for market risk. The amendments aim to strengthen the supervisory framework, ensuring that institutions maintain adequate capital buffers to mitigate market risk effectively. Key elements include:

- Rigorous Supervisory Assessment: Supervisors are required to conduct comprehensive assessments of an institution's market risk management practices, including the adequacy of its capital buffers, the effectiveness of its internal models, and its adherence to regulatory requirements. This assessment is based on both on-site inspections and off-site monitoring.

- Capital Adequacy: The SREP process evaluates whether institutions hold sufficient capital to cover their market risk exposures under both normal and stressed market conditions. Supervisors may impose additional capital requirements or corrective measures if deficiencies are identified.

- Continuous Monitoring: Supervisors are tasked with continuous monitoring of institutions' market risk profiles, leveraging the detailed reports submitted under Article 430b. This ongoing supervision ensures that institutions remain compliant with regulatory standards and that emerging risks are promptly addressed.

Context of the Delegated Act: Capital Requirements Regulation 3 (CRR III)

Market Risk and Financial Instruments

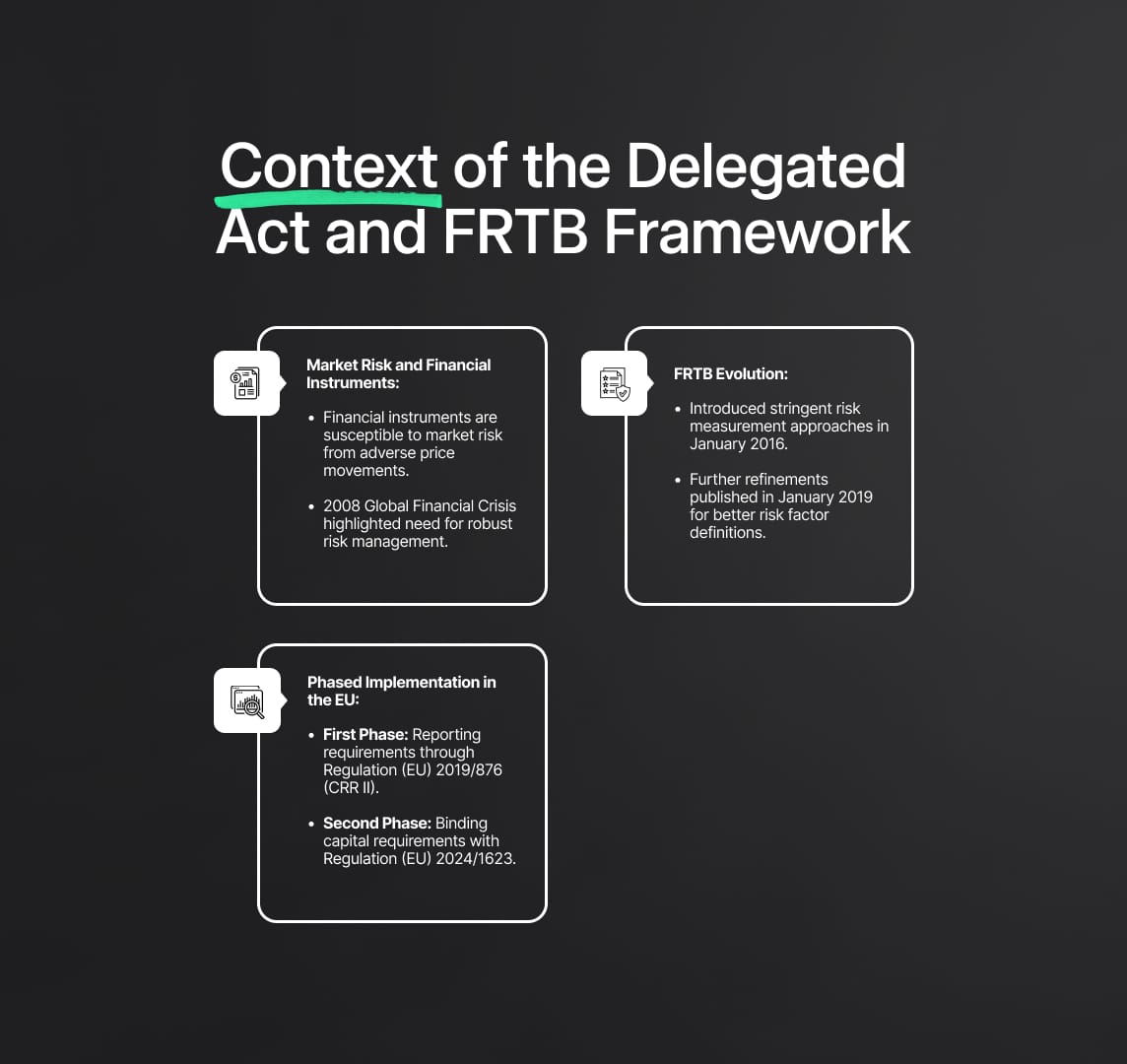

Financial instruments held by banks for trading purposes, such as shares, bonds, and derivatives, are inherently susceptible to market risk—the risk of value depreciation due to adverse market price movements. Market risk encompasses various risk factors including, but not limited to, fluctuations in interest rates, equity prices, foreign exchange rates, and commodity prices. The 2008 Global Financial Crisis starkly exposed significant weaknesses in the prudential requirements for market risk. Many financial institutions found themselves with inadequate capital reserves to absorb the substantial losses incurred, underscoring the need for more robust risk management frameworks.

In response to these vulnerabilities, the Basel Committee on Banking Supervision (BCBS) undertook a comprehensive revision of international market risk standards. This effort culminated in the Fundamental Review of the Trading Book (FRTB) framework, adopted in January 2016. The FRTB introduced more stringent and granular risk measurement approaches to ensure financial institutions maintain sufficient capital to cover potential market risk losses.

Evolution of the FRTB Framework

The FRTB framework, since its inception, has undergone several iterations to address various technical and implementation challenges. Following its initial adoption in January 2016, the framework was subjected to further refinements, resulting in the publication of a final version in January 2019. Key enhancements in this version included more precise risk factor definitions, improved models for capturing market risk, and better calibration of capital requirements to reflect actual risk exposures.

Initially, the BCBS set an implementation deadline of January 1, 2022. However, the global disruption caused by the COVID-19 pandemic necessitated a postponement to January 1, 2023. This delay provided financial institutions and regulators additional time to adapt to the new standards amidst the operational challenges posed by the pandemic. Despite this extension, the substantial changes introduced by the FRTB and the ongoing revisions at the Basel level prompted the European Union to adopt a phased implementation approach to ensure a smooth transition.

Phased Implementation of the FRTB in the EU

The EU's phased implementation approach for the FRTB is designed to systematically integrate the new standards into the existing regulatory framework, minimizing disruption while enhancing market risk management capabilities.

First Phase: Reporting Requirements

The first phase of the FRTB implementation involved introducing it as a reporting requirement through Regulation (EU) 2019/876 (CRR II). This phase was essential for enabling competent authorities to monitor banks' implementation of the FRTB before these provisions became binding for calculating own funds requirements. By requiring institutions to report their market risk exposures using the new FRTB methodologies, regulators could assess the readiness of institutions and the potential impact of the new standards.

Second Phase: Binding Capital Requirements

The second phase, completed with the adoption of Regulation (EU) 2024/1623 in May 2024, established the FRTB standards as binding capital requirements within EU legislation. This regulatory milestone was critical in formalising the enhanced market risk framework and ensuring consistent application across all financial institutions operating within the EU. Article 461a of Regulation (EU) No 575/2013, amended by Regulation (EU) 2024/1623, mandates the European Commission to monitor international implementation of the Basel FRTB standards and adopt delegated acts to ensure a level playing field if significant deviations arise in third countries' implementations.

Challenges and Considerations in Implementing the FRTB

Implementing the FRTB framework presents several challenges and considerations for financial institutions and regulators:

- Complexity of Risk Models: The FRTB introduces more complex risk models that require significant data inputs and advanced computational capabilities. Financial institutions must invest in upgrading their risk management systems and ensure they have the technical expertise to implement these models effectively.

- Data Quality and Granularity: Accurate risk measurement under the FRTB depends on high-quality, granular data. Institutions must ensure their data collection and management processes are robust enough to support the detailed reporting and modeling requirements of the FRTB.

- Regulatory Coordination: Ensuring a coordinated implementation across jurisdictions is crucial to maintaining a level playing field. Discrepancies in the adoption timelines or interpretations of the FRTB standards can lead to competitive imbalances and regulatory arbitrage.

- Operational Impact: The transition to the FRTB framework involves significant operational changes. Institutions must realign their internal processes, risk management frameworks, and reporting systems to comply with the new standards. This transition phase requires careful planning and resource allocation to avoid operational disruptions.

Phased Implementation of the FRTB in the EU Under Capital Requirements Regulation 3 (CRR III)

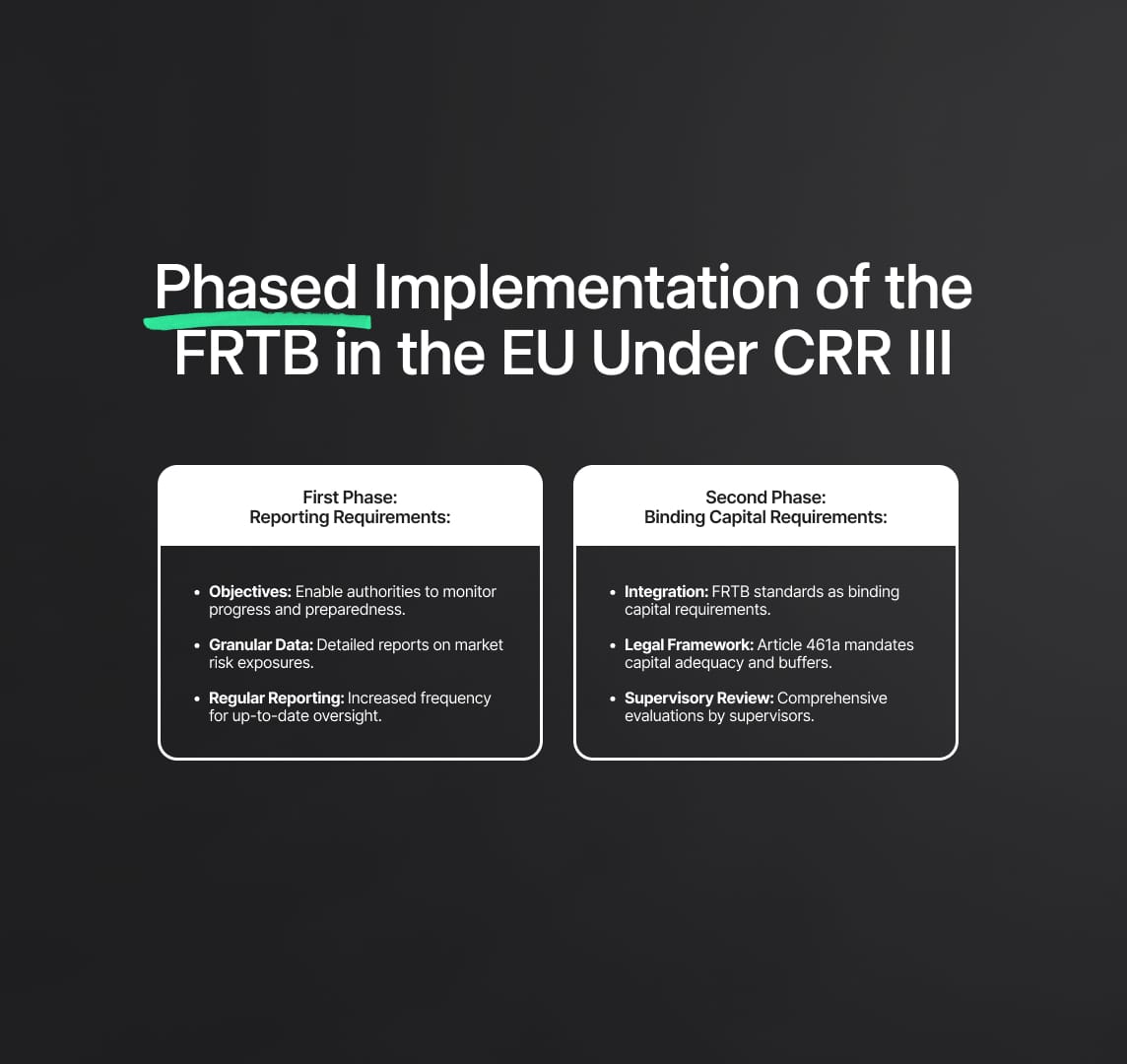

First Phase: Reporting Requirements

The phased implementation of the Fundamental Review of the Trading Book (FRTB) under the Capital Requirements Regulation 3 (CRR III) begins with an initial focus on reporting requirements. This phase was introduced through Regulation (EU) 2019/876, also known as CRR II, and serves as a preparatory step for full compliance with the FRTB standards.

Objectives and Scope of the Reporting Phase

The primary objective of the reporting phase is to enable competent authorities to monitor the progress and preparedness of financial institutions in implementing the FRTB standards. This phase mandates that institutions report their market risk exposures using the new FRTB methodologies. The data collected during this phase provides invaluable insights into how institutions are adjusting to the new risk measurement approaches and highlights any areas requiring further refinement or support.

Key Elements of the Reporting Requirements

- Granular Data Submission: Institutions are required to submit detailed reports on their market risk exposures. This includes information on the composition of their trading book, the methodologies employed for risk assessment, and the outcomes of these assessments. The granularity of the data helps regulators understand the risk profile of each institution.

- Regular Reporting Intervals: The reporting frequency is increased to ensure that supervisory authorities receive timely updates on market risk exposures. This frequent reporting is crucial for maintaining up-to-date oversight and allows for the early identification of emerging risks.

- Enhanced Transparency: Detailed and accurate reporting enhances transparency, providing a clearer picture of the institution's risk management practices. This transparency is vital for building trust among stakeholders and ensuring that institutions adhere to regulatory expectations.

Second Phase: Binding Capital Requirements

The second phase of the FRTB implementation was solidified with the adoption of Regulation (EU) 2024/1623 in May 2024. This phase establishes the FRTB standards as binding capital requirements within EU legislation, marking a significant step towards comprehensive market risk management.

Objectives and Legal Framework

The primary goal of this phase is to integrate the FRTB standards into the binding regulatory framework, ensuring that all financial institutions within the EU maintain adequate capital buffers to cover potential market risk losses. Article 461a of Regulation (EU) No 575/2013, as amended by Regulation (EU) 2024/1623, provides the legal mandate for this implementation. The European Commission is tasked with monitoring the international implementation of the Basel FRTB standards and has the authority to adopt delegated acts to address any significant deviations in other jurisdictions.

Key Elements of the Binding Capital Requirements

- Standardized and Internal Models Approaches: The FRTB framework allows institutions to use either standardized approaches or internal models for calculating market risk capital requirements. The internal models must be rigorously validated and back-tested to ensure their reliability and must reflect stressed market conditions.

- Capital Adequacy and Buffers: Institutions are required to hold sufficient capital to cover market risk exposures, both under normal and stressed conditions. The adequacy of these capital buffers is crucial for absorbing potential losses and maintaining financial stability.

- Supervisory Review Process: The supervisory review and evaluation process (SREP) plays a pivotal role in assessing the effectiveness of an institution’s market risk management practices. This process involves comprehensive evaluations by supervisors, including both on-site inspections and continuous off-site monitoring.

Addressing Implementation Discrepancies

To address these discrepancies and preserve a level playing field, the European Commission deemed it necessary to postpone the FRTB standards' application by one year, setting the new implementation date to January 1, 2026. This delay impacts several ancillary CRR requirements related to the FRTB, including:

- Trading Book/Non-Trading Book Boundary Conditions: These conditions define the scope of market risk own funds requirements, ensuring that institutions correctly classify their exposures.

- Reporting and Disclosure Requirements: Consistent and transparent reporting is maintained to ensure continuous oversight and to provide stakeholders with relevant information on market risk exposures.

- Output Floor Application: The output floor sets a minimum capital requirement relative to risk-weighted assets, ensuring that capital levels are not understated.

- Supervisory Benchmarking: Regular benchmarking exercises are conducted to compare institutions’ market risk models and practices, promoting consistency and best practices across the industry.

Key Components of the Guidance

- Detailed Implementation Guidelines: The EBA and SSM will issue detailed guidelines on how institutions should implement the FRTB standards, including specific methodologies, data requirements, and reporting formats.

- Best Practices and Standards: The guidance will outline best practices for market risk management, encouraging institutions to adopt robust risk measurement and mitigation techniques.

- Continuous Support and Clarifications: Ongoing support will be provided to institutions to address any implementation challenges and to clarify regulatory expectations. This support is crucial for ensuring that all institutions, regardless of size, can effectively transition to the new standards.

CRR 3 Delegated Regulation: Next Steps

The Delegated Regulation will enter into force on the day following its publication in the Official Journal of the European Union and will apply from January 1, 2025. During this period, the current market risk requirements, including the calculation of own funds requirements for market risk, reporting, and disclosure obligations, will remain in effect:

- Transition Period Utilization: Financial institutions are encouraged to use this transition period to prepare for the upcoming changes, ensuring full compliance by the new implementation date.

- Regulatory Engagement: Continuous engagement with regulatory bodies will be essential for institutions to stay informed about further developments and additional guidance.

Reduce your

compliance risks