MiFID II Regulation: ESMA's Consultation on Draft RTS

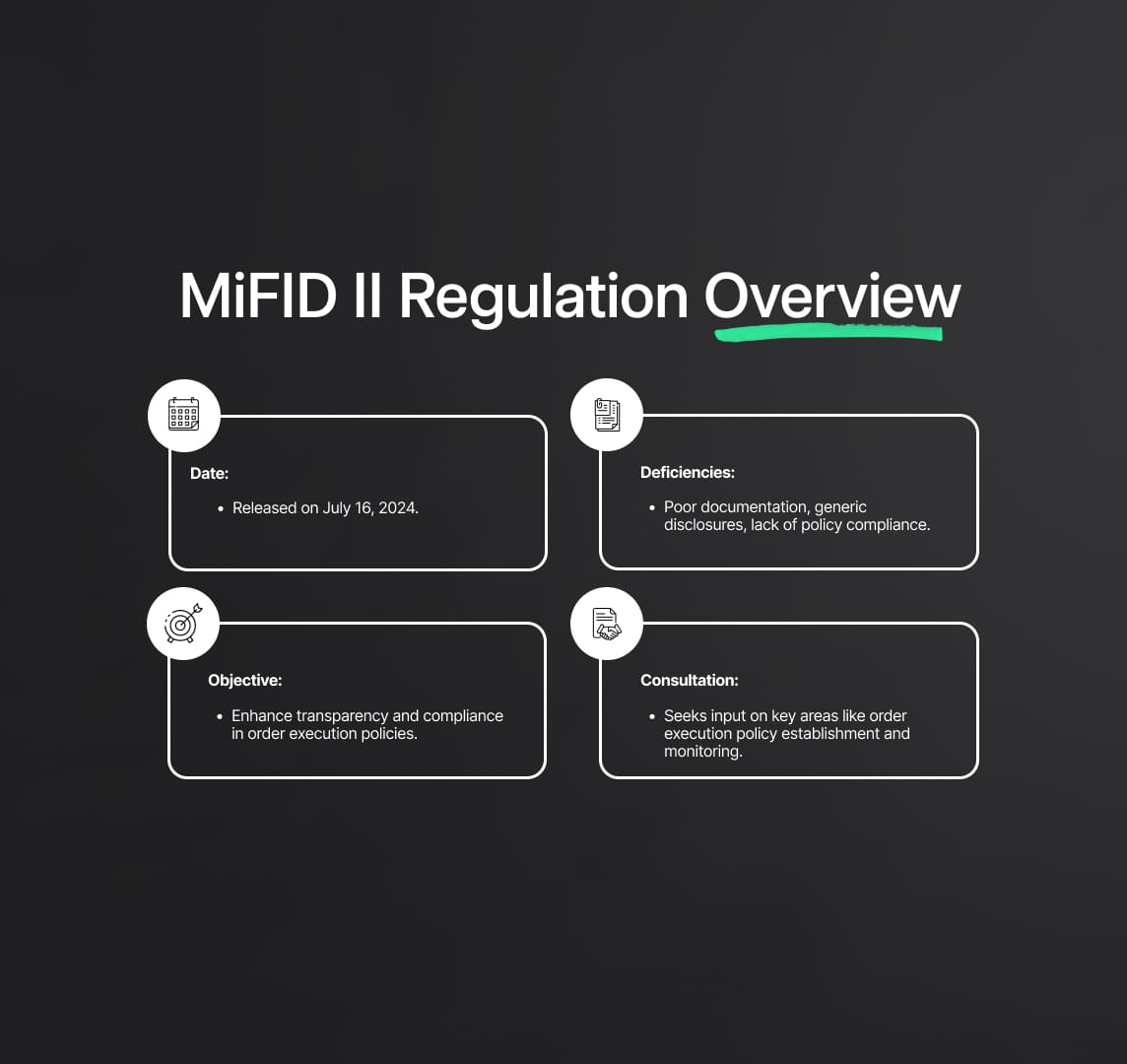

ESMA's July 16, 2024, consultation paper proposes new MiFID II standards to improve order execution policies of investment firms. It highlights current deficiencies like poor documentation and generic disclosures, emphasizing transparency and compliance.

On July 16, 2024, the European Securities and Markets Authority (ESMA) released a consultation paper detailing draft technical standards. These standards outline the criteria investment firms must follow to establish and assess the effectiveness of their order execution policies under MiFID II Regulation.

Through extensive supervisory activities and the enforcement of MiFID II best execution requirements, ESMA and competent authorities across EU Member States identified several deficiencies in how firms implemented their execution policies. Notably, it was found that in various jurisdictions:

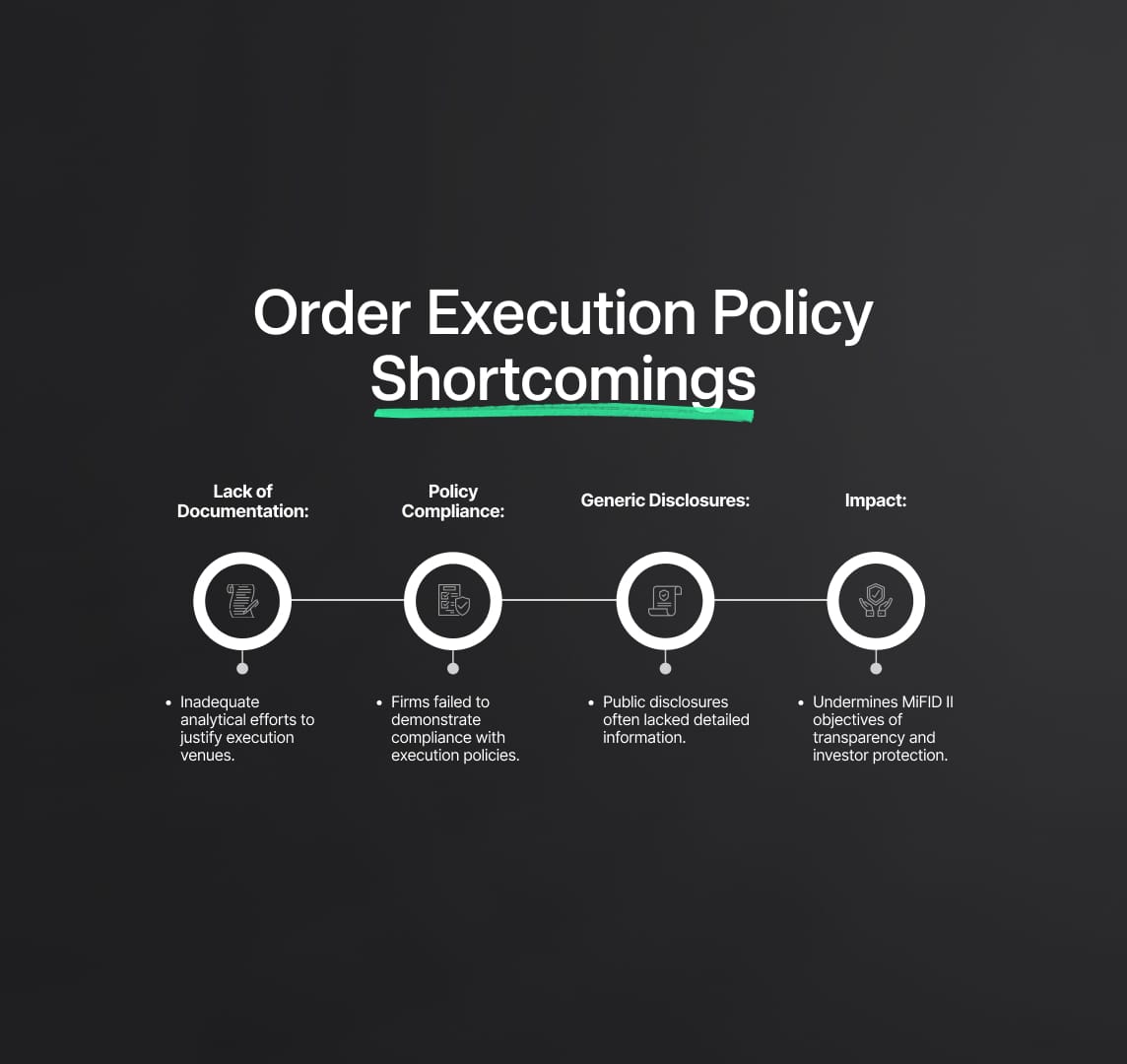

- Firms often lacked adequately documented analytical efforts to justify their choice of execution venues.

- Firms frequently failed to demonstrate compliance with their own order execution policies when executing client orders.

- Public disclosures regarding order execution policies and the steps taken to achieve the best possible result were often too generic, lacking detailed information.

Following the entry into force of the Directive amending MiFID II on March 29, 2024, Article 1(4)(e) mandates ESMA to develop regulatory technical standards (RTS) for establishing and assessing the effectiveness of investment firms' order execution policies. The consultation paper seeks input on several key areas:

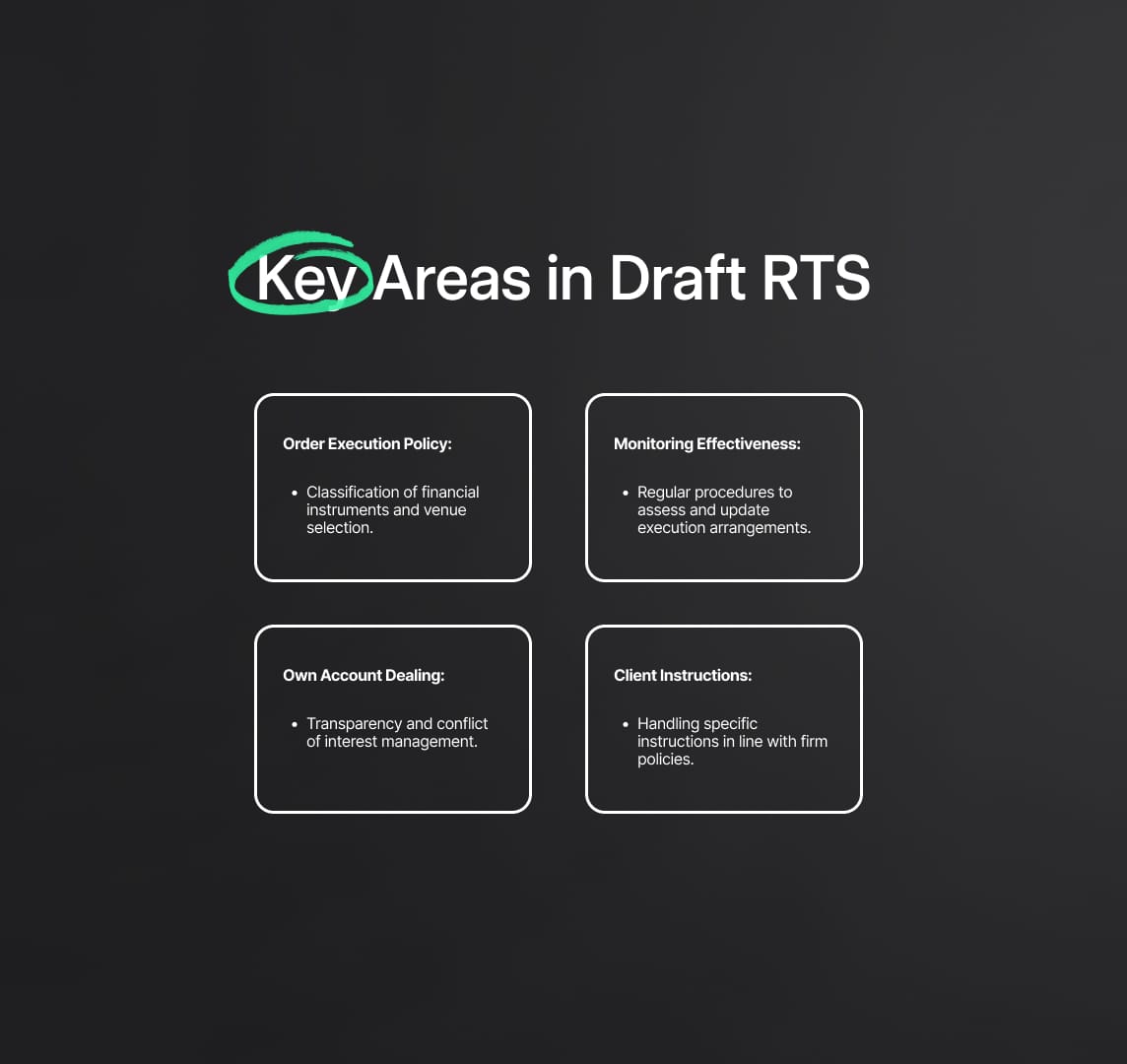

- Establishment of Order Execution Policy: This includes the classification of financial instruments in which firms execute client orders and the initial selection of venues for the order execution policy.

- Monitoring and Assessing Effectiveness: Firms must have robust procedures to regularly monitor and assess the effectiveness of their order execution arrangements and policies.

- Execution Through Own Account Dealing: The consultation addresses how firms execute client orders through own account dealing, emphasizing transparency and the avoidance of conflicts of interest.

- Handling Client Instructions: The paper explores how investment firms should manage specific client instructions to ensure they are executed in line with the firm's policies and in the best interest of the clients.

Source

[1]

Alessandro Micagni

Alessandro Micagni

Shortcomings in Current Order Execution Policies

The MiFID II Regulation mandates investment firms to adhere to rigorous order execution policies designed to secure the best possible outcomes for their clients. However, through its supervisory activities and engagements with Member State competent authorities (NCAs), the European Securities and Markets Authority (ESMA) identified several significant shortcomings in the implementation of these policies. These deficiencies undermine the effectiveness of MiFID II's objectives to enhance market transparency, improve investor protection, and ensure market integrity.

Insufficient Analytical Efforts

A critical shortcoming identified by ESMA is the lack of sufficiently documented analytical efforts by many investment firms to justify their choice of execution venues. This inadequacy directly impacts the firms' ability to demonstrate compliance with the best execution requirements under MiFID II. Without thorough analytical documentation, it is challenging for firms to substantiate that they are achieving the best possible results for their clients, as mandated by Article 27 of MiFID II.

The analytical efforts should include detailed assessments of various factors such as the price of the financial instrument, the liquidity provided by the venue, transaction costs, and the speed and likelihood of execution. Proper documentation of these assessments is crucial for transparency and accountability, allowing firms to demonstrate their decision-making process and compliance with regulatory standards.

Inadequate Demonstration of Policy Compliance

Another major issue identified is the inadequate demonstration of compliance with established order execution policies. Many firms have struggled to provide evidence that they are executing client orders in strict accordance with their stated policies. This gap raises serious concerns about the reliability and effectiveness of these policies, as well as the firms' commitment to upholding MiFID II standards.

Compliance demonstration involves not only adhering to the written policies but also consistently applying them in practice. Firms must implement robust monitoring and review mechanisms to ensure that their execution strategies are being followed and are achieving the intended outcomes. This includes regular internal audits, performance evaluations, and adjustments based on market conditions and client needs.

Generic Public Disclosures

ESMA also highlighted the issue of generic public disclosures by investment firms regarding their order execution policies. These disclosures often lack the necessary detail and specificity, providing insufficient insight into the firms' execution strategies and practices. Generic information does not adequately inform clients or regulators about the steps taken to achieve the best execution of client orders, which is a fundamental requirement under MiFID II.

To address this, firms need to ensure that their public disclosures are comprehensive and transparent. Disclosures should include specific details about the criteria used for selecting execution venues, the methodologies for assessing execution quality, and the measures in place to handle potential conflicts of interest. This level of detail helps build trust with clients and enhances regulatory oversight.

MiFID II Review and Regulatory Technical Standards (RTS)

In response to these identified shortcomings, the Directive amending MiFID II, which entered into force on March 29, 2024, mandates ESMA to develop Regulatory Technical Standards (RTS). These standards are aimed at specifying the criteria for establishing and assessing the effectiveness of investment firms' order execution policies. Article 1(4)(e) of the MiFID II review outlines the requirements for these RTS, emphasizing the need for clarity, transparency, and robust compliance mechanisms.

Key Areas of Focus in the Consultation Paper

The consultation paper released by ESMA seeks input on several critical aspects of order execution policies to address the identified shortcomings and enhance the overall regulatory framework. These key areas include:

Establishment of Order Execution Policy: The paper invites input on the classification of financial instruments in which firms execute client orders and the initial selection of venues for the order execution policy. This involves defining clear and specific criteria for categorising financial instruments and selecting execution venues that can consistently deliver the best results for clients.

Monitoring and Assessing Effectiveness: Investment firms are required to implement robust procedures for monitoring and regularly assessing the effectiveness of their order execution arrangements and policies. This includes continuous evaluation of execution outcomes, periodic reviews, and updates to the policies based on performance metrics and market developments. The goal is to ensure that the execution policies remain effective and aligned with regulatory requirements.

Execution through Own Account Dealing: The consultation addresses how firms execute client orders through own account dealing, emphasising the need for clear and transparent practices. Firms must manage potential conflicts of interest and ensure fair treatment of clients when dealing on their own account. This involves stringent compliance with regulatory standards and thorough documentation of the execution processes.

Handling Client Instructions: The consultation explores how investment firms should handle specific client instructions, ensuring that these instructions are executed in line with the firm's policies and in the best interest of the clients. Firms must define clear procedures for dealing with specific instructions and ensure that these are consistently applied and well-documented.

MiFID II Regulation: Key Elements of the Draft RTS

Categorization of Financial Instrument Classes

The draft Regulatory Technical Standards (RTS) under MiFID II Regulation emphasize a meticulously structured methodology for categorising financial instruments. This categorisation is pivotal for the effective establishment of order execution policies, ensuring that firms can achieve the best execution outcomes for their clients.

ISO Standard 10962 Groups

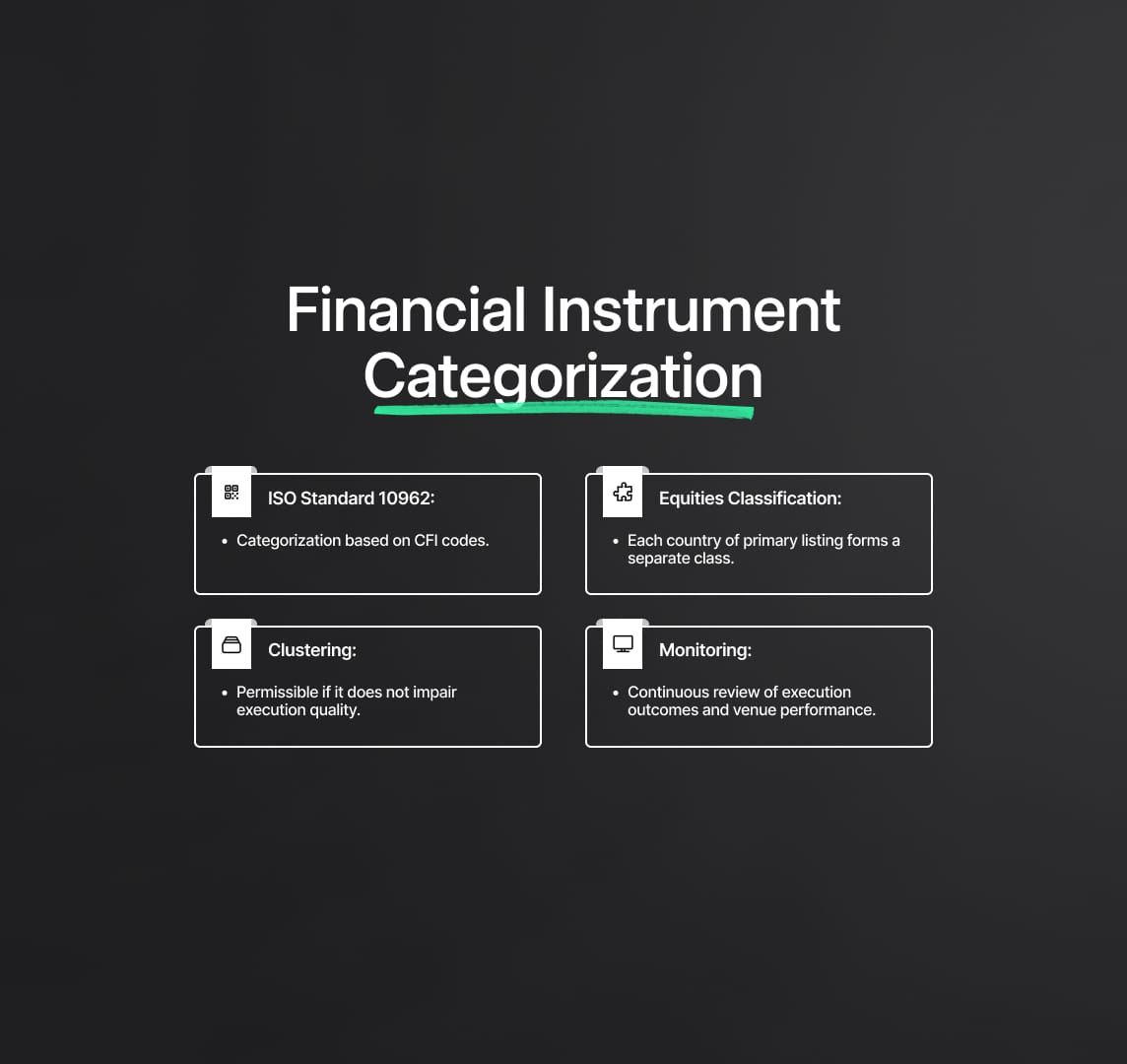

Investment firms are required to categorise financial instruments based on the instrument groups defined by the first two letters of the Classification of Financial Instruments (CFI) code, as stipulated under ISO Standard 10962. This classification system provides a standardized approach, enhancing the consistency and comparability of data across different firms and markets.

Equities Classification

For equities (denoted as E--—*), the draft RTS propose that each country of primary listing should constitute a separate class of financial instruments. This ensures that execution policies can be tailored to the specific market dynamics and regulatory environments of different countries, thereby improving the precision and effectiveness of execution strategies.

Clustering of Classes

The RTS also allow for the clustering of several classes of instruments into a single class if the number of orders is relatively low. However, this clustering is permissible only if it does not impair the firm's ability to achieve the best possible result for its clients. This flexibility helps smaller firms manage their resources more efficiently while still adhering to the best execution principles.

Alternatively, the RTS propose using a fixed list of financial instrument classes, potentially based on MiFID II RTS 1 and RTS 27 classifications. This alternative approach includes:

- Separate Classes for Shares: Each country of primary listing for company shares forms a distinct class.

- Grouping Other Instruments: Other financial instruments are grouped into approximately 15-20 classes.

- Allowing Clustering: Similar clustering of classes is permitted if it does not compromise the quality of execution.

MiFID II RTS: Establishing Effective Order Execution Policies

Investment firms must pre-select execution venues that consistently deliver the best possible results for client orders. The draft RTS outline several key requirements to ensure that firms can identify and utilize the most effective venues.

Venue Pre-Selection Criteria

Firms should pre-select venues based on criteria that allow for a meaningful assessment of their ability to achieve the best possible result for clients. These criteria should include factors such as price, costs, speed, and the likelihood of execution and settlement. The aim is to ensure that firms select venues that offer the optimal conditions for executing orders, thereby maximizing the benefits for clients.

Comprehensive List of Venues

Firms must establish and maintain an updated list of authorised venues for client order execution. This list should include detailed internal approval information, such as the approval date, the approver's name and capacity, the classes of financial instruments each venue can handle, and the client categories each venue can serve. This comprehensive documentation ensures transparency and accountability in the venue selection process.

Monitoring and Updating Execution Policies

To ensure continuous compliance and effectiveness, firms must regularly monitor and update their execution policies. The draft RTS outline several key requirements for maintaining robust execution strategies.

Continuous Monitoring

Firms must set out the frequency and methodology for continuous or periodic monitoring in their execution policies. This involves regularly reviewing execution performance to ensure that it aligns with the firm's best execution obligations. The frequency of these reviews should be sufficient to capture significant changes in market conditions and execution quality.

Performance Assessment

Firms should assess all transactions or a representative sample per class of financial instruments. This assessment should include evaluating key performance metrics such as execution price, costs, and speed. Performance metrics should trigger reviews when certain thresholds are breached, indicating potential issues with the execution quality. This proactive approach helps firms identify and address problems before they impact clients.

Use of Third Parties

Firms may rely on third-party monitoring, such as independent data providers, to enhance the robustness of their performance assessments. However, it is crucial that firms ensure these third-party processes are thoroughly assessed and representative of the firm's client base. This means that the data and insights provided by third parties should accurately reflect the characteristics and needs of the firm's clients, ensuring that the execution policies remain effective and aligned with regulatory requirements.

MiFID II Regulation: Specific Criteria for Execution Venue Selection

Under the MiFID II Regulation, investment firms are required to specify detailed criteria for selecting execution venues to ensure they consistently achieve the best possible results for their clients. This section of the draft Regulatory Technical Standards (RTS) delves into the obligatory and discretionary factors that must be considered, the use of automatic order routing systems, and the need for regular reviews and adjustments to the execution policies.

Obligatory and Discretionary Factors

When executing client orders, firms must establish and adhere to specific criteria for selecting execution venues. These criteria must be tailored for each class of financial instruments and should address both retail and professional clients. The factors to be considered include:

- All Costs Directly Related to Order Execution: This encompasses not only the explicit costs such as fees and commissions charged by the execution venue but also implicit costs like market impact and opportunity costs. Firms must ensure they consider the total cost of executing an order when selecting venues.

- Real-Time Market or Historical Data: Firms need to leverage both real-time market data and historical performance data to evaluate the effectiveness of different venues. Real-time data helps in making immediate execution decisions, while historical data provides insights into the long-term performance and reliability of venues.

- Characteristics of the Order: The specific attributes of each order, such as its size and nature, must be considered. Larger orders might require venues with deeper liquidity to minimize market impact, whereas smaller orders might be executed more efficiently on venues with lower transaction costs.

Automatic Order Routing Systems

For firms using automatic order routing systems, the draft RTS mandates a thorough documentation of these systems' characteristics in the execution policy. Key requirements include:

- System Characteristics: Firms must describe the main features of their automatic order routing systems, including the algorithms used for order routing, the criteria for selecting execution venues, and any safeguards in place to prevent adverse impacts on execution quality.

- Transparency and Accountability: The execution policy should provide detailed information on how the routing system operates, ensuring transparency for clients and regulators. This includes disclosing how the system prioritizes different factors such as speed, cost, and likelihood of execution.

Regular Reviews and Adjustments

To maintain the effectiveness of their execution policies, firms are required to conduct regular reviews and adjustments. This ongoing evaluation process includes:

- Annual Assessments: Firms must perform at least annual assessments of their selected venues and execution arrangements. These assessments should involve a comprehensive review of performance metrics and adherence to best execution standards.

- Event-Driven Reviews: In addition to annual assessments, firms must conduct reviews whenever there are significant events or material changes that could impact execution quality. Examples include major market disruptions, changes in venue performance, or regulatory updates.

- Update Policies: Based on the findings from these reviews, firms must update their execution policies and arrangements promptly, but no later than three months after the review. This ensures that the policies remain current and effective in achieving the best execution for clients.

- Detailed Analysis: Reviews should include a detailed comparison of the prices obtained for client orders against a reference dataset. This analysis helps firms identify any discrepancies or areas for improvement, ensuring that execution policies are fine-tuned to deliver optimal results.

Client Instructions and Own Account Dealing

MiFID II Regulation allows clients to provide specific instructions regarding the execution of their orders. The draft RTS outlines how firms should manage these instructions to ensure compliance and best execution:

Handling Specific Client Instructions

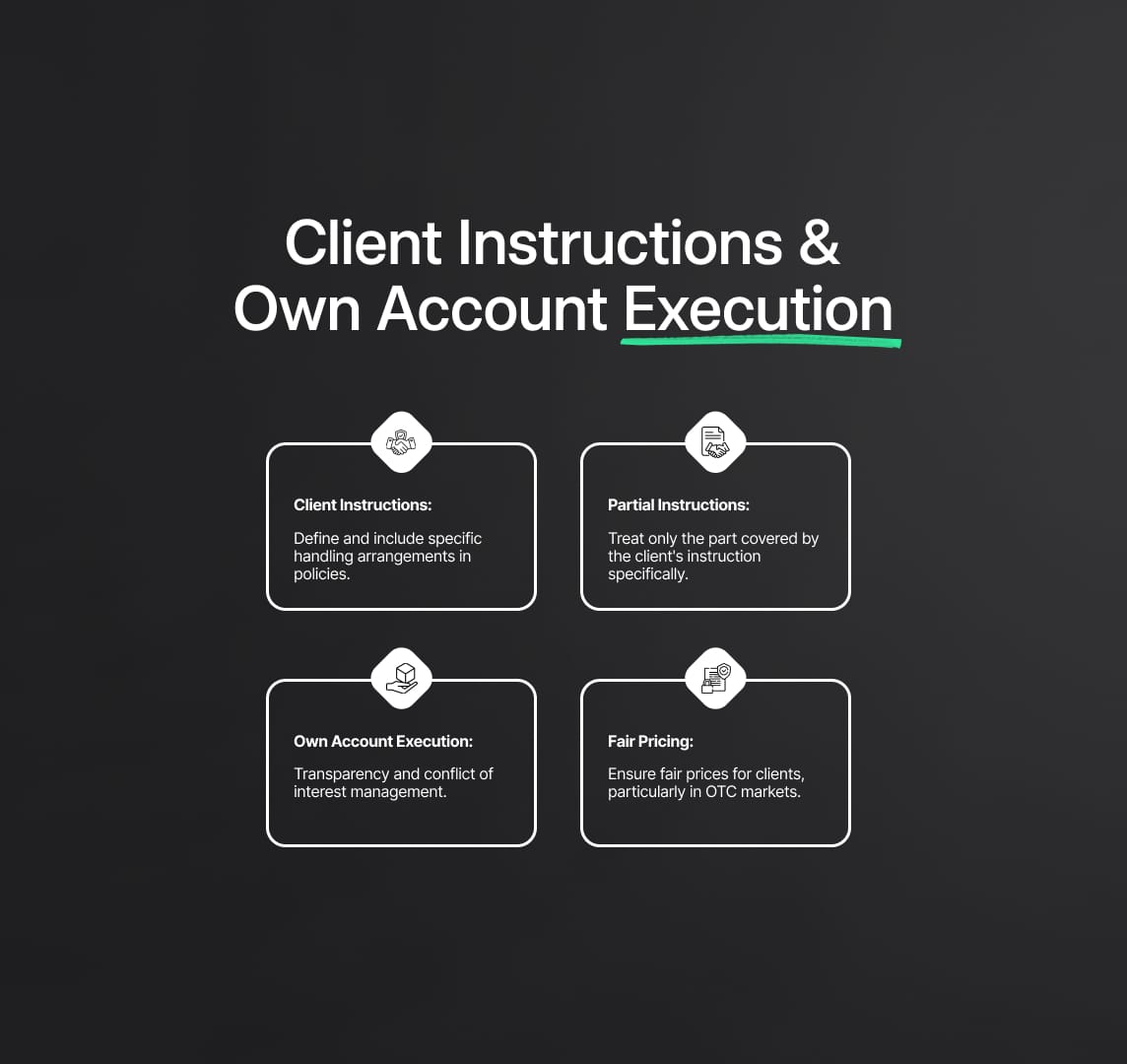

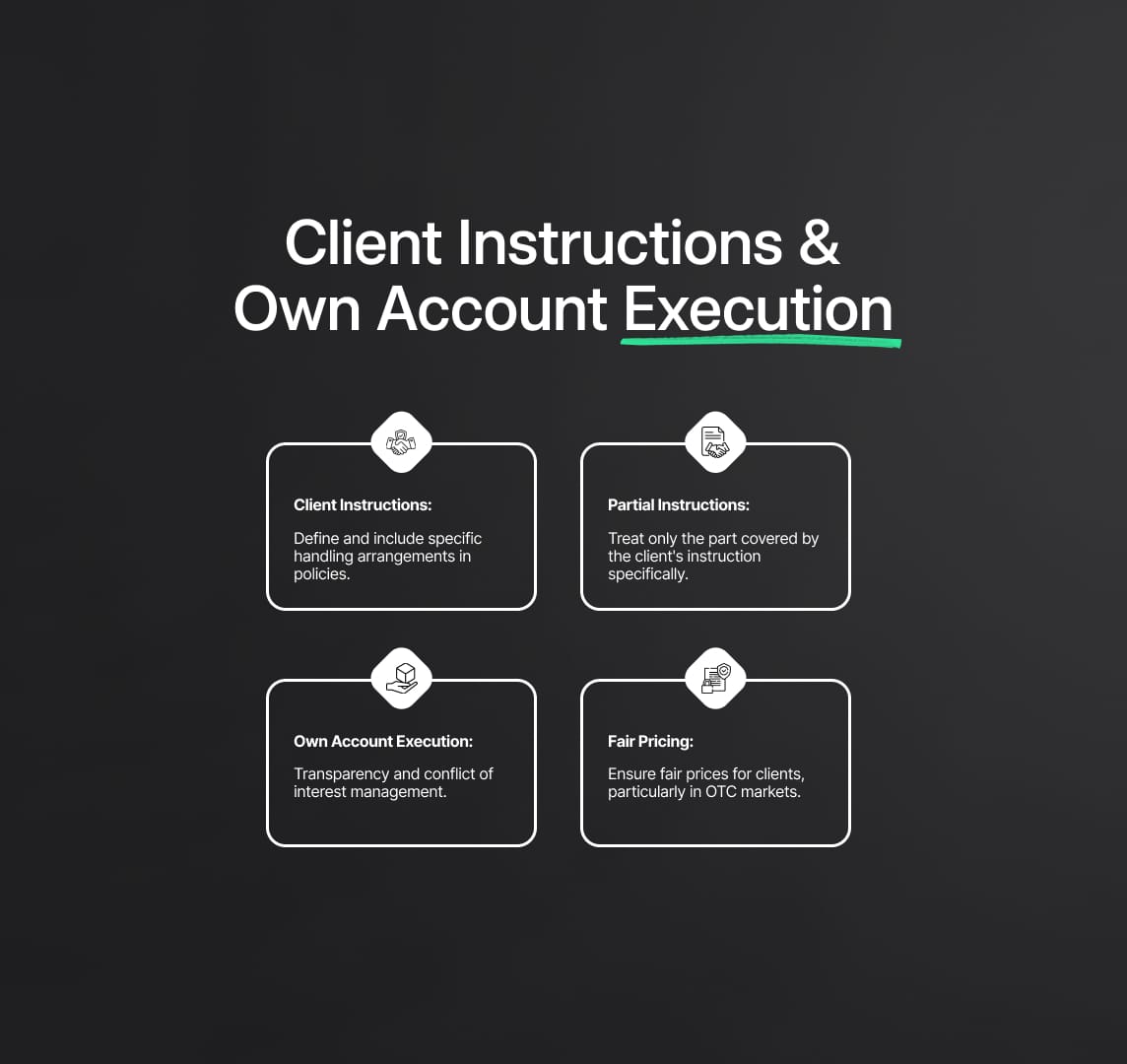

- Policy Inclusions: Firms must clearly specify in their order execution policies how they will handle specific instructions from clients. This includes detailing the impact of these instructions on the selection of execution venues and the steps taken to achieve the best possible result.

- Defining Instructions: Specific instructions involve clients choosing from multiple options provided by the firm or instructing the firm to handle the order differently than outlined in the policy. Firms must define these scenarios clearly to avoid any ambiguity.

- Processing Orders: Only the part of the order that is explicitly covered by the client's instruction is treated as such; the remaining parts must follow the general execution policy to ensure overall compliance with best execution requirements.

Execution on Own Account

- Policy Requirements: Firms must explicitly state in their execution policies if they execute client orders on their own account. This practice must be justified to ensure it provides the best possible result for clients.

- Conflict of Interest Management: Firms must implement robust procedures to identify, prevent, and manage conflicts of interest that may arise from executing orders on their own account. This includes ensuring transparency and fairness in all dealings.

- Price Fairness: In accordance with Article 64(4) of Commission Delegated Regulation (EU) 2017/565, firms must ensure that the prices proposed to clients are fair, particularly when dealing in over-the-counter (OTC) products. This involves having systematic and robust checks in place to validate the fairness of prices.

MiFID II Regulation: ESMA’s Consultation and Stakeholder Feedback

The European Securities and Markets Authority (ESMA) has engaged in extensive public consultations to refine the draft Regulatory Technical Standards (RTS) under MiFID II Regulation. This collaborative approach is critical for ensuring that the proposed standards are not only robust and practical but also aligned with the evolving needs of the market. By seeking input from the Securities and Markets Stakeholder Group and analyzing potential costs and benefits, ESMA aims to create a comprehensive and effective regulatory framework.

Detailed Breakdown of Specific Proposals

The draft RTS outlines specific criteria and methodologies for selecting execution venues, ensuring continuous monitoring and review of execution policies, and handling client instructions. These detailed proposals are designed to enhance the transparency, effectiveness, and compliance of investment firms' order execution policies under MiFID II Regulation.

Specific Criteria for Execution Venue Selection

Investment firms must establish rigorous criteria for selecting execution venues to ensure they consistently achieve the best possible results for their clients. The draft RTS specifies both obligatory and discretionary factors that firms need to consider:

- Authorized Venues: Firms should select venues that are authorized by national competent authorities or recognized third-country authorities. This ensures that the venues meet regulatory standards and provide a secure environment for order execution.

- Internal Governance: The selection process must comply with the firm's internal governance procedures. This includes obtaining necessary approvals and documenting the decision-making process to ensure accountability and transparency.

- Updated Lists: Firms must maintain an up-to-date list of approved execution venues, including detailed information about each venue, such as the types of financial instruments they handle, their operational characteristics, and any specific conditions or limitations.

Monitoring and Reviewing Execution Policies

To maintain continuous compliance and effectiveness of their order execution policies, firms must implement robust monitoring and review processes. The draft RTS outlines several key requirements:

- Continuous Monitoring: Firms must define the frequency and methodology for continuous or periodic monitoring within their execution policies. This involves regularly evaluating the performance of execution venues to ensure they deliver the best possible outcomes for clients.

- Performance Metrics: Firms should assess all transactions or a representative sample per class of financial instruments. Performance metrics, such as execution prices, transaction costs, and speed of execution, should be used to trigger reviews when certain thresholds are breached.

- Event-Driven Reviews: Firms must initiate reviews of their execution policies whenever significant events or material changes occur. Examples include market disruptions, changes in venue performance, or updates in regulatory requirements. These reviews ensure that the policies remain relevant and effective under changing market conditions.

Client Instructions and Order Handling

Handling specific client instructions is a critical aspect of ensuring best execution under MiFID II Regulation. The draft RTS provides detailed guidelines on how firms should manage these instructions:

- Defining Instructions: Firms must clearly define what constitutes a specific client instruction. This involves detailing the scenarios where clients can provide specific instructions and the implications of these instructions on the execution process.

- Policy Inclusion: Execution policies must include arrangements for handling specific instructions from clients. This ensures that firms are prepared to manage these instructions in a manner that aligns with their best execution obligations.

- Partial Instructions: When a client provides a specific instruction for part of an order, only that part should be treated according to the instruction. The remainder of the order must be executed according to the firm's general execution policy to ensure overall compliance with best execution standards.

Compliance with Own Account Execution

Executing client orders on the firm's own account requires careful management to avoid conflicts of interest and ensure fair treatment of clients. The draft RTS specifies several requirements for firms engaging in own account execution:

- Explicit Policy Statements: Firms must clearly state in their execution policies if they engage in own account execution. This transparency helps clients understand the firm's practices and potential conflicts of interest.

- Conflict Management: Firms must implement robust procedures to identify, prevent, and manage conflicts of interest related to own account execution. This includes ensuring that clients receive fair and unbiased treatment.

- Fair Pricing Compliance: Firms must ensure that the prices offered to clients in own account transactions are fair. This involves conducting systematic and robust checks to validate the fairness of prices, particularly in over-the-counter (OTC) markets, in accordance with Article 64(4) of Commission Delegated Regulation (EU) 2017/565.

Reduce your

compliance risks