ESRS to Corporate Sustainability Reporting Directive (CSRD)

Exploring the transformative impact of the EU Sustainability Reporting Standards (ESRS) and the Corporate Sustainability Reporting Directive (CSRD), the European Union's groundbreaking initiatives are setting global benchmarks for sustainability in business.

EU Adoption of ESRS Paves Path for Corporate Sustainability Reporting Directive (CSRD)

In the field of sustainability, the European Financial Reporting Advisory Group (EFRAG) has made a huge advancement. The legislative process for the ground-breaking EU Sustainability Reporting Standards (ESRS) has been concluded successfully. This accomplishment is extremely significant for the Corporate Sustainability Reporting Directive (CSRD) and is not only a cherry on top for EFRAG. The successful conclusion of the ESRS legislative procedure serves as a trigger, guaranteeing the seamless and punctual implementation of the CSRD throughout European businesses.

Many businesses are preparing their operational and reporting structures as 2024 draws nearer. This is in advance of them submitting their very first sustainability reports in compliance with the new requirement. Close collaboration between the accounting community and the corporate sector is ensuring that the shift to the CSRD framework is not only efficient but also seamless. Their shared goal is to transform the CSRD into a force for good in the actual world, not just a directive on paper.

But like with any big shift, there have been difficulties with the implementation of ESRS. Within the industry, there have been whispers regarding the complexity of ESRS. Concerns regarding the possible complications that could occur from aligning with these standards have been expressed by certain stakeholders. However, in spite of these concerns, the essential goal is still very much the same: to select sustainability disclosures that are not only pertinent in the current environment, but also uniform and comparable, guaranteeing openness and responsibility.

There is more to this project than merely reporting rules; it is propelled by the ESRS and the CSRD. It's a big step toward the objective of having an economy that is carbon neutral, something that the European Union and many other international organizations are working to achieve. It is anticipated that the emphasis on sustainability, accountability, and openness will encourage businesses to embrace more environmentally friendly practices, providing a better future for everybody.

Notable has been EFRAG's participation in this revolutionary journey. They have been advocating for high-quality sustainability reporting since September 2020. Their active involvement and direction have played a pivotal role in molding the ESRS and, consequently, the CSRD. They see this as a baseline for sustainability reporting requirements that might affect behaviors not just in the EU but worldwide, rather than merely a local accomplishment.

In summary, the completion of the ESRS legislative process and the approaching CSRD implementation are more than just legislative turning points. They stand for the dedication of the European Union to a sustainable future, in which EFRAG is a crucial component. The creation of a corporate landscape that is sustainable, transparent, and accountable continues to be the primary focus as firms, regulators, and stakeholders prepare for 2024.

Understanding the Impact of the EU Sustainability Reporting Standards (ESRS)

The European Union's financial environment is being affected by the transformative EU Sustainability Reporting Standards (ESRS) law. Stakeholders from all facets of the industry have been actively involved with its content from its launch, keenly analyzing its disruptive potential and possible repercussions.

The ESRS is a wake-up call to businesses, heralding the start of a new era of sustainability, rather than merely a collection of rules or regulations. The urgency of tackling environmental concerns—which are now real risks rather than just distant worries—reverberates throughout its form and meaning. The ESRS serves as a road map for companies, providing guidance on how to incorporate sustainable practices into their main operations and business plans. Nevertheless, the path to sustainability is complex, necessitating a comprehensive comprehension of the ESRS in order to fully realize its potential.

The deadline for firms to comply with the ESRS is drawing near—2024. However, what does this alignment actually mean? It goes beyond simply checking boxes related to compliance. Companies must absorb the ESRS's fundamental ideas and make sure that their operational, strategic, and financial choices are driven by a commitment to environmental sustainability if they are to fully adopt the standard. Businesses that make this kind of commitment will surely become more well-known and gain the trust of both stakeholders and customers. Additionally, by implementing the ESRS, companies may open up new opportunities for growth and innovation in addition to laying the groundwork for a sustainable future.

The Cornerstone of Corporate Sustainability Reporting Directive (CSRD)

The Corporate Sustainability Reporting Directive (CSRD) is a shining example of transparency in an era where knowledge is power. Acknowledging the significant influence that businesses have on the environment, the European Union enacted the Corporate Social Responsibility Directive (CSRD) to guarantee that corporations bear accountability for their actions and maintain transparency on them.

Fundamentally, the CSRD promotes sustainability reporting requirements. What does this signify for businesses? They must expose their activities to scrutiny by reporting their sustainability performance on a frequent and thorough basis. Such openness may have unintended consequences. On the one hand, it ensures that companies are continuously working toward more sustainable practices by holding them accountable. Conversely, it provides a chance for companies to demonstrate their dedication to sustainability and gain the confidence and support of a growing number of environmentally conscious customers.

The CSRD aims to change enterprises' basic essence rather than just guaranteeing compliance. As the world struggles with the effects of unrestrained environmental degradation, the CSRD provides a way ahead, pointing companies in the direction of a successful and sustainable future. It establishes a precedent that sustainability and profitability can coexist and are not exclusive.

But creating such a synergy takes work. Companies need to be aware of the CSRD's nuances in order to properly report their sustainability performance. This requires arming them with the necessary resources, expertise, and reporting techniques. This entails knowing both the letter and the spirit of the law. The European Union's dedication to building a more sustainable and environmentally friendly future is demonstrated by the CSRD, which places a strong focus on transparency. Companies can take the lead in promoting a new era of environmental stewardship and business responsibility by aligning with this direction.

Transparency and Accountability: The Twin Pillars of ESRS and CSRD

Transparency and accountability are more important than ever at a time when information spreads quickly. These two principles are now embodied in the ESRS and the Corporate Sustainability Reporting Directive (CSRD), which serve as beacons of hope amidst the enormous expanse of corporate governance.

With the introduction of the ESRS and CSRD, transparency has become more than just a catchphrase. It stands for a business's dedication to transparency regarding its sustainability activities, enabling investors, stakeholders, and the general public to see through its strategies, actions, and decision-making procedures. Collaboration towards a sustainable future is facilitated by such openness, which builds trust and stimulates communication between businesses and their stakeholders.

Transparency, on the other hand, is enhanced by accountability. Companies are held accountable for their activities and pledges as well as encouraged to be open with the introduction of ESRS and the CSRD directives. Their responsibility is to demonstrate sincere efforts towards sustainability, making sure that their reports are more than just paperwork but rather a true account of what they have done.

Adopting accountability and openness, nevertheless, is not without its difficulties. Companies may come under more scrutiny when pursuing these ideals, which raises questions about possible reputational implications. Overall though, the advantages outweigh the disadvantages. In this day and age, it is crucial for a firm to cultivate loyalty among stakeholders and customers by being honest and accountable.

Companies who incorporate these two pillars into their corporate culture not only follow the ESRS and CSRD but also carve out a place for themselves in a market that is becoming more and more competitive and environmentally concerned.

European Financial Reporting Advisory Group (EFRAG): Championing the Cause of ESRS and CSRD

An essential part in the story of the ESRS and the Corporate Sustainability Reporting Directive (CSRD) is played by the European Financial Reporting Advisory Group (EFRAG). EFRAG has played a pivotal role in defining the evolution of these guidelines since their origin and ensuring their effective implementation.

EFRAG has been leading the way in promoting high-quality sustainability reporting and helping businesses navigate the intricacies of ESRS and CSRD. For many businesses, their knowledge and involvement have served as a guide through the difficult seas of sustainable reporting. EFRAG has been steadfast in its objective to guarantee that the ESRS and CSRD aren't merely theoretical constructs but rather practical frameworks through seminars, webinars, and stakeholder engagements.

Their commitment goes beyond simply supporting businesses. The ESRS and CSRD are always being improved and refined by EFRAG to make sure they are still applicable and useful in the ever-changing corporate environment. Their emphasis on industry-specific standards and their latest move to create a Q&A forum demonstrate how dedicated they are to developing a comprehensive, inclusive, and dynamic sustainability reporting system.

EFRAG's function essentially goes beyond regular regulatory oversight. They have become collaborators, instructors, and trailblazers, pushing the envelope in sustainability reporting and making sure that the ESRS and CSRD continue to be the industry standard not just in the EU but throughout the world.

Looking Forward: The Future of Sustainability Reporting with ESRS and CSRD

The EU Sustainability Reporting Standards (ESRS) and the Corporate Sustainability Reporting Directive (CSRD) are leading the charge in the change of the corporate sustainability landscape. These frameworks are defining a future in which sustainability, responsibility, and transparency become the cornerstones of corporate operations in addition to influencing the present.

The combination of ESRS and CSRD offers companies a clear route that combines environmental considerations with financial success. Companies of all sizes and in all industries are preparing to fully implement these directives as 2024 draws near. This alignment represents a change in corporate thinking, where companies now see sustainability as an essential component of their strategy plan rather than just an optional endeavor. It goes beyond simply following legislation.

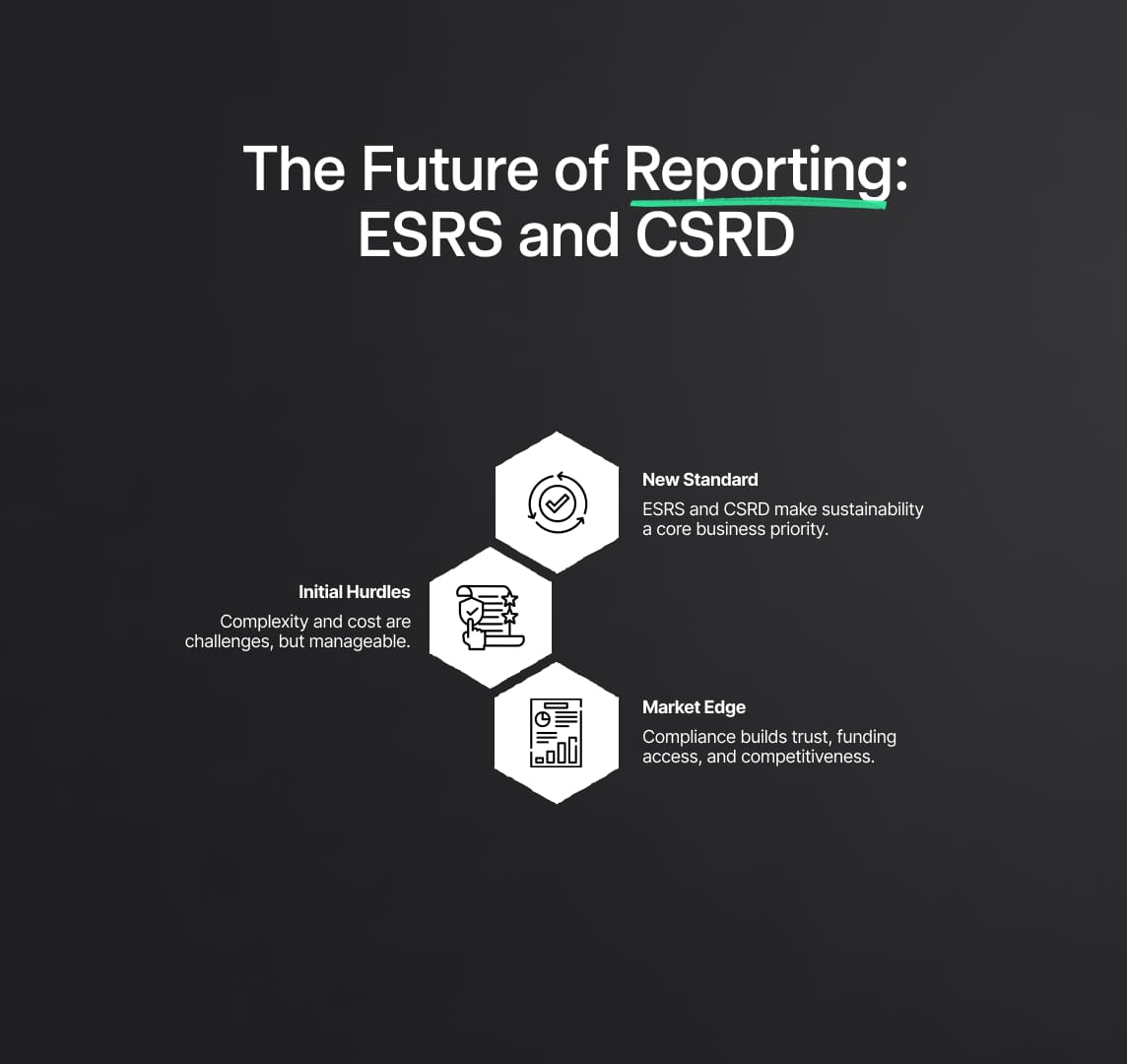

However, there are obstacles in the way. The complexity of ESRS and CSRD can be intimidating, particularly for businesses that are only starting out on their sustainability journey. Concerns over the expense of alignment, the requirement for specialist knowledge, and the possible necessity for operational redesigns are prominent. However, when seen in a larger context, these difficulties are overcomeable. Is it financially feasible for firms to deviate from ESRS and CSRD compliance?

The world economy is undergoing a paradigm change. Customers, stakeholders, and investors are looking for businesses that are not only providing high-quality goods and services but are also ecologically mindful as they become more environmentally concerned. This change may be seen in the way people invest, as sustainable financing is becoming more popular. Businesses who support ESRS and CSRD will profit from this trend by having access to funding that values and rewards sustainability.

Additionally, CSRD and ESRS give companies a competitive edge. The strict guidelines established by ESRS and the guidelines of CSRD enable businesses to stand out in a market crowded with sustainability claims by demonstrating their sincere dedication to a greener future.

In conclusion, ESRS and CSRD will continue to change sustainability reporting in a positive way. Even if the path may be difficult, there are substantial material and intangible benefits. The objective for this future is clear: a corporate environment that is profitable but also sustainable, transparent, and accountable as companies, regulators, and stakeholders work together. By implementing ESRS and CSRD, the European Union is not only establishing a global standard but also encouraging businesses all over the world to join the fight for a sustainable future.

Reduce your

compliance risks