IFRS Accounting Standards for SME

The December 2023 IFRS for SMEs Accounting Standard Update presents crucial advancements in financial reporting. Focusing on SMEs, it details significant changes within the IFRS framework, aimed at improving transparency and ensuring alignment with global IFRS Accounting Standards.

The Global Standard for Financial Reporting

In today's interconnected global economy, a universal language for financial reporting is not just beneficial, it's essential. International Financial Reporting Standards (IFRS), issued by the influential International Accounting Standards Board (IASB), serve as this common framework. The primary goal of IFRS is to ensure the consistent application of accounting principles worldwide. This consistency significantly enhances the comparability of financial data across different countries, leading to more efficient capital allocation and accurate asset pricing on a global scale.

Disparate national accounting standards can often obscure a company's true financial health, creating challenges for investors, lenders, and other stakeholders. By establishing a unified set of rules, IFRS Accounting Standards bring unparalleled transparency and quality to financial information, empowering market participants to make sound, informed economic decisions.

Commitment to Small and Medium-Sized Entities (SMEs)

The IFRS Foundation, the parent organization of the IASB, is dedicated to developing standards that also cater to the unique needs of small and medium-sized entities (SMEs). This focus acknowledges the vital role SMEs play in the global economy and highlights the broad applicability of IFRS beyond large, multinational corporations.

Core Objectives and Key Benefits of Global Accounting Harmonization

The central mission of IFRS is to establish a single set of high-quality, understandable, and enforceable accounting standards that are accepted worldwide. This harmonization is critical for investors who rely on comparable financial data to evaluate investment opportunities across international markets. When companies use different accounting rules, it can be difficult to draw meaningful comparisons between them.

The adoption of a single global standard provides distinct advantages for various stakeholders:

- For Investors and Lenders: IFRS increases transparency and reduces investment risk by simplifying the process of comparing companies in different jurisdictions.

- For International Companies: A unified standard can lead to a lower cost of capital, streamlined consolidation of financial statements for multinational groups, and easier access to global capital markets.

- For Small and Medium-Sized Entities (SMEs): Adopting a framework like the IFRS for SMEs® Accounting Standard enhances credibility with international partners, including customers, suppliers, and investors, thereby fostering greater cross-border trade and investment.

Ultimately, this global harmonization builds greater trust and stability within the international financial system by promoting high-quality, comparable financial reporting. The continued development and adoption of IFRS, including standards tailored for SMEs, represent a powerful and sustained movement toward global accounting convergence.

The IFRS for SMEs Accounting Standard: A Tailored Framework

Recognizing that the full scope of IFRS may be overly complex for non-publicly accountable entities, the IASB developed the IFRS for SMEs® Accounting Standard. This is a self-contained and globally recognized set of principles designed specifically for businesses that do not have public accountability but still produce general-purpose financial statements for external users, such as non-managing owners, creditors, and credit rating agencies.

The IFRS for SMEs standard is a simplified version of the full IFRS, modified to meet the specific needs of its users while considering the cost-benefit balance for preparers. Key simplifications include:

- Omitting topics not relevant to SMEs.

- Providing fewer accounting policy choices.

- Simplifying many recognition and measurement principles.

- Requiring significantly fewer disclosures.

- Using clear, easily translatable language.

The standard's global success is demonstrated by its widespread adoption. It provides a proportionate, effective, and internationally respected reporting framework for the vast majority of companies worldwide.

The Evolution of IFRS for SMEs: Journey to the Third Edition

The IFRS for SMEs® Accounting Standard is a dynamic framework that undergoes periodic reviews. This ensures it remains relevant, aligns with developments in full IFRS Accounting Standards, and continues to meet the specific needs of small and medium-sized entities.

The December 2023 Update: A Prelude to Major Revisions

In December 2023, the IFRS Foundation staff issued an "IFRS for SMEs Accounting Standard Update." It is critical to note that this document was a staff summary of news and activities; it was not a standard-setting document and had not been reviewed by the IASB.

This staff summary offered valuable insights into the IASB's ongoing work, including updates on the redeliberations for the Third Edition, a preview of a forthcoming addendum to the Exposure Draft, and an overview of the future standard for subsidiaries (which would become IFRS 19).

SME Implementation Group (SMEIG)

A key part of the December 2023 update focused on the SME Implementation Group (SMEIG), a body that supports the international adoption of the standard and addresses implementation questions. During its meeting on December 5, 2023, the SMEIG provided vital advice to the IASB on several topics under consideration for the Third Edition of the IFRS for SMEs Standard.

Key areas of discussion included:

- Revenue from Contracts with Customers: The group debated proposed changes to Section 23, covering contract modifications, warranties, and customer options. SMEIG members shared practical feedback on the necessity of certain requirements and the potential cost burden of new disclosures, such as disaggregated revenue.

- Addendum to the Exposure Draft: The SMEIG advised on aligning the standard with recent amendments to full IFRS concerning supplier finance arrangements and the lack of exchangeability.

- Impairment of Financial Assets: The group deliberated on the number of SMEs with significant credit risk exposure, a key factor in revising impairment rules.

This detailed feedback from the SMEIG was instrumental in the IASB's redeliberations, ensuring the final standard was both robust and practical for SMEs by testing simplification principles against real-world challenges.

The Second Comprehensive Review: Paving the Way for the Third Edition

The path to the Third Edition officially began in 2019 with the IASB's second comprehensive review. These reviews are conducted periodically to keep the standard current. The scope of this review included new and amended full IFRS Standards issued since the last update in 2015, as well as extensive stakeholder consultation.

This rigorous process led to the publication of an Exposure Draft (ED) in September 2022, followed by an Addendum in March 2024 to incorporate further feedback and alignments. The extended timeline from 2019 to 2025 underscores the meticulous effort required to balance two competing goals: maintaining alignment with full IFRS principles while ensuring the standard remains simplified and cost-effective for SMEs.

Issuance of the Third Edition: A Landmark Update for 2025

On February 27, 2025, the IASB culminated this extensive review by issuing the Third Edition of the IFRS for SMEs® Accounting Standard. This substantially revised version marks a significant update for accounting practices for all eligible entities.

The Third Edition becomes effective for annual reporting periods starting on or after January 1, 2027, with early application permitted to allow entities ample time to prepare.

To facilitate a smooth transition, the IFRS Foundation is providing comprehensive support materials, including:

- A marked-up version of the standard showing all changes from the second edition.

- Updated educational modules to reflect the new requirements, with priority given to sections with major changes like Module 11 on Financial Instruments.

The Third Edition of the IFRS for SMEs Standard

Effective Date: January 1, 2027

The Third Edition of the IFRS for SMEs Accounting Standard introduces pivotal changes designed to improve the quality and comparability of financial reporting for non-publicly accountable entities. These updates strictly adhere to the core principles of simplification and cost-effectiveness that define the standard.

Core Principles Guiding the Revisions

The IASB's approach to updating the standard is guided by a consistent set of principles. The goal is to incorporate relevant developments from full IFRS, but only when the changes are appropriate for SMEs, can be implemented without undue cost or effort, and ensure a faithful representation of the company's financial reality.

The key principles underpinning the Third Edition are:

- Relevance to SMEs: Amendments are only adopted if the underlying transactions or events are common for SMEs and the resulting information is useful to the users of their financial statements.

- Simplicity: When aligning with a full IFRS Standard, the IASB actively simplifies the requirements. This is achieved in several ways:

- Omitting irrelevant topics, such as earnings per share, interim financial reporting, and segment reporting.

- Removing complex accounting policy choices available in full IFRS when a simpler alternative exists for SMEs.

- Simplifying recognition and measurement principles to make them easier to apply.

- Substantially reducing required disclosures, with an estimated 90% reduction compared to the requirements in full IFRS.

- Using plain, clear language to make the standard easier to understand and translate globally.

- Faithful Representation: Despite extensive simplification, the standard is designed to ensure that SMEs can provide a financial report that faithfully represents their financial position, performance, and cash flows.

- Cost-Benefit Analysis: The IASB meticulously weighs the benefits of any change for financial statement users against the implementation costs for SMEs.

These guiding principles ensure the IFRS for SMEs® Accounting Standard remains a practical and highly effective reporting framework, specifically tailored to the unique environment of smaller entities around the world.

The following table provides a high-level comparison of key areas between the Second (2015) and Third (2025) Editions:

Table 1: Key Amendments: Second vs. Third Edition of IFRS for SMEs Accounting Standard

| Area of Standard (Section No.) | Key Aspect in Second Edition (2015) | Key Aspect in Third Edition (2025) | Primary Alignment with Full IFRS | Brief Rationale/Key Simplification for SMEs |

|---|---|---|---|---|

| Conceptual Basis (Section 2) | Based on the 1989 IASB Framework and some concepts from the 2010 Conceptual Framework. | Revised to align with the IASB’s 2018 Conceptual Framework for Financial Reporting. | 2018 Conceptual Framework | Ensures foundational principles are consistent with full IFRS, enhancing coherence. Updated definitions, recognition criteria, and concepts like prudence and stewardship. |

| Statement of Cash Flows (Section 7) | General guidance aligned with IAS 7. | Now requires reconciliation of liabilities from financing activities and disclosures for supplier finance arrangements. | IAS 7 | Improves transparency of financing activities and cash‐flow movements, reflecting current practices like supplier financing. |

| Consolidation (Section 9) | Two control assessment models. | Adopts a single definition of “control” aligned with IFRS 10; parent measures retained interest at fair value on loss of control of a subsidiary. | IFRS 10 | Enhances consistency in consolidation. Fair-value treatment on loss of control aligns with full IFRS principles. |

| Financial Instruments (Section 11) | Separate Sections 11 (basic) & 12 (other); option to apply IAS 39 recognition/measurement; incurred‐loss model for impairment. | Combined into a single Section 11; aligned with IFRS 9 principles (e.g. SPPI-like criteria for amortized cost) but retains an incurred-loss model. IAS 39 option removed. | IFRS 9 | Simplifies structure and removes the outdated IAS 39 option. Keeps incurred-loss model for SMEs due to cost-benefit considerations. |

| Fair Value Measurement (Section 12) | Fair‐value guidance dispersed across various sections. | New standalone Section 12 consolidating fair-value guidance, aligned with IFRS 13 for measurement and disclosure. | IFRS 13 | Centralizes FV guidance for clarity and consistency, improving the quality of fair‐value information. |

| Business Combinations (Section 19) | Definition of a business based on older IFRS 3; acquisition costs capitalized. | Definition of “business” aligned with current IFRS 3; acquisition costs expensed; contingent consideration at fair value if no undue cost/effort; goodwill still amortized. | IFRS 3 | Improves consistency with full IFRS for business definition and acquisition costs. SME relief (“undue cost/effort”) for contingent consideration; retains goodwill amortization for simplicity. |

| Revenue Recognition (Section 23) | Based on IAS 18 Revenue and IAS 11 Construction Contracts. | Revised and renamed “Revenue from Contracts with Customers,” aligned with IFRS 15 using a simplified five-step model. | IFRS 15 | Modernizes revenue recognition based on control transfer. Practical expedients and concise language make the model more manageable for SMEs. |

| Development Costs (Section 18) | All research and development costs expensed. | Retains requirement that all research and development costs are expensed. | Deliberate divergence from IAS 38 | Simplification for SMEs: avoids complex assessments of ongoing viability and reduces preparation costs. |

| Borrowing Costs (Section 25) | All borrowing costs expensed. | Retains requirement that all borrowing costs are expensed. | Deliberate divergence from IAS 23 | Simplification for SMEs: minimizes preparation costs and maintains ease of application, enhancing comparability of debt costs. |

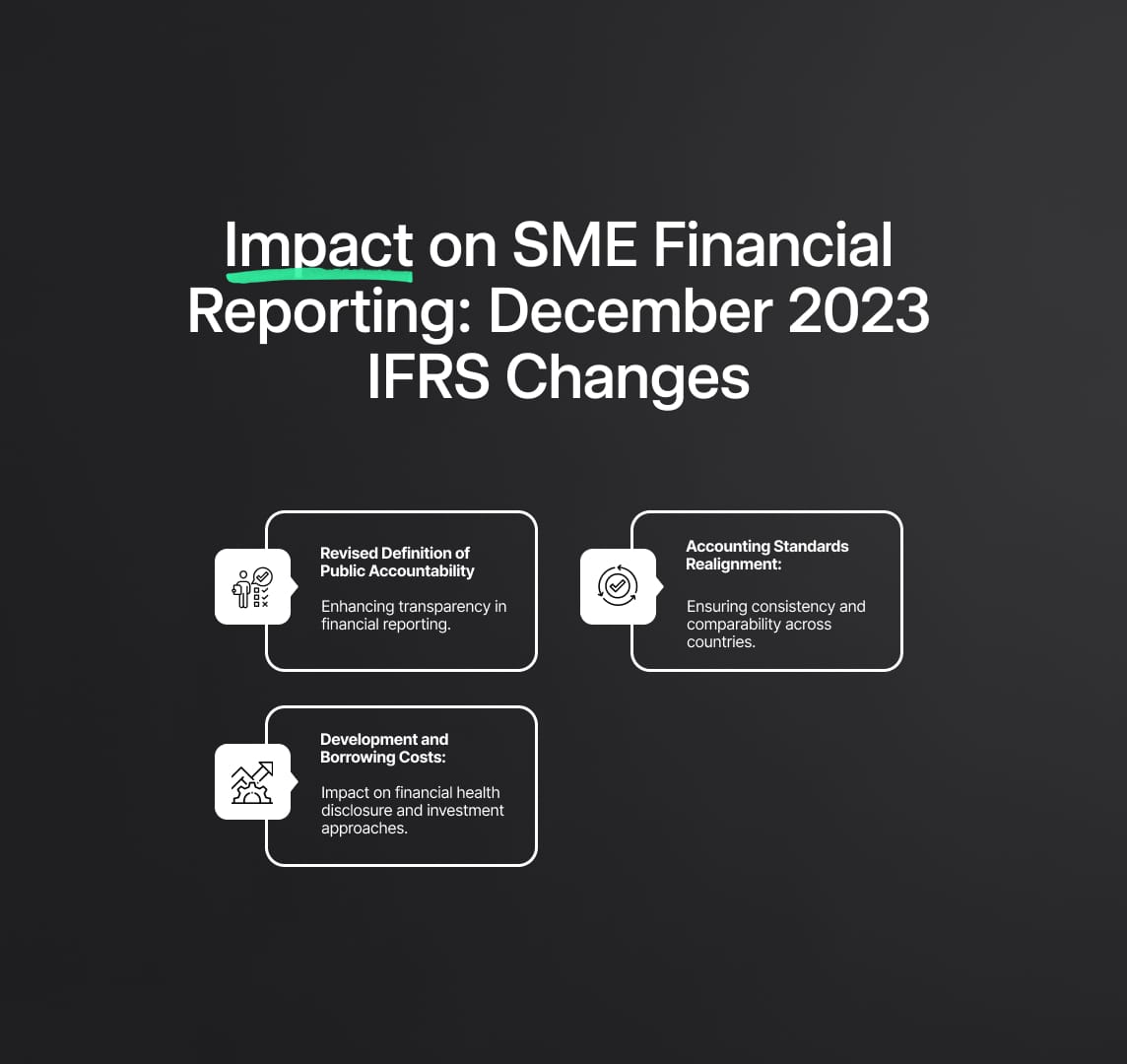

Defining 'Public Accountability' in the Third Edition

The eligibility to use the IFRS for SMEs Accounting Standard is determined by a single factor: an entity must not have public accountability. The Third Edition clarifies this crucial definition in Section 1. According to paragraph 1.3, an entity has public accountability if:

- (a) Its debt or equity instruments are traded in a public market (such as a domestic or foreign stock exchange or an over-the-counter market), or it is in the process of issuing such instruments for public trading; OR

- (b) It holds assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses (e.g., banks, credit unions, insurance companies, securities brokers/dealers, mutual funds, and investment banks).

This definition aligns with the one used in IFRS 19 Subsidiaries without Public Accountability: Disclosures. The clarification in the Third Edition enhances its operational clarity with explicit examples, rather than fundamentally changing the concept.

Importantly, a subsidiary whose parent entity uses full IFRS is not automatically barred from using the SME standard. If the subsidiary itself does not meet the definition of public accountability, it may use the IFRS for SMEs Accounting Standard for its own separate financial statements.

Key Amendments in the Third Edition IFRS for SMEs Standard

The Third Edition introduces targeted amendments across several sections, primarily to align with key principles from full IFRS where it is beneficial and practical for SMEs.

Section 2: Alignment with the Conceptual Framework

A foundational change is the revision of Section 2, Concepts and Pervasive Principles, to align with the IASB's 2018 Conceptual Framework for Financial Reporting. This is significant as the Conceptual Framework underpins all IFRS Standards.

The updated Section 2 introduces and clarifies:

- New concepts on measurement, presentation, and disclosure.

- Guidance on the derecognition of assets and liabilities.

- Updated definitions and recognition criteria for assets and liabilities.

- Clarified concepts of prudence, stewardship, and measurement uncertainty.

This change enhances the internal consistency of the standard and has pervasive implications for how preparers interpret and apply all of its requirements.

Section 7: Enhanced Statement of Cash Flows

Section 7, Statement of Cash Flows, is updated to improve alignment with IAS 7. A key enhancement is a new requirement to disclose a reconciliation of liabilities arising from financing activities, which must show financing cash flows separately from non-cash changes (e.g., acquisitions or foreign exchange movements).

Additionally, reflecting modern financing practices, the revised Section 7 now requires disclosures about an entity's supplier finance arrangements, providing users with more transparent information about liquidity and cash management.

Section 9: A New Approach to Consolidated Financial Statements

Section 9, Consolidated and Separate Financial Statements, is significantly updated to align with IFRS 10. The most important change is the adoption of a single definition of 'control' as the sole basis for consolidation.

Furthermore, the revised section adds new rules for the loss of control of a subsidiary. Any retained interest in the former subsidiary must be measured at fair value on the date control is lost, with any gain or loss recognized in profit or loss. This promotes greater consistency and comparability.

Section 11: A Complete Overhaul of Financial Instruments (IFRS 9 Alignment)

One of the most substantial revisions is to Section 11, Financial Instruments, which now combines the previous Sections 11 and 12. The new section incorporates simplified principles from IFRS 9 Financial Instruments.

Classification and Measurement

- The standard continues to primarily use an amortized cost model.

- The option for SMEs to apply the recognition and measurement rules of IAS 39 has been removed to improve consistency.

- Investments in certain shares are measured at fair value through profit or loss (FVTPL) only if publicly traded or otherwise reliably measurable; otherwise, they are measured at cost less impairment.

- In a key simplification, entities are not required to reassess the classification of a financial instrument after its initial recognition.

Impairment

- Crucially, the Third Edition retains the incurred loss model for impairment. An impairment loss is recognized only when there is objective evidence of a loss event.

- This is a deliberate and significant divergence from IFRS 9, which mandates a more complex, forward-looking expected credit loss (ECL) model. The IASB retained the incurred loss model based on cost-benefit feedback that the ECL model would be unduly burdensome for SMEs.

Hedge Accounting

- Hedge accounting is still permitted, but the qualifying criteria and eligible risks are more restrictive than under full IFRS 9.

These changes to Section 11 introduce modern accounting concepts while carefully avoiding the full complexity of IFRS 9, striking a balance tailored for SMEs.

The following table summarizes key simplifications in Section 11 compared to full IFRS 9:

Table 2: IFRS 9 Financial Instruments: Key Simplifications for SMEs in Section 11 (Third Edition)

| Aspect of Financial Instrument Accounting (IFRS 9) | Approach in Full IFRS 9 (Brief) | Simplified Approach in IFRS for SMEs Section 11 (Third Edition) | Rationale for SME Simplification (Cost-Benefit, Complexity Reduction) |

|---|---|---|---|

| Classification of Financial Assets | Complex model with categories: Amortized Cost (AC), Fair Value Through Other Comprehensive Income (FVOCI), Fair Value Through Profit or Loss (FVTPL), based on business-model and SPPI tests. | Primarily an AC model for “basic financial instruments” meeting simplified SPPI-like criteria. Limited FVTPL for certain equity investments if FV reliably measurable without undue cost or effort; otherwise cost less impairment (para S11.14(c)). No FVOCI category for debt instruments. | Reduces complexity of multiple measurement categories and detailed business-model assessments. “Undue cost or effort” relief simplifies valuation of unquoted equities. |

| Impairment of Financial Assets | Forward-looking Expected Credit Loss (ECL) model (12-month ECL or lifetime ECL). Requires significant estimation and data. | Incurred loss model: impairment recognized when objective evidence of a loss event exists. | Significantly reduces complexity and data requirements. ECL model deemed too burdensome for typical SMEs with simple receivables. |

| Reclassification of Financial Assets | Required in specific circumstances when the entity’s business model for managing financial assets changes. | No reassessment of classification required after initial recognition. | Simplifies ongoing accounting and avoids complex reclassification adjustments. |

| Hedge Accounting | Extensive and flexible hedge-accounting model, with detailed qualification and documentation requirements. | Permitted for specific risks and instruments, with simplified effectiveness testing. | Provides SMEs access to hedge accounting without the full complexity of IFRS 9’s requirements. |

| Measurement of Equity Investments | Default FVTPL, with an irrevocable option at initial recognition to present changes of non-trading equity investments in OCI. | FVTPL only if publicly traded or FV is reliably measurable without undue cost or effort; otherwise cost less impairment (para S11.14(c)). | Avoids mandatory FV measurement for unquoted equities where valuation may be difficult or costly for SMEs. |

Section 12: A New Hub for Fair Value Measurement (IFRS 13 Alignment)

A significant structural improvement in the Third Edition is the introduction of a new, standalone Section 12, Fair Value Measurement. Previously, guidance on this topic was scattered throughout the standard. This new section consolidates all fair value requirements and aligns them with the principles of IFRS 13 Fair Value Measurement.

The new Section 12 includes:

- A definition of fair value consistent with IFRS 13: the price to sell an asset or transfer a liability in an orderly transaction between market participants.

- Principles for measuring fair value, including simplified guidance on valuation techniques and the fair value hierarchy (Levels 1, 2, and 3).

- Specific disclosure requirements related to fair value measurements.

By centralizing this guidance, the IASB aims to improve the clarity, consistency, and quality of fair value measurements by SMEs. This is critical because fair value is required or permitted in many other areas, including Financial Instruments (Section 11), Investment Property (Section 16), and Business Combinations (Section 19). A clear understanding of Section 12 is therefore essential for the correct application of these related sections.

Section 19: Revised Rules for Business Combinations and Goodwill (IFRS 3 Alignment)

Section 19, Business Combinations and Goodwill, has been updated to enhance alignment with IFRS 3 Business Combinations.

Key changes include:

- Definition of a 'Business': The definition of what constitutes a business is now aligned with IFRS 3, which is crucial for distinguishing a business combination from a simple asset acquisition.

- Contingent Consideration: This must now be measured at fair value, but with a key SME simplification: an "undue cost or effort" exemption.

- Acquisition Costs: In line with IFRS 3, costs related to an acquisition (e.g., legal and due diligence fees) must now be expensed as incurred, not capitalized.

- Goodwill: The standard retains its requirement for the amortization of goodwill. This is a notable and deliberate divergence from full IFRS (which uses an impairment-only model) and is kept for the sake of simplicity.

These amendments improve consistency with full IFRS while retaining targeted simplifications that reduce complexity for smaller entities.

Section 23: A New Five-Step Model for Revenue (IFRS 15 Alignment)

One of the most impactful changes in the Third Edition is the complete rewrite of Section 23, now titled Revenue from Contracts with Customers. The section is now aligned with the principles of the landmark standard IFRS 15.

The revised Section 23 implements a simplified version of the IFRS 15 five-step model. The core principle is that an entity recognizes revenue to show the transfer of goods or services in an amount that reflects the consideration it expects to receive.

The simplifications embedded in the model for SMEs were developed based on extensive feedback and include:

- Using simple, concise language.

- Limiting the amount of judgment and information required.

- Omitting topics from IFRS 15 not generally relevant to SMEs.

- Providing simplified disclosure requirements.

Input from the SMEIG on practical issues like contract modifications, warranties, and disclosures was highly influential in shaping this user-friendly yet robust new section.

The following table details the simplifications within the five-step model as implemented in Section 23:

Table 3: IFRS 15 Five-Step Model: Simplifications for SMEs in Section 23 (Third Edition)

| Step in Revenue Recognition Model (IFRS 15) | Core Principle (Brief from IFRS 15) | Key Simplification/Application in IFRS for SMEs Section 23 (Third Edition) | Example of Practical Implication for an SME |

|---|---|---|---|

| Step 1: Identify the contract(s) with a customer | Contract exists if criteria (approval, identifiable rights, payment terms, commercial substance, probable collection) are met. | Simplified criteria focusing on approval, commercial substance, and probability of collecting the consideration to which the entity is entitled. | An SME might only require a signed agreement and basic credit check, without assessing every detailed IFRS 15 criterion. |

| Step 2: Identify the performance obligations in the contract | Separate promises to transfer distinct goods or services; distinct if the customer can benefit on its own (or with readily available resources) and the promise is separately identifiable. | Concise definition of “distinct.” Promises are distinct if (a) the customer can benefit on its own and (b) they are separable. Pragmatic expedient: customer options accounted as separate only if they confer a material right and can be executed without undue cost or effort. | A software SME selling both a license and installation can readily treat them as separate if the license works with other installers and the installation service stands alone; material-right options are simplified. |

| Step 3: Determine the transaction price | Consideration expected, including variable consideration (constrained), financing components, non-cash consideration, and pay-back to customer. | Include variable consideration only if highly probable no significant reversal. Optional exemption for financing component if payment ≤1 year (with disclosure). Non-cash consideration at fair value or stand-alone selling price if FV not reasonably estimable. | An SME offering volume discounts only includes the discount if it’s highly probable. The one-year financing exemption avoids interest calculations on short-term sales. |

| Step 4: Allocate the transaction price to performance obligations | Allocate proportionally based on relative stand-alone selling prices (SSP); estimate SSP if not directly observable. | Same allocation principle, but with less prescriptive guidance on estimating SSP. | An SME selling equipment plus a service contract allocates total proceeds based on standalone prices; simpler estimation methods suffice if precise SSPs aren’t available. |

| Step 5: Recognise revenue when (or as) performance obligations are satisfied | Revenue when control transfers (over time or at a point in time). | Guidance on control transfer (ability to direct use and obtain benefits). Three over-time criteria. Practical expedient: recognize revenue to the amount the entity has the right to invoice if it corresponds directly to work performed. | An SME building custom furniture recognizes revenue over time if the customer is obliged to pay for work completed. The right-to-invoice expedient streamlines progress measurement. |

This alignment with IFRS 15 principles, even in a simplified form, is a major step towards improving the relevance and comparability of revenue information reported by SMEs.

Deliberate Divergence: Why Development and Borrowing Costs are Expensed

In two notable areas, the Third Edition of the IFRS for SMEs® Accounting Standard intentionally maintains a simpler approach than full IFRS. This highlights the IASB's pragmatic focus on cost-benefit and usability for smaller entities.

Development Costs

The standard continues to require that all research and development costs be expensed when incurred. The IASB considered allowing SMEs to capitalize development costs that meet the criteria in IAS 38 Intangible Assets. However, this was rejected for two key reasons:

- Practicality: Feedback indicated that SMEs often lack the resources to reliably perform the ongoing viability assessments required for capitalization under IAS 38.

- Usefulness: Some IASB members argued that capitalizing only a portion of these costs might not provide useful information to users.

Therefore, the simpler approach of expensing all development costs was retained to reduce complexity and ensure the standard remains cost-effective.

Borrowing Costs

Similarly, the Third Edition requires that all borrowing costs be expensed in the period they are incurred. This is a deliberate divergence from IAS 23 Borrowing Costs, which requires capitalization of certain borrowing costs as part of an asset's cost.

The IASB chose to maintain the simpler expensing model to minimize preparation costs for SMEs. It was also argued that presenting all borrowing costs in one place in the financial statements makes it easier for users to assess an entity's cost of debt and forecast its cash flows.

Section 16: Accounting for Investment Property

Section 16 provides specific rules for investment property, property held to earn rentals or for capital appreciation.

- Initial Measurement: Investment property is initially measured at its cost, including the purchase price and any directly attributable transaction costs (e.g., legal fees, transfer taxes).

- Subsequent Measurement: After initial recognition, SMEs have a choice, contingent on whether fair value is reliably measurable without undue cost or effort:

- Fair Value Model: If fair value can be measured reliably without undue cost or effort on an ongoing basis, the entity must use this model. The property is re-measured to fair value at each reporting date, with changes recognized in profit or loss.

- Cost Model: If fair value cannot be measured reliably without undue cost or effort, the entity must use the cost model from Section 17 (cost less accumulated depreciation and impairment). The "undue cost or effort" exemption (detailed in paragraph 2.14C) is a critical simplification.

Specific disclosure requirements apply depending on the model used, as referenced in paragraphs 16.10 and 17.32-17.34. This framework provides a practical approach for a common asset class, with the exemption playing a vital role in making the standard workable for all SMEs.

Adopting the Third Edition: Transition Rules and Early Application

The Third Edition of the IFRS for SMEs Accounting Standard is effective for annual reporting periods beginning on or after January 1, 2027. Early application is permitted, provided it is disclosed.

While the standard generally requires retrospective application, the IASB has provided crucial transitional relief to ease the burden on SMEs for several major changes:

- Section 12 (Fair Value Measurement): The new requirements are to be applied prospectively from the date of adoption.

- Section 19 (Business Combinations): The amended rules are to be applied prospectively to business combinations that occur on or after the date of adoption.

- Section 23 (Revenue): SMEs can choose to continue applying the old revenue rules to contracts that are already in progress at the date of adoption, avoiding the need to restate all ongoing contracts.

- Financial Instruments: Other simplifications are available for entities that previously used the IAS 39 option, which has now been removed.

These transition provisions are essential for facilitating a smooth adoption. They acknowledge the practical constraints of SMEs and allow for a more phased implementation of the most significant changes, encouraging timely and effective compliance.

IFRS 19: A New Disclosure Standard for Subsidiaries

Alongside the evolution of the IFRS for SMEs Accounting Standard, the IASB has launched a new standard that specifically targets the disclosure requirements for eligible subsidiaries, offering significant relief.

What is IFRS 19? An Overview

In May 2024, the International Accounting Standards Board (IASB) issued IFRS 19 Subsidiaries without Public Accountability: Disclosures. This new standard is effective for annual reporting periods beginning on or after January 1, 2027, with earlier application permitted.

IFRS 19 creates an alternative financial reporting path for certain subsidiaries. It gives them a new choice: instead of applying full IFRS Accounting Standards with extensive disclosures, they can now apply full IFRS with the reduced disclosures of IFRS 19, providing a valuable alternative to the IFRS for SMEs® Accounting Standard.

The Objective of IFRS 19: Reducing the Disclosure Burden

The core purpose of IFRS 19 is to provide a simplified set of disclosure requirements for eligible subsidiaries. It is critical to understand that IFRS 19 is a disclosure-only standard. An entity choosing to apply it must still follow all the recognition and measurement requirements of full IFRS Accounting Standards. The relief is solely in the volume of notes to the financial statements.

This standard directly addresses a long-standing issue where subsidiaries without public accountability were often required to produce costly and extensive disclosures simply because their parent company reported under full IFRS. IFRS 19 offers a more proportionate approach, reducing the compliance burden without affecting the underlying accounting used for group consolidation. The application of IFRS 19 is entirely voluntary.

Who Can Apply IFRS 19? Key Eligibility Criteria

A subsidiary is permitted to apply IFRS 19 in its financial statements if, and only if, it meets both of the following criteria at its reporting date:

- It does not have public accountability. The definition aligns perfectly with the IFRS for SMEs® Accounting Standard. An entity has public accountability if:

- Its debt or equity instruments are traded in a public market, or it is in the process of issuing them.

- It holds assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses (e.g., banks, insurance companies, investment funds).

- Its parent company produces publicly available consolidated financial statements prepared under IFRS Accounting Standards.

The rationale is clear: if the parent already provides full IFRS-compliant information to the public, the need for the subsidiary to replicate those extensive disclosures is significantly reduced.

The following checklist can help entities assess their eligibility:

Table 4: Eligibility Checklist for Applying IFRS 19 Disclosures

| Question | Response Options | Implication for Eligibility |

|---|---|---|

|

1. Does the entity (subsidiary) have public accountability as defined in IFRS 19? (i.e., debt/equity instruments traded in a public market or in the process of issuing them; OR holds assets in a fiduciary capacity for a broad group of outsiders) |

Yes / No |

If Yes, the entity is INELIGIBLE to apply IFRS for SMEs. If No, proceed to Question 2. |

| 2. Is the entity a subsidiary whose ultimate or intermediate parent produces consolidated financial statements available for public use? | Yes / No |

If No, the entity is INELIGIBLE. If Yes, proceed to Question 3. |

| 3. Are the parent's publicly available consolidated financial statements prepared in accordance with full IFRS Accounting Standards? | Yes / No |

If No, the entity is INELIGIBLE. If Yes (and Question 1 was No), the entity is ELIGIBLE. |

| Overall Eligibility Conclusion: | – |

The entity is ELIGIBLE if it answers No to Q1, Yes to Q2, and Yes to Q3. Otherwise, it is INELIGIBLE. |

Key Implications of Adopting IFRS 19

The introduction of IFRS 19 creates several important strategic implications for eligible subsidiaries and their parent companies.

- Reduced Disclosure Burden: The most immediate benefit is a significant reduction in the volume and complexity of disclosures compared to full IFRS. This leads directly to cost savings and a less time-consuming financial reporting process.

- Continued IFRS Compliance: Subsidiaries applying IFRS 19 must still use the same recognition and measurement principles as full IFRS Accounting Standards. This ensures high-quality financial data that remains perfectly aligned with group reporting for consolidation.

- Streamlined Group Reporting: IFRS 19 may encourage more subsidiaries to adopt IFRS for their statutory financial statements. Those currently using a local GAAP for statutory reports while providing IFRS figures for consolidation can eliminate this dual reporting burden, especially where local GAAP differs significantly from IFRS.

- Voluntary and Flexible Application: Adopting IFRS 19 is voluntary. An eligible subsidiary can elect to use it and can also choose to apply or revoke its use in different reporting periods, offering significant flexibility to adapt to changing circumstances or stakeholder needs.

- Stakeholder and Regulatory Considerations: An entity must still consider the needs of local stakeholders (like lenders or regulators) and may voluntarily provide disclosures beyond the IFRS 19 minimum. Notably, for entities with U.S. market exposure, the staff of the U.S. Securities and Exchange Commission (SEC) has issued guidance regarding the use of IFRS 19 in SEC filings that must be considered.

- Explicit Statement of Compliance: A subsidiary that applies the standard must state clearly in its financial statements that it has complied with IFRS Accounting Standards by applying IFRS 19 Subsidiaries without Public Accountability: Disclosures.

IFRS 19 vs. the IFRS for SMEs Standard: A Clear Distinction

It is crucial to understand that IFRS 19 and the IFRS for SMEs® Accounting Standard are two distinct frameworks that are not interchangeable.

- IFRS 19 is designed for subsidiaries within a full IFRS group. It allows them to maintain the group's full IFRS recognition and measurement policies while providing reduced disclosures.

- The IFRS for SMEs Standard is a comprehensive, self-contained framework. It offers both simplified recognition and measurement principles and reduced disclosures. It is designed for a broader range of standalone non-publicly accountable entities.

The choice between these standards depends entirely on a company's specific situation, group structure, and stakeholder needs, as their underlying accounting bases are fundamentally different.

Reduce your

compliance risks