Capital Requirements Regulation (CRR): Basel 3.1 Implementation

HM Treasury revokes key Capital Requirements Regulation (CRR) provisions, implementing PRA’s Basel 3.1 rules to enhance financial stability and streamline capital requirements.

The Capital Requirements Regulation (CRR) has been a cornerstone of financial regulation in the UK, focusing on the stability and resilience of financial institutions by ensuring that banks maintain adequate capital buffers. In light of the UK's departure from the EU, regulatory autonomy has gained importance, leading to a significant shift in how the country approaches its prudential regulation framework. One of the most substantial shifts comes with the introduction of the Financial Services and Markets Act (FSMA) 2023, which aims to apply a UK-specific approach to regulation, moving away from assimilated EU laws.

On 12 September 2024, HM Treasury (HMT) published a comprehensive Policy Paper titled ‘Applying the FSMA 2000 model of regulation to the Capital Requirements Regulation’. This document lays out the framework for transitioning the UK’s regulatory landscape, particularly as it pertains to Capital Requirements Regulation and associated financial legislation.

Source

[1]

[2]

FSMA 2023 and CRR Transition

The Financial Services and Markets Act (FSMA) 2023 was designed to replace parts of the EU-derived regulatory regime with a more UK-centric model. This transition has major implications for the Capital Requirements Regulation (CRR), which has been partially revoked and replaced by Prudential Regulation Authority (PRA) rules. The CRR historically provided a framework for how banks, building societies, and investment firms manage risk through capital adequacy requirements, ensuring they hold sufficient capital against their risk exposures.

The purpose of these changes is to ensure that UK financial services regulations align with national objectives, especially as the country integrates the Basel III.1 standards into its domestic regulatory framework. The Basel III.1 standards, set by the Basel Committee on Banking Supervision, offer a robust framework for mitigating systemic risk, with a particular focus on strengthening capital requirements, liquidity standards, and risk management practices. As part of this transition, the PRA and the Bank of England will assume a greater role in dictating the rules and guidelines surrounding capital requirements, ensuring a more flexible, UK-focused regulatory approach.

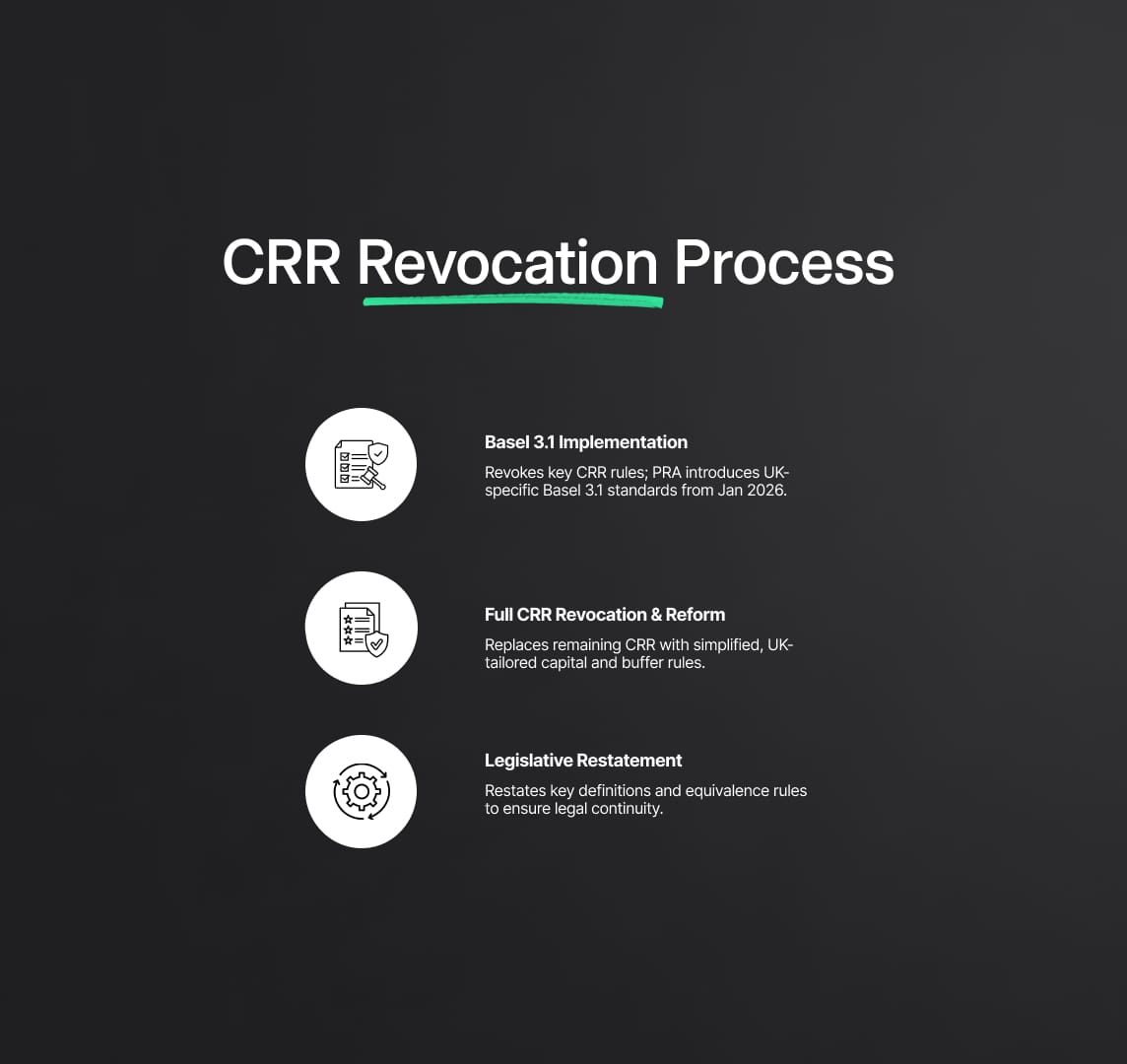

CRR Revocation Process

The transition from the EU-based CRR to the UK's FSMA model will take place in three key stages, as outlined in the HMT Policy Paper. These stages are designed to ensure a seamless and systematic shift in the regulatory environment, enabling both regulators and financial institutions to adapt without significant disruption.

Stage 1: Basel 3.1 Implementation and CRR Revocation

The first stage focuses on revoking specific articles of the CRR that are essential for the Basel 3.1 implementation. The Basel III.1 package represents a set of international standards developed to strengthen bank capital requirements and mitigate risks within the global banking system. These standards, while international, need to be adapted to the UK's specific regulatory environment. For example, the Basel III.1 standards include adjustments to the calculation of risk-weighted assets (RWAs), which are fundamental to how banks determine the capital required for their credit, market, and operational risks.

To meet these goals, certain articles of the CRR will be revoked by commencement regulations, giving the PRA the ability to replace these with domestic rules. The PRA’s rulebook will reflect the UK's implementation of Basel III.1, ensuring the new requirements for risk-weighted assets, leverage ratios, and liquidity standards are appropriately covered under UK law. This revocation will allow the PRA to introduce tailored rules, especially regarding how capital adequacy is calculated and maintained, ensuring a focus on UK-specific financial stability concerns.

The PRA’s Basel 3.1 rules, which will take effect on 1 January 2026, are a critical component of this stage. These rules aim to solidify the resilience of the UK’s financial system by tightening the capital requirements for banks and aligning them with evolving global standards.

Stage 2: Full Revocation of Remaining CRR Provisions

Once Basel III.1 is implemented, the second stage will involve revoking the remaining CRR provisions that are left on the statute book. According to the Policy Paper, the PRA plans to introduce a range of reforms during this phase, leveraging rules and policy statements to replace the revoked CRR and Capital Buffers and Macro-Prudential Measures Regulations 2014 (CBR) provisions.

The PRA’s proposed reforms are aimed at streamlining the capital framework, making it simpler and more coherent for UK financial institutions. For instance, the Strong and Simple framework, part of these reforms, is a regime proposed by the PRA to simplify prudential requirements for small domestic deposit takers (SDDTs), reducing their compliance burden without compromising their resilience.

These reforms are expected to enhance the regulatory architecture by introducing tailored rules that respond to the unique needs of the UK’s financial services sector, particularly focusing on areas such as:

- Capital Buffers: Revising the capital buffer requirements to ensure that they better align with macroeconomic conditions and risks specific to the UK. The PRA’s future rules will replace the current legislative framework for capital buffers, including the Countercyclical Capital Buffer (CCyB), Other Systemically Important Institutions (O-SII) buffer, and Capital Conservation Buffer (CCoB), with updated policies that better reflect UK-specific risk conditions.

- Macroprudential Measures: Adjusting macroprudential regulations to offer the Bank of England more flexibility in addressing systemic risks. This includes potential adjustments to the UK’s framework for capital adequacy in light of lessons learned from the 2008 financial crisis and subsequent global economic changes.

The goal of this stage is to ensure that UK capital requirements are not only compliant with international standards but also reflect the domestic regulatory objectives of financial stability and economic resilience. For example, capital buffers will continue to play a key role in ensuring that financial institutions maintain extra capital during periods of economic growth to prepare for downturns, but the UK may introduce additional tools to address specific domestic vulnerabilities.

Stage 3: Legislative Restatement and CRR Equivalence Regimes

The third and final stage involves several legislative efforts, including:

- Restatement of CRR Equivalence Regimes: Some parts of the CRR equivalence regime will need to be restated in UK law to maintain international comparability and ensure a level playing field for UK banks operating globally. These equivalence regimes allow UK banks to recognize the regulatory framework of other jurisdictions, which is crucial for maintaining international capital flows and risk management consistency.

- Restatement of Key CRR Definitions: Essential CRR definitions will be restated in legislation to ensure that the overarching regulatory framework remains operational, even after full revocation of the CRR. For example, definitions related to capital adequacy and risk-weighted assets (RWAs) will be maintained in a UK-specific legal context to ensure regulatory continuity and clarity.

- Consequential Amendments: As part of this process, amendments will be made to other related laws and regulations to ensure full legal and regulatory coherence once the CRR is entirely revoked. This step will involve revising and restating specific technical standards and regulatory reporting requirements, ensuring that the PRA’s rules are fully aligned with the UK’s broader financial regulatory framework.

While the exact details of the legislative changes required for this stage are not yet included in the Policy Paper, the UK government plans to consult with stakeholders in due course to ensure the legislative framework operates as intended.

Draft Legislation and Next Steps

Alongside the Policy Paper, HM Treasury (HMT) has published three critical pieces of draft legislation that set the foundation for the phased revocation of the Capital Requirements Regulation (CRR) and the transition to a new regulatory framework under the Financial Services and Markets Act (FSMA) 2023. These draft regulations mark essential steps in transitioning from EU-derived legislation to a UK-specific prudential framework while ensuring alignment with Basel III.1 standards.

- Commencement regulations for Basel 3.1 revocations: These regulations represent the first step toward formalizing the PRA’s rules for the UK's Basel III.1 implementation. The commencement regulations empower the PRA to begin revoking specific CRR provisions that pertain to Basel III.1 standards. This revocation enables the Prudential Regulation Authority (PRA) to replace the existing EU-based regulations with UK-specific rules that are aligned with Basel III.1. This includes reforms in the calculation of risk-weighted assets (RWA), leverage ratios, and credit risk, all of which are critical in defining the capital banks must hold.

- Restatement of certain CBR requirements in legislation: To ensure continuity in the UK's prudential framework, HMT has proposed the restatement of certain Capital Buffers and Macro-Prudential Requirements (CBR). The CBR regulations are essential for macro-prudential oversight, providing key tools like the Countercyclical Capital Buffer (CCyB) and Systemic Risk Buffer (SRB), which help in addressing systemic risks. The Bank of England will also play a crucial role in revising these rules to fit within the FSMA framework, maintaining the UK's commitment to international standards while ensuring that buffers are aligned with domestic risks.

- Commencement regulations for revocation of capital-related CRR provisions: The third draft legislation focuses on the revocation of CRR provisions related to the definition of capital. This is particularly relevant to the PRA’s Strong and Simple regime, which is designed to simplify capital rules for smaller, domestic-focused financial institutions. The goal of the Strong and Simple framework is to reduce the regulatory burden for Small Domestic Deposit Takers (SDDTs), allowing them to compete more effectively without compromising financial stability. Under these regulations, provisions that define the quality and quantity of capital that firms must hold will be revoked, and new PRA rules will replace them to better reflect the risk profile of smaller institutions.

Implementation Timetable

HMT plans to initiate the CRR revocation process in stages, with the objective of aligning the revocation timeline with the PRA’s Basel III.1 implementation. The draft commencement regulations set forth a clear roadmap for phasing out the CRR and transitioning to UK-specific rules. 1 January 2026 has been set as the target date for full implementation of the Basel III.1 standards, giving both regulators and financial institutions adequate time to adapt to the new framework. This gradual, staged approach allows for the revocation of non-Basel-related aspects of the CRR and Capital Buffers and Macro-Prudential Requirements (CBR) provisions without disrupting the operational integrity of the financial system.

HMT recognizes that certain aspects of the CRR, particularly those that do not relate directly to Basel III.1, will require further commencement regulations. These forthcoming regulations will address additional capital-related provisions, ensuring that the UK's regulatory framework remains robust and adaptable to evolving financial risks.

Stakeholder Feedback and Consultation

To ensure the proposed legislative changes deliver the intended benefits, HMT and the PRA have opened a consultation process. This process invites feedback from stakeholders on the effectiveness of the draft legislation and its ability to provide regulatory clarity while enhancing prudential oversight. The consultation process is crucial to refining the regulatory framework to fit the unique needs of the UK’s financial system, while also ensuring it remains competitive on the international stage.

The proposed changes emphasize regulatory flexibility and responsiveness, which are key features of the FSMA model of regulation. By soliciting input from industry participants, HMT aims to ensure that the transition to this new framework is smooth and effective, delivering enhanced regulatory transparency, stability, and financial resilience.

Reduce your

compliance risks