CRR and CRD: Market Risk Management with FRTB

The EBA and ECB back the updated CRR and CRD, integrating FRTB to enhance market risk management, increase capital requirements, and strengthen the resilience of EU financial institutions

The Capital Requirements Regulation (CRR) and the Capital Requirements Directive (CRD) form the foundation of the European Union's regulatory framework for banks and financial institutions, ensuring financial stability and risk management. These regulations have undergone significant updates, effective as of September 2024, to enhance the EU banking sector's resilience to financial shocks. These updates, driven by legislative changes and recent delegated acts, focus on capital adequacy, risk management, liquidity, and supervisory practices, with the goal of safeguarding the banking system.

A key component of the updated CRR is the integration of the Fundamental Review of the Trading Book (FRTB), which introduces stricter methodologies for managing market risk. This framework transforms how banks measure and hold capital against risks in their trading books by implementing more conservative risk metrics and stricter rules on capital adequacy. This article explores the core elements of CRR, CRD, and FRTB, highlighting their impact on banks and the broader EU financial sector, while assessing the long-term implications of these reforms.

Source

[1]

CRR (Capital Requirements Regulation) and Market Risk

The Capital Requirements Regulation (CRR) is crucial for ensuring that banks hold sufficient capital to cover various risks, particularly market risk. Market risk encompasses potential losses from fluctuations in interest rates, stock prices, and exchange rates. Informed by the Basel III framework, CRR ensures that banks maintain robust capital buffers to mitigate these risks and enhance overall financial stability within the EU banking sector.

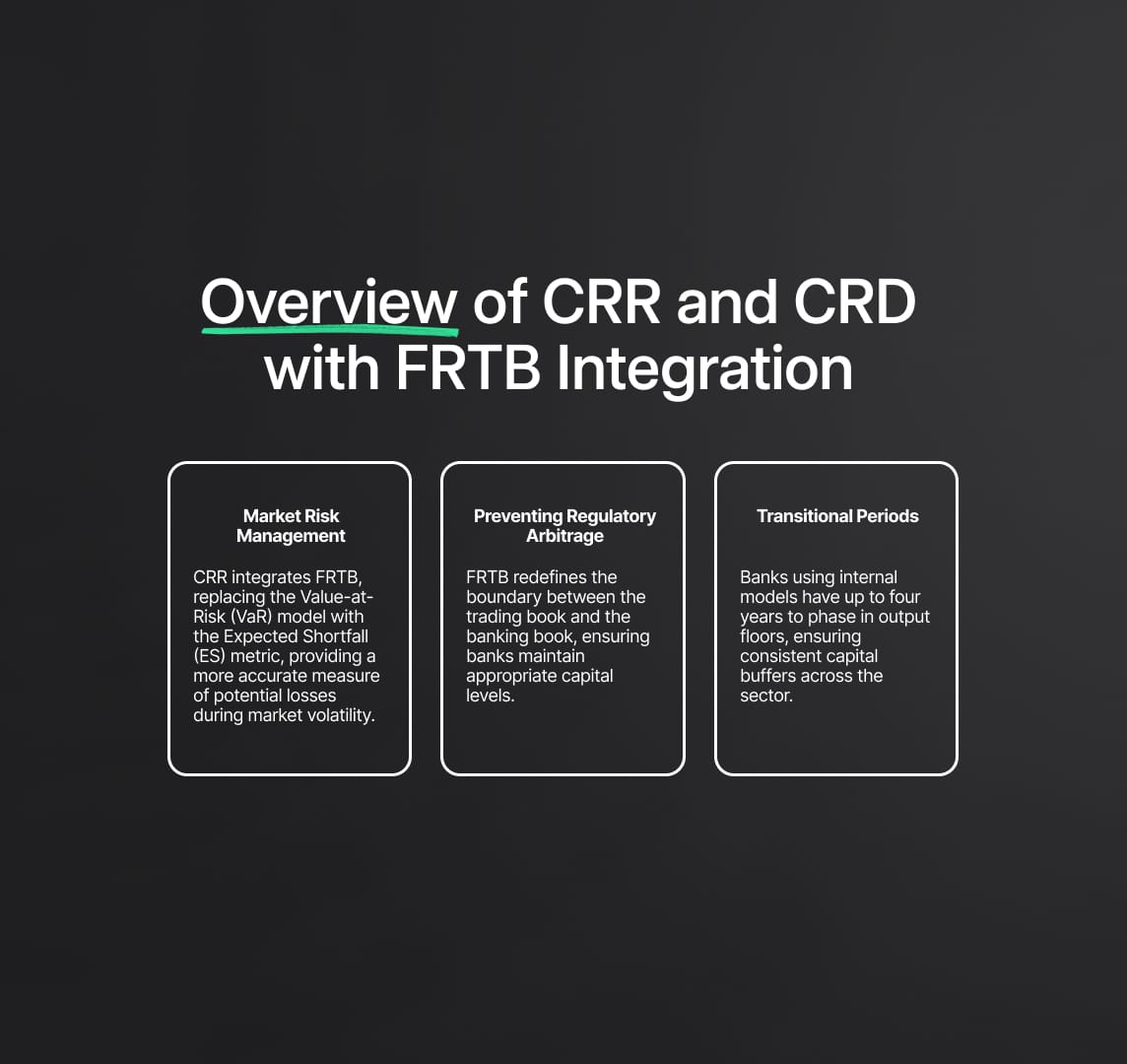

With the introduction of the Fundamental Review of the Trading Book (FRTB), CRR has undergone a significant transformation. FRTB replaces the traditional Value-at-Risk (VaR) model with the more conservative Expected Shortfall (ES) metric. The ES metric offers a more accurate measure of potential losses, especially during extreme market volatility, ensuring banks are better prepared for tail risks. This update in CRR emphasizes the EU’s commitment to preventing the underestimation of market risks, which could jeopardize financial stability.

Additionally, FRTB redefines the boundary between the trading book and the banking book to prevent regulatory arbitrage, where banks previously shifted assets between these categories to minimize capital requirements. By imposing stricter rules, the revised CRR framework ensures that banks maintain appropriate capital levels for all exposures, strengthening their ability to withstand market shocks.

Transitional Periods and Regulatory Adjustments in CRR

The Capital Requirements Regulation (CRR) includes transitional periods to help banks adjust to the new market risk management standards under FRTB. Banks using internal models for market risk calculation are granted up to four years to phase in output floors, which set minimum capital requirements based on standardized approaches. These output floors prevent banks from underestimating their risk-weighted assets (RWAs) and ensure consistent capital buffers across the sector.

Banks using the standardised approach for market risk calculation are not eligible for these transitional periods, reflecting CRR's focus on minimising discrepancies in risk models. This ensures that all banks, regardless of size or complexity, maintain adequate capital buffers, further reinforcing the resilience of the EU banking system.

Interaction Between CRR and CRD (Capital Requirements Directive)

While CRR provides quantitative rules on capital adequacy and market risk management, the Capital Requirements Directive (CRD) introduces qualitative supervisory and governance standards. CRD outlines the responsibilities of bank management boards, strengthens internal governance practices, and enhances risk management frameworks. These measures ensure that banks not only meet capital requirements but also implement strong internal controls to proactively manage risk.

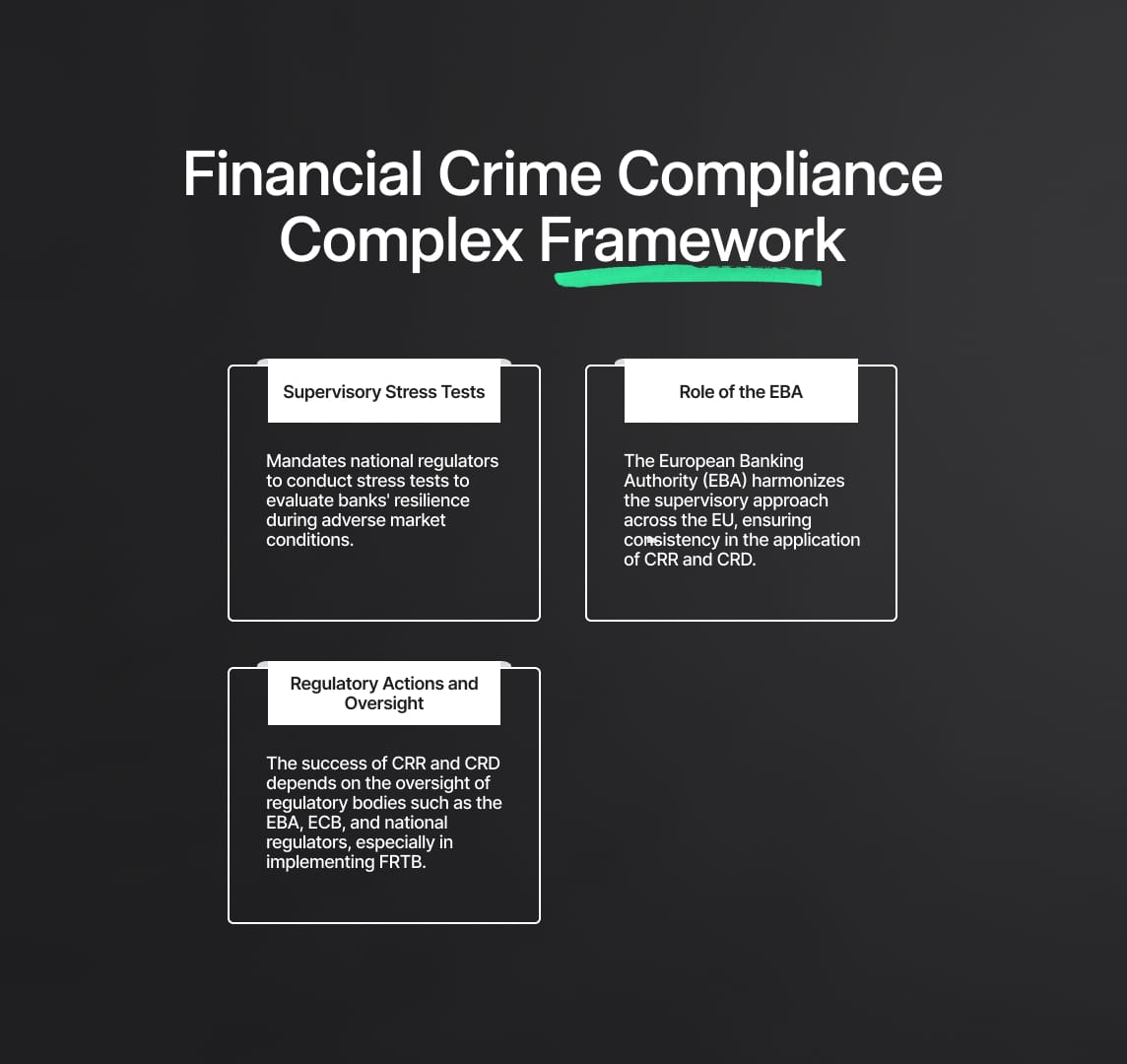

The CRD mandates that national regulators conduct supervisory stress tests to evaluate banks’ ability to maintain adequate capital during adverse market conditions. The European Banking Authority (EBA) plays a key role in harmonizing the supervisory approach across the EU, ensuring consistency in how CRR and CRD are applied. This alignment contributes to a more unified, stable financial system, enhancing the EU's ability to manage cross-border risks.

Regulatory Actions and Oversight under CRR and CRD

The success of the Capital Requirements Regulation (CRR) and Capital Requirements Directive (CRD) depends on the oversight of regulatory bodies such as the European Banking Authority (EBA), the European Central Bank (ECB), and national regulators under the Single Supervisory Mechanism (SSM). These institutions are responsible for ensuring that banks adhere to the updated standards, particularly the Fundamental Review of the Trading Book (FRTB), which introduces stricter capital requirements for market risk.

Postponement of FRTB Implementation

One of the most significant regulatory actions in the run-up to FRTB implementation has been the postponement of full adoption within the EU, as highlighted in the September 2024 updates. Due to technical challenges and concerns about banks’ readiness, the EBA issued no-action letters, extending the timeline for FRTB compliance. This extension provides banks with additional time to update their internal models and systems to meet the revised market risk capital framework under FRTB.

Despite the delay, regulators will closely monitor banks' progress. On-site inspections and reviews of risk management frameworks will increase, ensuring banks comply with the Expected Shortfall (ES) metric and follow the stricter trading book and banking book boundary rules. The success of FRTB's implementation will depend on banks’ ability to adapt to these higher standards.

Model Approval and Stress Testing

Regulatory oversight under CRR involves a rigorous model approval process for banks using internal models to calculate market risk. Banks must demonstrate that their models meet accuracy and reliability standards, or risk being required to adopt the standardized approach, which typically leads to higher capital requirements. This model validation process ensures that banks maintain appropriate capital levels to protect against severe market risks.

Additionally, stress testing will remain a key supervisory tool, allowing regulators to assess banks' resilience to extreme market conditions. These tests simulate adverse economic scenarios to determine whether banks hold sufficient capital to absorb potential losses. Banks found to be undercapitalized may face capital add-ons, requiring them to hold additional capital beyond the regulatory minimum.

Future Impact of CRR, CRD, and FRTB on the EU Banking Sector

The full implementation of FRTB within the CRR framework, combined with the supervisory standards of CRD, will significantly impact how banks allocate capital, manage risk, and generate profits.

Increased Capital Requirements

One of the most immediate effects of FRTB is the significant increase in capital requirements for banks engaged in trading activities. The shift from the Value-at-Risk (VaR) model to the Expected Shortfall (ES) metric will require banks to hold more capital to cover potential losses, especially in illiquid markets. This increase in capital will particularly affect banks with large trading books, as they will need to allocate more capital to mitigate risks.

Impact on Profitability and Business Models

The increased capital demands under FRTB will impact the profitability of banks, particularly in trading activities. As capital costs rise, banks may reduce exposure to high-risk markets or eliminate less profitable business lines. Many institutions may shift their focus toward client-driven activities and fee-based services, which require less capital and offer a more stable revenue stream under the updated CRR framework.

Market Liquidity and Structural Shifts

FRTB’s focus on liquidity horizons—adjusting capital requirements based on how long it takes to exit a position—may also affect market liquidity. By increasing capital requirements for less liquid positions, FRTB incentivizes banks to reduce their involvement in certain asset classes, potentially diminishing market depth. This shift could open opportunities for non-bank financial institutions such as hedge funds or asset managers to step in and provide market liquidity, though this may introduce additional systemic risks.

The integration of the Fundamental Review of the Trading Book (FRTB) into the Capital Requirements Regulation (CRR) and the enhanced supervision provided by the Capital Requirements Directive (CRD) mark a significant evolution in how banks manage market risk and allocate capital. These updates, effective as of September 2024, aim to strengthen financial stability across the EU by ensuring that banks maintain sufficient capital to absorb potential losses and manage risk effectively.

While these changes bring long-term benefits in terms of reduced systemic risk, they also pose challenges for banks, particularly regarding higher capital requirements and the need for more sophisticated internal models. As the full implementation of FRTB progresses, the EU banking sector will need to adapt, with implications for profitability, market structure, and liquidity. The role of regulatory authorities in overseeing these transitions will be critical to ensuring the stability and resilience of the financial system in the years to come.

Reduce your

compliance risks