IFRS S1 and S2 Implementation

Evolving Financial Reporting delves into the ICAEW's advocacy for IFRS S1 & S2, spotlighting the urgent need for unified sustainability standards. As the ISSB and IASB navigate the future, the successful integration of these standards could revolutionise global financial reporting.

ICAEW Urges ISSB to Prioritise Implementation of IFRS S1 and S2

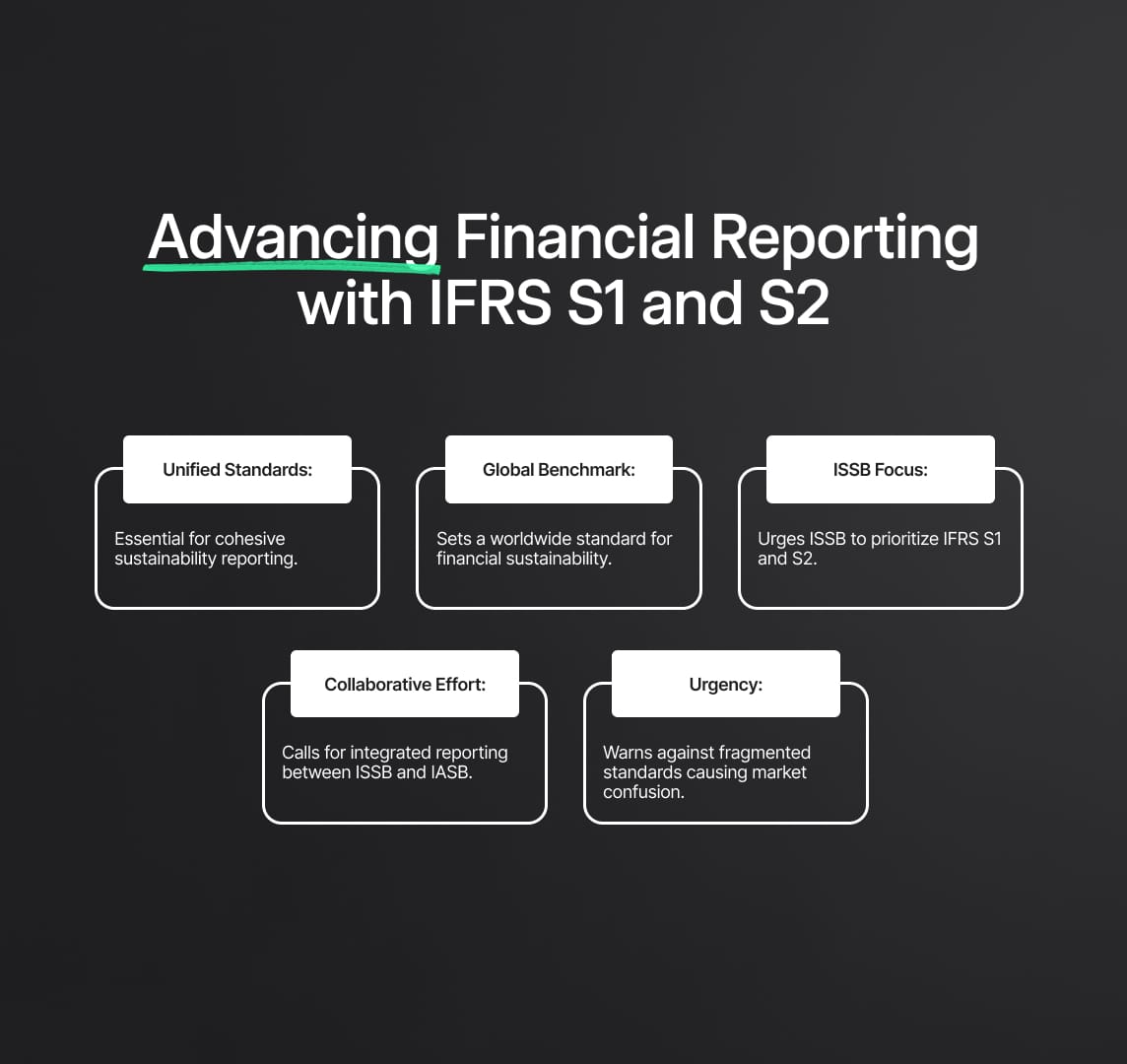

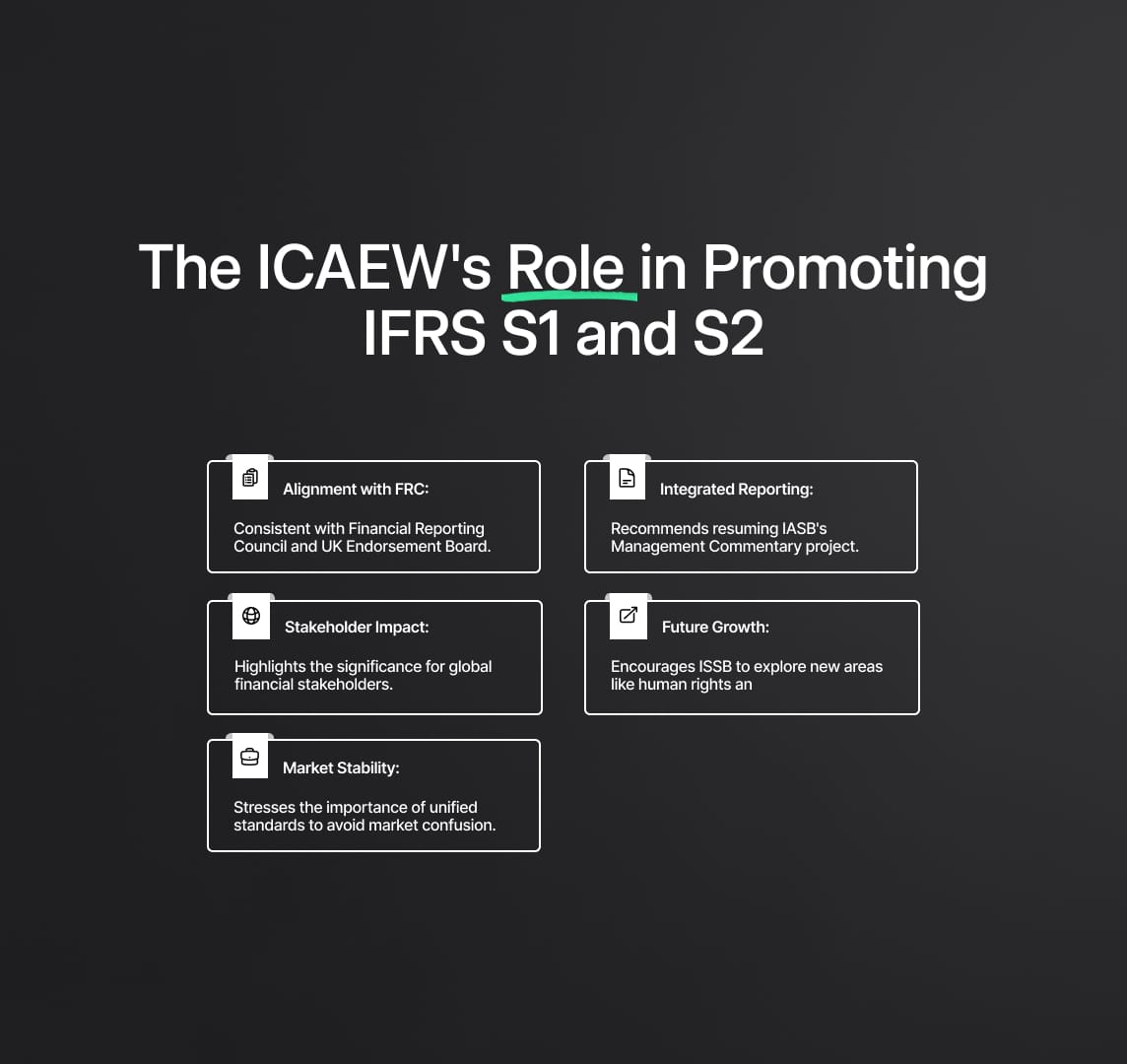

The International Sustainability Standards Board (ISSB) has received strong recommendations from the Institute of Chartered Accountants in England and Wales (ICAEW) to prioritize the implementation of the International Financial Reporting Standards S1 and S2 (IFRS S1 and S2). This position is consistent with that of the Financial Reporting Council (FRC) and the UK Endorsement Board. Additionally, the International Standards Board (IASB) and the International Standards Standards Board (ISSB) are to collaborate closely on an integrated reporting effort. After the ISSB was established, the Management Commentary project, which had been started by the IASB, was put on pause. However, if it were to be picked up again, it might yield insightful information. The significance of the ISSB establishing a clear intention to advance past S2 is likewise emphasized by the ICAEW. The ICAEW warns that in the absence of this, standards from other organizations may fill the void and cause confusion in the market.

Financial Reporting: The ICAEW's Push for IFRS S1 & S2

The Institute of Chartered Accountants in England and Wales (ICAEW) has been a well-known proponent of strong and open sustainability standards in the rapidly changing field of global financial reporting. Their recent focus on the International Financial Reporting Standards S1 and S2 (IFRS S1 and S2) highlights how urgently we need to reconcile both financial and non-financial narratives in sustainability reporting through a single, cohesive methodology.

The position of the ICAEW, which aligns with the viewpoints of the Financial Reporting Council (FRC) and the UK Endorsement Board, indicates a developing consensus throughout the financial world. The central idea of this movement? a strong plea to the International Sustainability Standards Board (ISSB) to give the IFRS S1 and S2 top priority on their agenda, followed by the resumption of the IASB's Management Commentary project—an endeavor that had been put on hold due to changing regulatory circumstances.

Why is this relevant to stakeholders in the global financial system? The successful adoption of IFRS S1 and S2 worldwide may establish the benchmark for reporting on financial sustainability. The ISSB's future growth into new subject areas, such as urgent human rights issues or the dynamics of human capital, might be strengthened by such a well-coordinated framework. But if proactive measures aren't taken, there's a chance that different standards from different organizations will muddy the financial picture and cause uncertainty in the market.

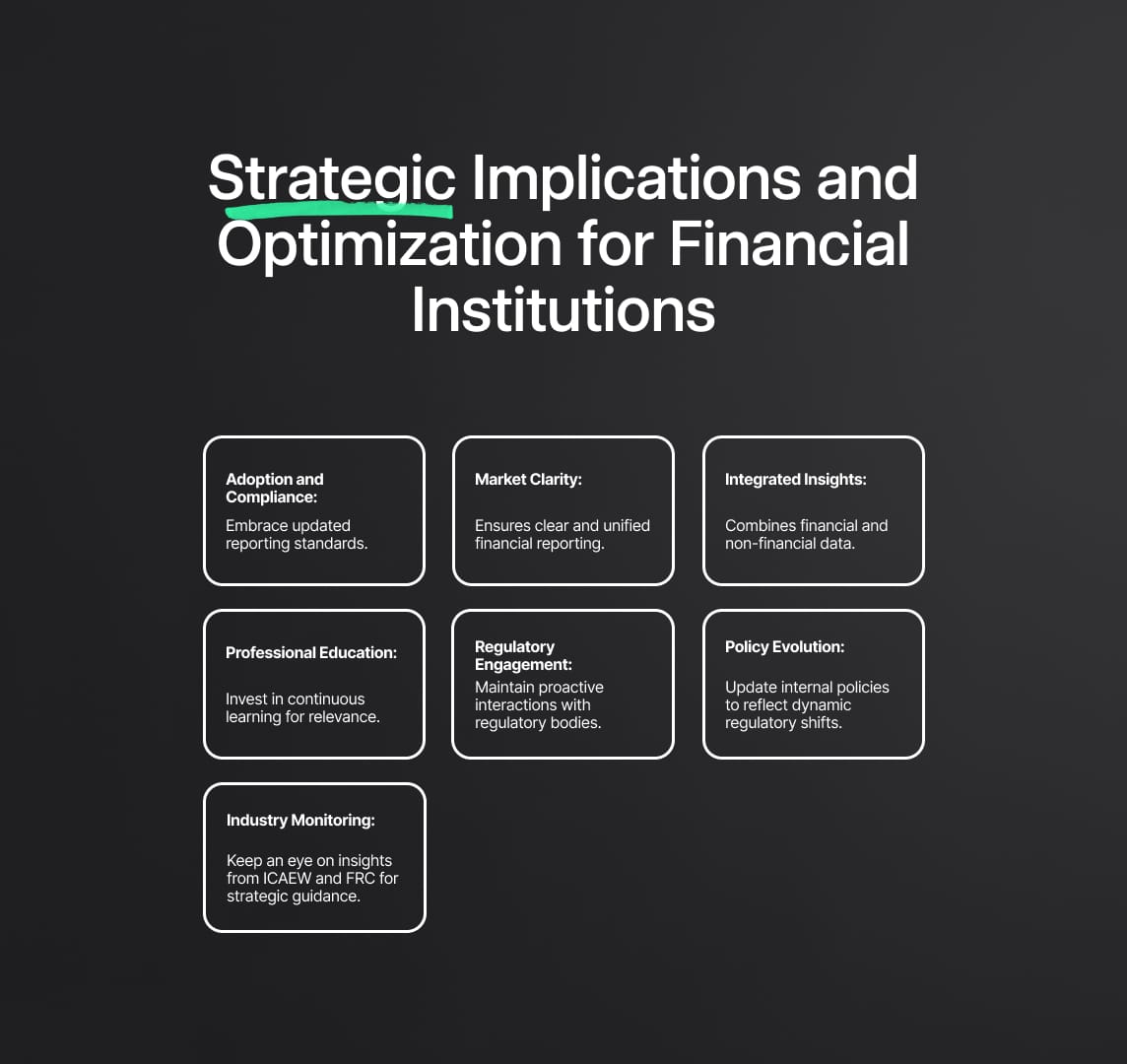

The symbiotic relationship between the International Accounting Standards Board (IASB) and the ISSB is also emphasized in the ICAEW's clarion cry. The fundamental structure of financial reporting might be redefined by an integrated reporting strategy that combines non-financial and financial insights. Financial institutions, particularly banks and organizations that follow IFRS, have a crucial role to play in this new paradigm. Their road map? Accept the updated reporting requirements, be on the lookout for any potential uncertainties in the market, and promote integrated reporting.

Optimizing for the Future: Investing in continuous professional education, being proactive in interactions with regulatory bodies, evolving internal policies to reflect dynamic regulatory shifts, and keeping an eye on insights from industry leaders such as the ICAEW and FRC are all essential for institutions looking to optimize for the future and remain relevant in this ever-changing landscape.

In conclusion, the ICAEW's advocacy and the story that is developing around IFRS S1 and S2 could very well set the path for a sustainable and integrated financial future at this critical juncture in the evolution of finance. It would be wise for all parties involved—financial institutions included—to pay attention to this trajectory in order to maintain the resilience and responsiveness of the global financial ecosystem.

Read More

Reduce your

compliance risks