EU Enhancements to the Retail Investment Package

The Retail Investment Package in June 2024 changes EU financial regulations by enhancing Key Information Documents (KIDs) for PRIPs. The package ensures market integrity, investor protection, and aligns with the Capital Markets Union goals.

In June 2024, the European Union unveiled pivotal reforms with the introduction of the Retail Investment Package, aimed at profoundly transforming the financial regulatory landscape. These enhancements, complemented by targeted amendments to Regulation (EU) No 1286/2014, focus on optimizing the Key Information Document (KID) for packaged retail investment products (PRIPs). This sweeping initiative is strategically designed to bolster market integrity, fortify investor protections, and assure the delivery of genuine value for money across retail investment offerings, perfectly aligning with the ambitious objectives of the European Capital Markets Union (CMU).

Detailed Overview of the Retail Investment Package Reforms

The Retail Investment Package introduces a series of comprehensive reforms that address multiple facets of the financial services sector, reflecting a deep commitment to enhancing transparency and trust in the European financial markets. These reforms are meticulously crafted to close gaps in the current regulatory framework, thereby strengthening the safeguards that protect retail investors.

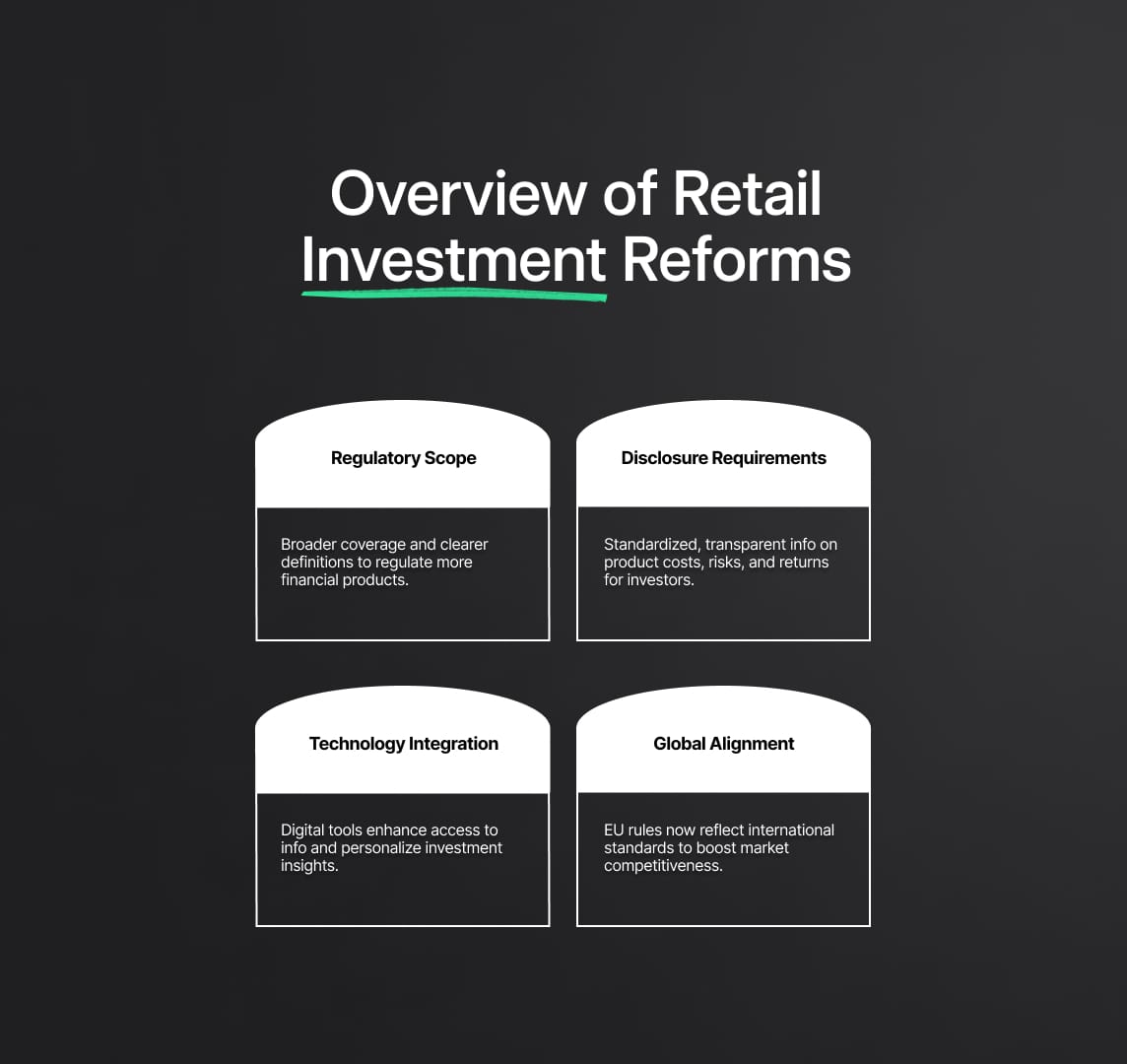

1. Expansion and Clarification of Regulatory Scope

The reforms broaden the scope of existing regulations to encompass a wider array of financial instruments and investment services. This expansion ensures that emerging financial products and evolving investment strategies are adequately regulated, maintaining a level playing field for all market participants. Furthermore, the package provides much-needed clarifications regarding the definitions and classifications used in the regulatory framework, which streamline compliance requirements and reduce ambiguities that could lead to exploitation.

2. Enhanced Disclosure Requirements

Central to the Retail Investment Package is the enhancement of disclosure requirements for financial products. These enhancements mandate that all investment products covered under the EU regulations provide detailed, easily understandable information about their costs, risk factors, and expected returns. The aim is to empower investors to make more informed decisions by providing them with comprehensive data in a standardised format.

3. Integration of Technological Advances

Recognizing the role of technology in modern finance, the package integrates digital tools to improve how information is delivered to investors. This includes the adoption of digital platforms for the dissemination of regulatory documents and the use of advanced analytics to provide personalised investment insights based on the individual’s risk tolerance and financial goals.

4. Adoption of Best Practices and International Standards

The reforms align the EU’s regulatory standards with international best practices, enhancing the global competitiveness of EU financial markets. By adopting standards that are recognized globally, the EU ensures that its financial markets remain attractive to international investors while safeguarding the interests of European investors.

Impact on Market Integrity and Investor Confidence

By addressing these critical areas, the Retail Investment Package significantly enhances the structural integrity of the EU's financial markets. The reforms are designed not only to protect investors but also to foster a transparent, fair, and stable investment environment. Enhanced regulatory clarity and improved investor protections help in rebuilding trust among investors, which is crucial for the stability and growth of the capital markets. Furthermore, the emphasis on value for money and comprehensive disclosure supports the CMU’s goal of increasing investment flows across the union, thereby fueling economic growth and innovation.

In summary, the Retail Investment Package marks a significant milestone in the EU’s efforts to refine its financial regulatory framework, ensuring that it remains robust, transparent, and responsive to the needs of modern investors. This initiative not only strengthens market integrity but also enhances the overall investment landscape, paving the way for a more secure and prosperous financial future for all EU citizens.

Regulatory Reforms and Enhancements to Investor Protections in the EU Retail Investment Package

In June 2024, the European Union introduced the Retail Investment Package, a transformative legislative framework designed to elevate standards across the financial sector. This package involves critical amendments to key directives such as UCITS (Undertakings for Collective Investment in Transferable Securities), MiFID II (Markets in Financial Instruments Directive), and Solvency II, which collectively enhance the regulation of investment services provided to retail clients. These reforms are strategically aligned with the EU's commitment to tightening financial regulations, ensuring transparency, and protecting investors from potential conflicts of interest, especially those related to the management and disclosure of inducements.

Detailed Breakdown of Directive-Specific Amendments

UCITS Enhancements

The amendments under the Retail Investment Package introduce stricter operational requirements for UCITS funds, focusing on improving their management and marketing within the EU. New regulations mandate enhanced disclosure of fund objectives, investment strategies, and associated risks, thereby providing retail investors with clear, comprehensive information that supports informed decision-making. Additionally, the reforms include stipulations for increased frequency and detail in reporting, aimed at fostering greater transparency regarding fund performance and management.

MiFID II Modifications

Under MiFID II, the Retail Investment Package significantly tightens the rules concerning the provision of investment advice and product recommendations to retail investors. These modifications include stricter criteria for assessing the suitability and appropriateness of financial products for each individual investor, ensuring that products offered align with the investor's financial situation, investment experience, and risk tolerance. Moreover, the package enforces more rigorous controls on inducements, such as commissions and fees, that advisers and brokers can receive, requiring that such inducements be clearly disclosed and justified as enhancing the quality of the service to the client.

Solvency II Adjustments

For insurance products covered under Solvency II, the Retail Investment Package enhances the regulations surrounding product oversight and governance. These adjustments require insurance firms to conduct thorough assessments of their investment products to ensure they meet the needs of targeted consumers, including detailed evaluations of risk profiles and cost structures. Furthermore, the reforms demand greater transparency in the pricing and provision of insurance-based investment products, facilitating better understanding and comparison for consumers.

Addressing Conflicts of Interest Through Inducement Management

A significant aspect of the Retail Investment Package is its focus on managing conflicts of interest, particularly through the lens of inducement management. The package stipulates that all inducements must be designed to enhance the quality of the service to the client and not detract from the duty of the financial adviser or firm to act in the best interests of the client. This involves explicit disclosure requirements, ensuring that clients are fully aware of any inducements that may influence the advice they receive. By tightening these regulations, the EU aims to prevent the misalignment of financial adviser incentives with client interests, thereby bolstering the integrity and trustworthiness of financial advisement within the EU markets.

Inducement Transparency and Implementing Value for Money Assessments in the Retail Investment Package

The European Union's Retail Investment Package represents a critical enhancement to the regulatory landscape, specifically targeting the transparency of inducements and the implementation of comprehensive "value for money" assessments. This section of the package is designed to refine the accountability mechanisms within the financial services industry, ensuring that all financial inducements are transparently disclosed and that the costs associated with financial products and services are proportionate to the benefits they deliver to consumers.

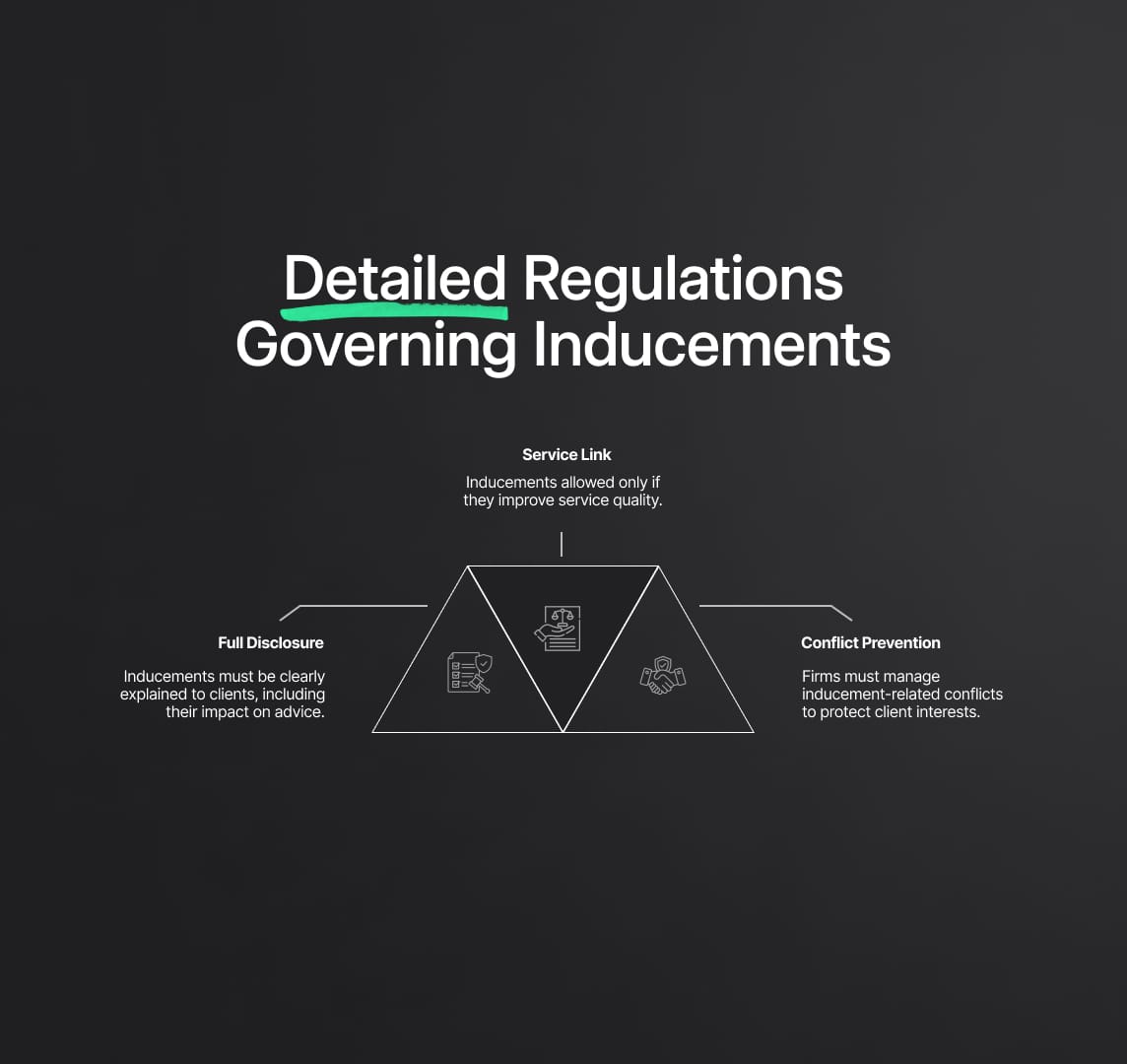

Detailed Regulations Governing Inducements

Under the new Retail Investment Package, the EU has introduced more stringent regulations governing the transparency of inducements—payments or rewards offered by service providers to influencers or decision-makers within the investment process. These inducements can range from commissions given to brokers to fees paid to financial advisors for recommending certain products. The updated regulations mandate:

- Full Disclosure: All financial inducements must be fully disclosed to clients in a clear, understandable manner, detailing how they might influence the recommended investment decisions.

- Link to Service Quality: Inducements must be linked directly to an enhancement in the quality of service provided to the client, and not merely to the volume of transactions or the product sold.

- Preventive Measures Against Conflicts of Interest: The package requires that firms put in place robust mechanisms to manage and mitigate any potential conflicts of interest that inducements could create, ensuring that the client’s best interests always take precedence.

These provisions are aimed at increasing transparency and trust in financial advisement, thereby safeguarding the market against practices that could undermine the integrity of financial advice and decision-making.

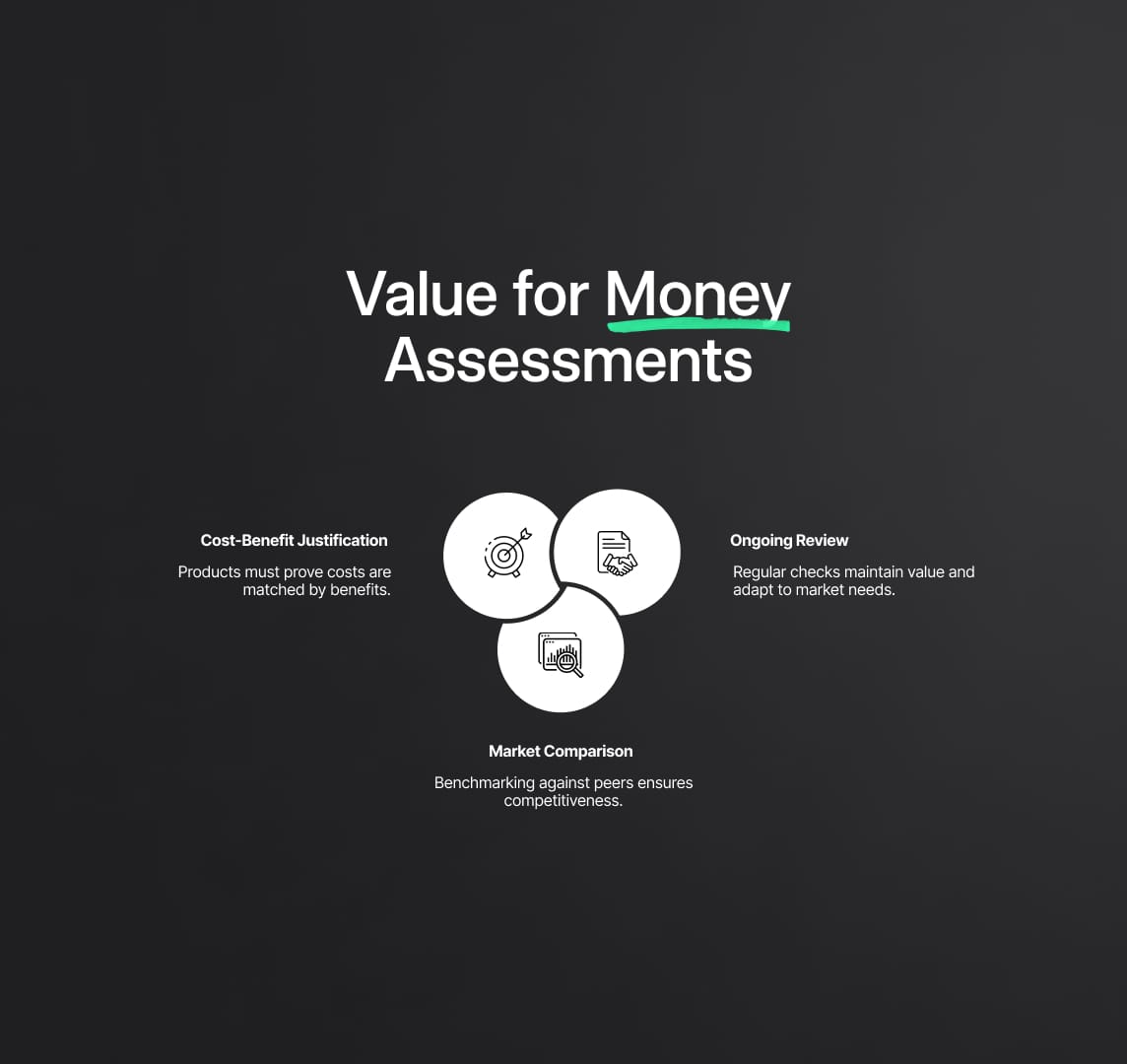

Value for Money Assessments

Another cornerstone of the Retail Investment Package is the implementation of "value for money" assessments. This initiative compels manufacturers and distributors of financial products to justify the costs and charges associated with their products, ensuring they are proportionate to the benefits provided. This assessment involves several key elements:

- Cost-Benefit Analysis: Financial products must undergo a thorough analysis to demonstrate that their costs are justified by the level of performance and the benefits they offer to the investor.

- Comparative Benchmarks: Products must be compared against similar offerings in the market to ascertain competitiveness and value alignment. This comparison helps in highlighting any discrepancies in pricing and benefits, pushing for more competitive pricing structures.

- Regular Reviews: Financial products are subject to periodic reviews to ensure ongoing compliance with value for money criteria. These reviews help adapt pricing and product features in response to market changes and consumer feedback, ensuring that products remain beneficial to consumers over time.

Implications for the Financial Market

By mandating enhanced transparency in inducements and rigorous value for money assessments, the Retail Investment Package aims to protect investors from potentially exploitative fees and to enhance the overall competitiveness of financial products in the market. These reforms are expected to lead to a more equitable financial market where investment decisions are made with greater confidence and where financial products are more closely aligned with the needs and expectations of investors.

The emphasis on clear, justified, and client-oriented financial service practices within the Retail Investment Package not only enhances consumer protection but also promotes a healthier, more competitive market environment. This initiative is a pivotal step in advancing the EU's commitment to fostering transparent and fair financial markets, enhancing investor trust, and contributing significantly to the stability and growth of the capital markets union.

Development of Supervisory Benchmarks and Strengthening Product Governance

Under the recently introduced Retail Investment Package, the European Securities and Markets Authority (ESMA) and the European Insurance and Occupational Pensions Authority (EIOPA) play pivotal roles in enhancing the integrity and transparency of financial markets across the European Union. This initiative, central to the Retail Investment Package, aims to establish a standardized yet adaptable framework for supervising and assessing the value offered by investment products.

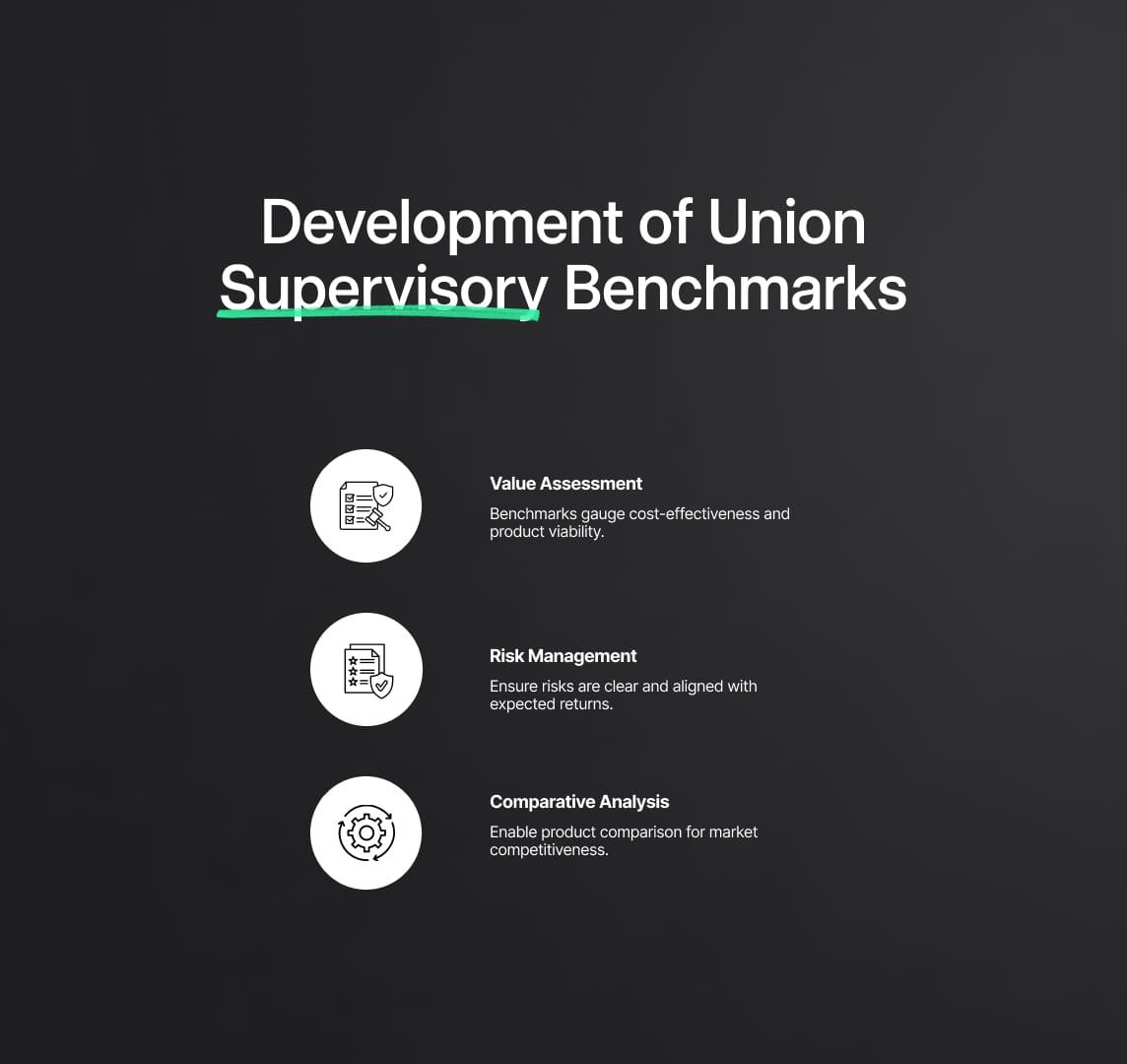

Development of Union Supervisory Benchmarks

The Retail Investment Package introduces a new system of Union supervisory benchmarks developed by ESMA and EIOPA. These benchmarks are designed as flexible supervisory tools rather than fixed requirements, providing a scalable solution that adapts to the evolving market conditions and product innovations. The benchmarks focus on several critical aspects:

- Value Assessment: These benchmarks help in assessing whether investment products provide adequate value for the money spent by consumers, scrutinizing factors such as cost-effectiveness, performance against market standards, and overall financial product viability.

- Risk Management: Supervisory benchmarks include parameters for evaluating the risk associated with different investment products, ensuring that these risks are transparently communicated to potential investors and align with the expected returns.

- Comparative Analysis: They facilitate a comparative analysis of similar products in the market, providing both regulators and consumers with clear insights into where a particular product stands in terms of market competitiveness and consumer value.

These benchmarks serve not only to guide the product manufacturers in enhancing their offerings but also assist national competent authorities in monitoring and ensuring that these financial products meet the stipulated standards of quality and transparency.

Strengthening Product Governance

The Retail Investment Package mandates that financial product manufacturers engage in rigorous market comparisons as part of their product approval process. This initiative is designed to foster a competitive market environment that inherently pushes for high-quality investment products. Key elements of this strengthened product governance include:

- Market Comparisons: Manufacturers are required to conduct detailed comparisons of their products against similar offerings in the market. This ensures that each product is competitively priced and offers value that is on par with or superior to existing alternatives.

- Continuous Assessment: Continuous assessment of products post-launch is encouraged to ensure ongoing compliance with market standards and regulatory expectations. This aspect of governance helps in dynamically adjusting product features or pricing to better meet consumer needs.

- Flexibility for Member States: Recognizing the diverse economic landscapes across the EU, the package provides flexibility for member states to tailor the implementation of these benchmarks. States can choose to utilize Union supervisory benchmarks or develop their own criteria that better suit their specific market conditions, thus ensuring that local markets are optimally regulated while still aligning with broader EU objectives.

The introduction of supervisory benchmarks and the emphasis on stringent product governance under the Retail Investment Package are set to significantly impact the financial industry. By standardizing the evaluation criteria for financial products and enhancing the transparency of product offerings, these measures are expected to lead to increased investor trust and participation in the financial markets.

Moreover, this approach encourages manufacturers to innovate and improve their products continuously, fostering an environment where quality and value are paramount. The flexibility offered to member states also ensures that these benefits are adapted to local contexts, maximising their effectiveness across diverse European markets.

The strategic enhancements in supervisory benchmarks and product governance are vital components of the Retail Investment Package, ensuring that the EU's financial markets remain robust, competitive, and transparent. These reforms not only protect investors but also promote a healthier market environment conducive to sustainable economic growth.

Key Information Document in the Retail Investment Package

In a significant update to Regulation (EU) No 1286/2014, the European Union has introduced comprehensive enhancements to the Key Information Document (KID) as part of its broader Retail Investment Package. These enhancements are strategically designed to increase the clarity and accessibility of KIDs, making it easier for retail investors to understand and compare the key attributes of investment products. This initiative underscores the EU's commitment to strengthening consumer protections and increasing transparency in the financial sector.

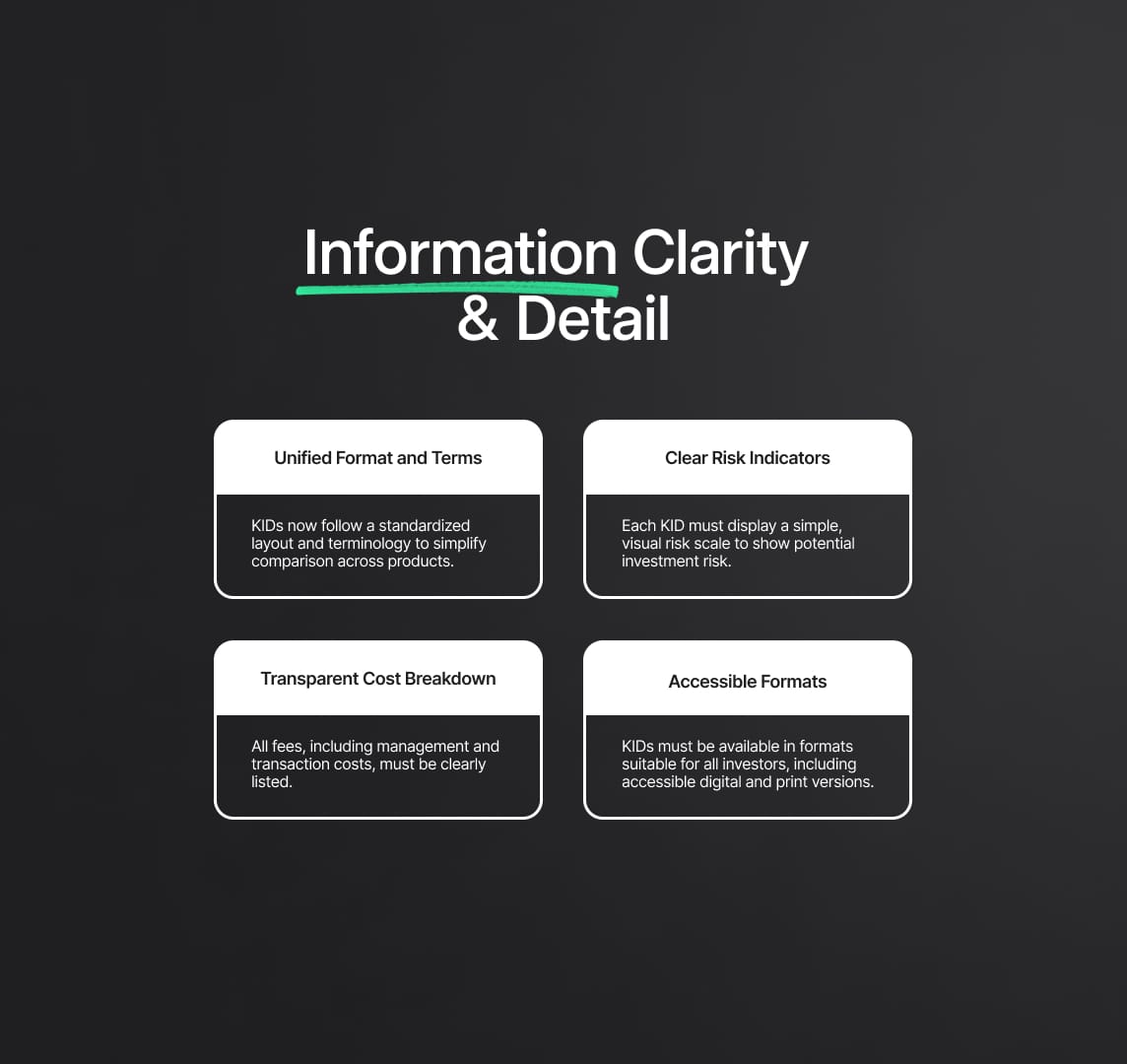

Clarity and Detail in Information Presentation

The amendments to the KID focus on several key areas to improve the document's effectiveness in communicating essential information to investors:

- Standardization of Layout and Terminology: The EU has introduced a standardized format and consistent terminology for all KIDs. This uniformity helps investors easily locate and comprehend critical information, such as risks, costs, and expected returns, across different investment products.

- Inclusion of Clear Risk Indicators: Each KID now must include a clear, easily understandable risk indicator, typically presented as a numerical scale or color-coded system. This indicator provides investors with an immediate visual representation of the potential risk associated with the investment product.

- Enhanced Description of Costs: The amendments require that all costs associated with an investment product, including management fees, performance fees, and transaction costs, be clearly outlined in the KID. This breakdown ensures that investors are fully aware of any charges that may impact their investment returns.

- Improved Accessibility: To accommodate a broader range of investors, including those with disabilities, KIDs are required to be available in multiple formats. This includes larger print versions, easy-to-read formats, and the possibility of digital versions that are compatible with screen readers.

Integration of Advanced Digital Tools

Recognising the increasing role of digital technology in financial services, the Retail Investment Package mandates the integration of advanced digital tools to enhance the functionality of KIDs:

- Interactive Features: Digital versions of KIDs can include interactive elements, such as calculators or clickable sections, allowing investors to customize the information based on their specific circumstances and investment goals.

- Real-time Updates: Digital KIDs are designed to offer real-time updates on product details, reflecting any changes in market conditions or product features promptly. This ensures that investors always have access to the most current information.

- Integration with Other Digital Financial Tools: KIDs are increasingly integrated into broader digital financial platforms. This integration allows investors to view their KID alongside other financial documents and tools, facilitating a more holistic approach to managing their investments.

Compliance and Monitoring

To support these enhancements, the EU has also set forth strict compliance and monitoring frameworks to ensure that all financial institutions adhere to the new KID standards. Regular audits and reviews are mandated, with significant penalties for non-compliance to reinforce the importance of accurate and transparent information disclosure.

Definitions and Digital Innovations in the Retail Investment Package

As part of the comprehensive Retail Investment Package, the European Union has implemented crucial amendments to Regulation (EU) No 1286/2014, focusing on the Packaged Retail and Insurance-based Investment Products (PRIPs). These amendments serve a dual purpose: refining the definition of PRIPs and leveraging modern technology to enhance transparency for investors, thereby aligning with the EU's commitment to improve the investment landscape.

Clarification and Expansion of PRIPs Definition

The recent amendments provide essential clarification on what constitutes a PRIP, ensuring a more inclusive and precise understanding. This clarification addresses the complexities of modern financial products and their risk profiles by defining PRIPs more broadly to cover any investment where the amount repayable to the investor is subject to fluctuation due to market performance. This includes instances where such fluctuations are not solely related to make-whole clauses, which are contractual provisions that compensate investors if a security is terminated before maturity.

This enhanced definition helps investors better understand the risks associated with different financial products and aligns product offerings with investor expectations and market realities. By delineating clear boundaries and characteristics of PRIPs, the Retail Investment Package aims to safeguard investors from unexpected financial exposures and align investment products more closely with regulatory standards.

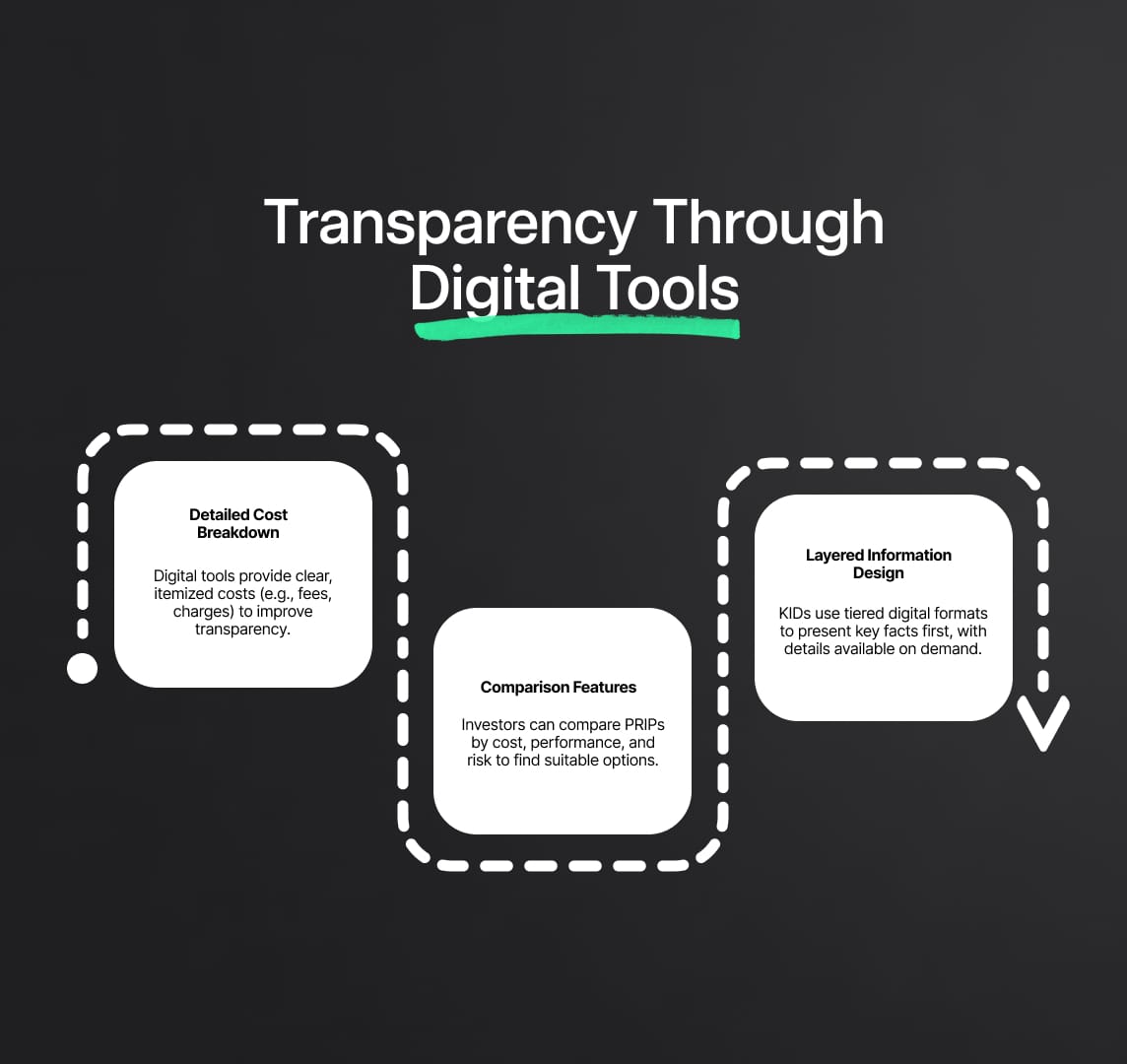

Transparency Through Digital Tools

Recognising the challenges posed by the diverse and complex nature of modern investment products, especially those offering multiple investment options, the amendments significantly advocate the use of advanced digital tools. These tools are designed to:

- Enhance Cost Transparency: Digital platforms now enable investors to access detailed breakdowns of all costs associated with PRIPs. This includes management fees, advisory fees, transaction costs, and any other charges that might impact the investment's overall profitability. By providing these details in an easily accessible digital format, investors can make more informed decisions based on comprehensive cost analyses.

- Facilitate Effective Comparisons: Through integrated comparison tools, investors can evaluate different PRIPs side-by-side, assessing not only the costs but also performance metrics and risk factors. This capability is crucial in empowering investors to choose products that best fit their investment goals and risk tolerance.

- Support Layered Information Presentation: To counteract information overload—a common issue with complex investment documents—the amendments promote a layered approach to the presentation of the Key Information Document (KID). This approach structures information into tiers, starting with the most critical insights at the top layer, followed by more detailed data accessible through further interaction. Such a structured digital presentation helps in distilling vast amounts of data into digestible and actionable information.

Sustainability and Timely Updates in the Retail Investment Package

As part of the ongoing enhancements within the Retail Investment Package, significant strides have been made to incorporate Environmental, Social, and Governance (ESG) criteria into investment decisions and to standardize information presentation through regulatory technical standards. These steps underscore the European Union's commitment to sustainability and consumer protection, ensuring that investment products align with broader social and environmental goals while maintaining transparency and relevance over time.

Inclusion of Sustainability Information in Key Information Documents (KIDs)

The latest amendments to the Retail Investment Package mandate the inclusion of detailed sustainability profiles in the Key Information Documents (KIDs) for Packaged Retail and Insurance-based Investment Products (PRIPs). This requirement aims to reflect the growing investor interest in sustainable and responsible investing by providing clear, actionable insights into the ESG performance of investment products. Here's how sustainability integration is being enhanced:

- Comprehensive ESG Disclosures: KIDs now must feature a section dedicated to explaining how PRIPs align with ESG criteria. This includes information on how investment funds are used to support environmental sustainability, social responsibility, and governance practices.

- Leveraging Existing EU Regulations: To streamline reporting processes and minimize the burden on financial institutions, the sustainability information required in KIDs draws from existing disclosures mandated by EU regulations such as the Sustainable Finance Disclosure Regulation (SFDR). This ensures consistency across documents and reduces redundancy in reporting.

- Transparency and Investor Confidence: By integrating ESG factors into KIDs, investors are empowered to make decisions that align with their values, enhancing trust and satisfaction with financial products offered within the EU.

Ongoing Updates for Accuracy and Relevance

To maintain the accuracy and relevance of the information provided in KIDs, the Retail Investment Package establishes protocols for regular updates:

- Dynamic Updating Process: KIDs must be periodically reviewed and updated, especially when new subscriptions are opened or products become available on secondary markets. This ensures that the information remains current and reflects any changes in market conditions or product characteristics.

- Real-time Information Availability: Updates to KIDs are required to be made available in real-time, ensuring that investors have access to the most current data before making any investment decisions.

Development of Regulatory Technical Standards by ESAs

The European Supervisory Authorities (ESAs) play a crucial role in enhancing the effectiveness of KIDs through the development of regulatory technical standards. These standards are focused on:

- Standardization of Presentation: The ESAs are tasked with creating uniform guidelines for presenting information in KIDs, including details on costs, performance risks, and sustainability factors. This standardization is critical for ensuring that all relevant information is easy to understand and compare across different investment products.

- Enhanced Comparability: By standardizing how information is presented, investors can more easily compare different PRIPs, leading to better-informed investment choices and fostering a competitive market environment.

- Adaptation to Market Developments: The regulatory technical standards are designed to be adaptable, allowing for updates and modifications as market conditions evolve and new investment trends emerge.

The inclusion of sustainability information and the ongoing updates to KIDs, coupled with the development of regulatory technical standards, are significant enhancements brought forth by the Retail Investment Package. These initiatives not only align with the EU's commitment to sustainable development but also ensure that retail investment products remain transparent, up-to-date, and aligned with investor needs and market trends. By embedding these practices into the regulatory framework, the Retail Investment Package promotes a more informed, conscious, and dynamic investment environment across the European Union.

Reduce your

compliance risks