MiFIR Regulation: RTS 22 and RTS 24 Updates

ESMA's MiFIR Regulation updates to RTS 22 and RTS 24 enhance data reporting, align with EMIR and SFTR, and integrate Distributed Ledger Technology (DLT) for improved market transparency.

The Markets in Financial Instruments Regulation (MiFIR) is a cornerstone of financial market regulation within the European Union (EU), aimed at ensuring market transparency, investor protection, and the integrity of financial transactions. On 3 October 2024, the European Securities and Markets Authority (ESMA) published a significant consultation paper as part of its review of Regulatory Technical Standard 22 (RTS 22) and RTS 24 under the MiFIR Regulation. This consultation paper marks a pivotal moment in refining transaction and order book data reporting under Articles 26 and 25 of the MiFIR Regulation, which were updated with the revised text that entered into force on 28 March 2024.

The revisions to the MiFIR Regulation are not merely administrative but represent a critical evolution in how the EU’s financial market regulations will operate, particularly in a landscape influenced by digital transformation, financial innovation, and increased cross-border market activities. This article provides a technical and detailed overview of these proposed changes to RTS 22 and RTS 24, their underlying principles, and the potential impact on market participants.

Source

[1]

[2]

MiFIR Regulation and its 2024 Amendments

The MiFIR Regulation, along with the Markets in Financial Instruments Directive (MiFID II), forms the legislative framework regulating financial markets in the EU. While MiFID II governs market structures and investor protection, the MiFIR Regulation primarily deals with the transparency and reporting of financial transactions. Together, these regulations ensure the EU's financial markets are efficient, transparent, and resilient.

In 2024, the MiFIR Regulation underwent amendments, primarily affecting Articles 25 and 26, which govern the maintenance of order book data and transaction reporting, respectively. These changes mandated ESMA to revisit and revise the existing technical standards, particularly RTS 22 and RTS 24, to better align them with current market practices, technological advancements, and international reporting standards.

Amendments to RTS 22: Transaction Data Reporting Under Article 26 of MiFIR Regulation

RTS 22 outlines the transaction reporting obligations for market participants under the MiFIR Regulation. The changes proposed by ESMA reflect the need for enhanced granularity, better identification of transactions, and alignment with other global reporting frameworks. Below are the primary areas addressed in the consultation paper.

1. Determination of Relevant Competent Authority (RCA)

A critical aspect of transaction reporting under the MiFIR Regulation is identifying the competent authority responsible for supervising a transaction. ESMA proposes refinements in the rules to determine the most relevant market in terms of liquidity (MRMTL). This is essential because the RCA impacts which regulatory body oversees reporting accuracy and market surveillance.

According to the revised Article 26 of the MiFIR Regulation, NCAs (National Competent Authorities) will be responsible for not only ensuring that transaction reports are submitted by investment firms but also for forwarding them to the competent authorities of the most relevant market in terms of liquidity. This expanded responsibility ensures that reports for all financial instruments are submitted to the correct regulatory body, based on the liquidity of the market in which they are traded. These criteria help align the competent authority's supervision with the location of the most significant trading activity, making it easier to detect any market abuse.

For example, in the case of cross-border transactions involving derivatives, these new determination rules are critical in identifying the RCA. If a derivative product is traded primarily in one EU jurisdiction, that market's competent authority will oversee the reporting, even if the transaction is executed across multiple venues.

2. New Fields for Transaction Reporting under MiFIR Regulation

ESMA’s amendments introduce several new fields to improve the precision of transaction data under the MiFIR Regulation:

- Transaction Effective Date: This field captures the date when a transaction becomes legally effective, enhancing the clarity of reporting timelines and obligations. For derivatives, such as interest rate swaps with forward start dates, this new field ensures regulators can track when the financial obligation becomes binding. This is particularly important for complex derivative products that have staggered execution and settlement dates, such as credit default swaps (CDS) or interest rate derivatives (IRD), where the transaction may not settle immediately but obligations commence at a future date.

- Reporting Obligation Entity: This field identifies the entity responsible for the reporting obligation under the MiFIR Regulation, which provides additional transparency. In cases where a transaction involves multiple intermediaries, the responsible entity—such as a fund manager or portfolio manager—must be clearly identified, thereby reducing ambiguity regarding the reporting party.

For example, in securities lending transactions, the entity managing the lending side of the transaction must now be explicitly stated, allowing regulators to track the parties responsible for compliance.

3. Enhanced Use of Identifiers

Transaction identifiers are set to undergo changes under the MiFIR Regulation to improve the linking of related transactions. Key updates include:

- Trading Venue Transaction Identification Code (TVTIC): Under the revised RTS 22 of the MiFIR Regulation, the TVTIC is required for all on-venue transactions to track executions more accurately. This code ensures that regulators can link large block trades or aggregated orders executed on multiple venues. Additionally, off-venue transactions will also require a similar transaction identifier to ensure complete traceability.

Real-world example: When an equity trade is executed on a primary market and then reported across several other venues, the TVTIC will ensure that regulators can track the trade from its initiation to completion, providing a clearer understanding of liquidity flows and potential market manipulation.

The proposed use of Identifiers aligns RTS 22 under the MiFIR Regulation with global standards such as the Legal Entity Identifier (LEI) system and the International Securities Identification Number (ISIN), ensuring consistency across reporting frameworks like EMIR and SFTR. This reduces the possibility of data fragmentation, as firms operating across multiple jurisdictions must now report using uniform identifiers.

4. Alignment with Other Regulatory Frameworks under MiFIR Regulation

ESMA's objective of harmonizing transaction reporting under the MiFIR Regulation with frameworks like EMIR (European Market Infrastructure Regulation) and SFTR (Securities Financing Transactions Regulation) ensures that firms no longer face redundant reporting obligations across different EU regulations. By standardizing data fields between the MiFIR Regulation and these other regulations, ESMA reduces the operational complexity for firms subject to multiple regulatory regimes.

For example, EMIR focuses on OTC derivatives reporting, while SFTR deals with securities financing transactions. MiFIR’s alignment with these frameworks, particularly in terms of data fields for trade reporting, ensures that firms engaged in cross-product transactions can benefit from a unified reporting process, thus reducing the administrative burden.

5. Distributed Ledger Technology (DLT) Integration under MiFIR Regulation

Recognizing the growing adoption of Distributed Ledger Technology (DLT), ESMA proposes incorporating DLT financial instruments within the scope of Article 26 of the MiFIR Regulation. For example, DLT-based securities—such as tokenized bonds or equity—are becoming more prevalent in financial markets. Under the revised RTS 22, transactions involving these instruments will be reported just like traditional financial instruments, ensuring comprehensive regulatory oversight and market transparency.

This amendment is particularly relevant as the EU moves toward the European Digital Finance Strategy, which includes regulatory initiatives designed to facilitate the use of DLT in financial services. By integrating DLT transactions into the MiFIR Regulation framework, ESMA ensures that innovations such as smart contracts and digital asset exchanges are subject to the same reporting standards as traditional financial transactions.

6. Improved Data Quality and Reporting Efficiency under MiFIR Regulation

The proposed amendments aim to enhance overall quality and efficiency of transaction reporting under the MiFIR Regulation by reducing errors and improving the reliability of transaction data for regulatory supervision. The use of standardized data fields across different EU regulations (such as MiFIR, EMIR, and SFTR) ensures that firms can benefit from a simplified reporting process, thus improving the accuracy and completeness of reported data.

For example, the new field alignment between the MiFIR Regulation and SFTR ensures that repo transactions and other securities financing agreements are consistently reported, which improves the quality of data collected by NCAs and the European Central Bank (ECB) for use in market surveillance and systemic risk assessments.

Amendments to RTS 24: Order Book Data Maintenance Under Article 25 of MiFIR Regulation

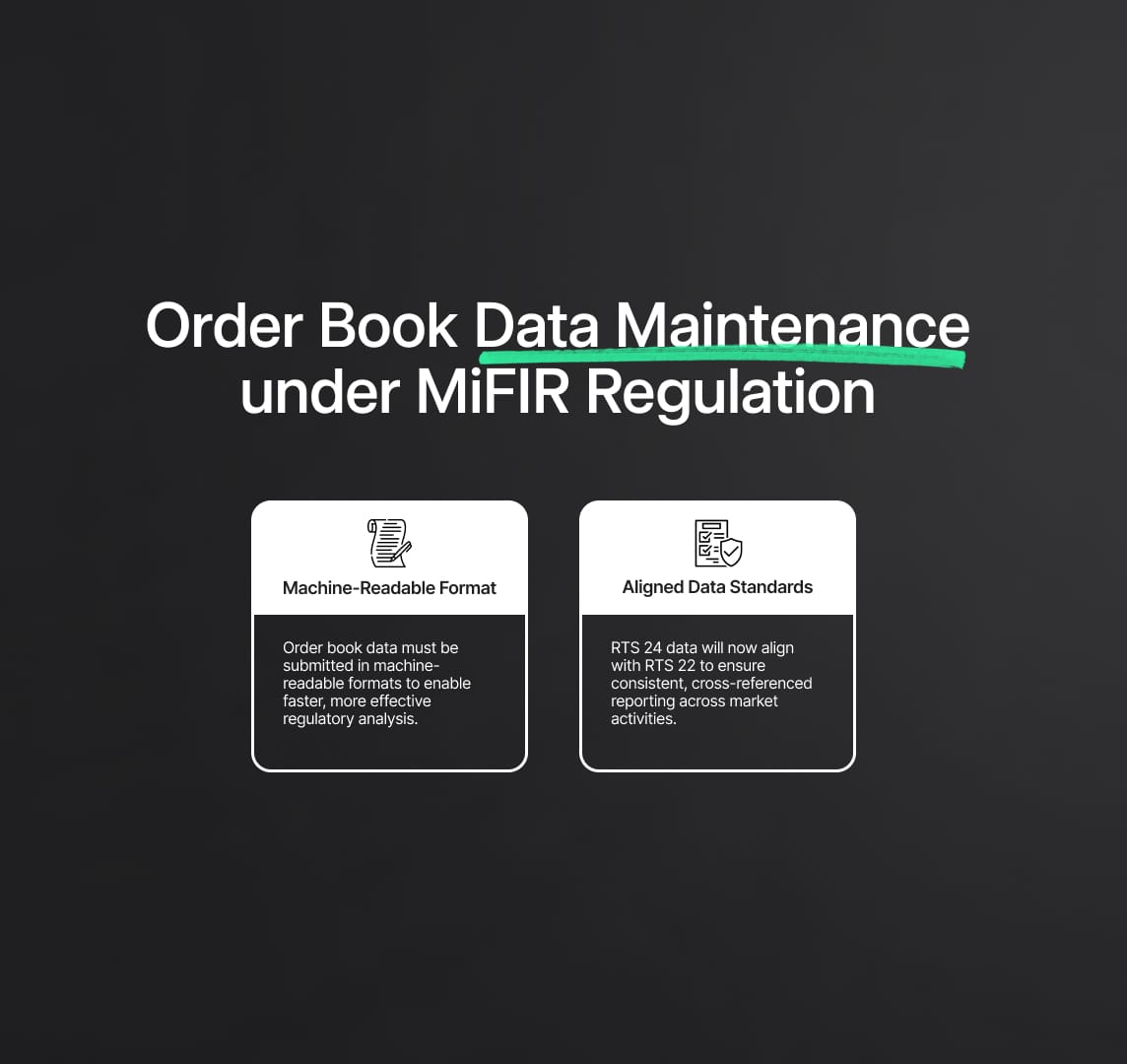

RTS 24 regulates how investment firms maintain and report order book data under the MiFIR Regulation. In light of technological advances, ESMA’s proposals focus on improving data accessibility and ensuring that order book data is maintained in a machine-readable format.

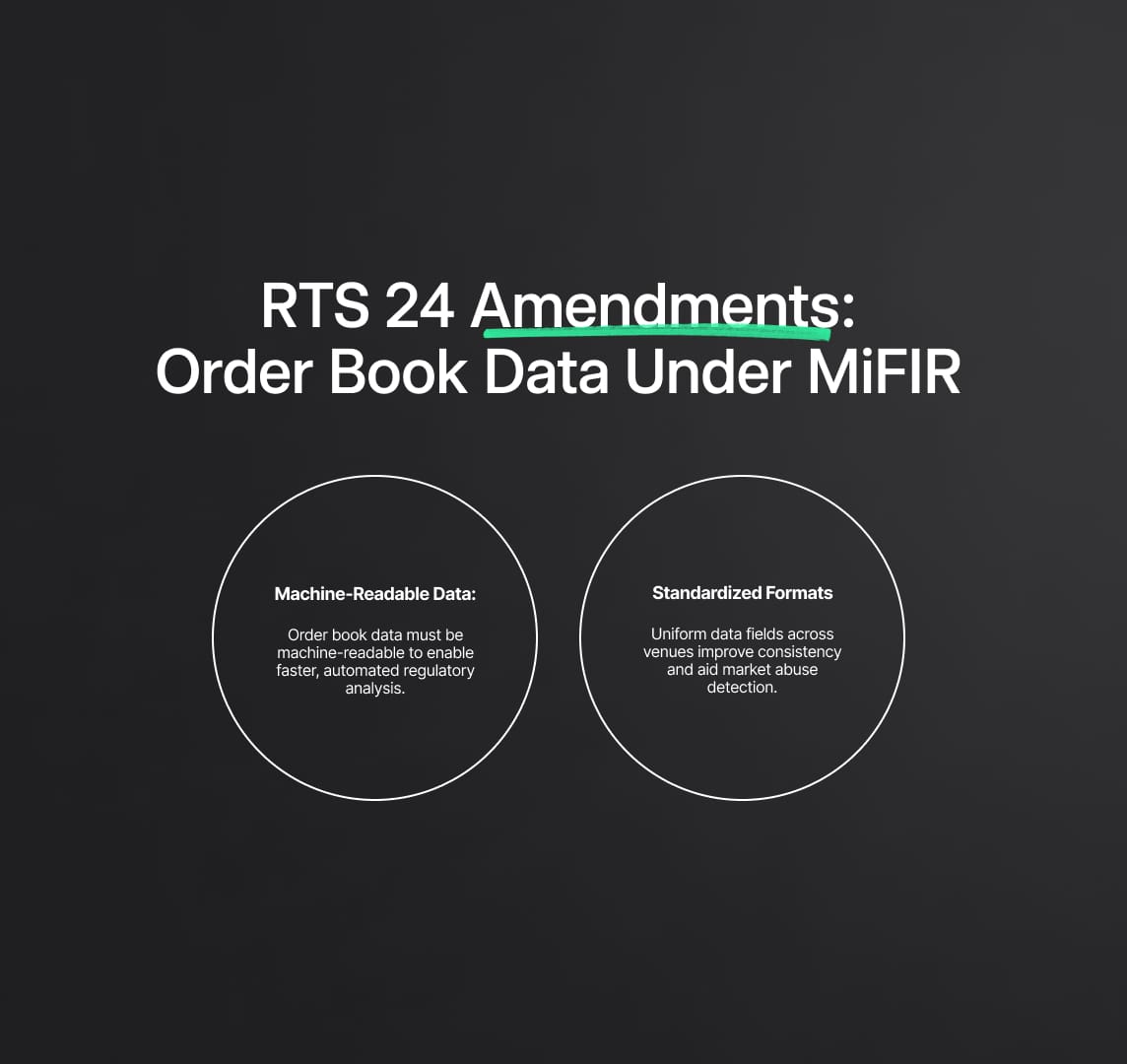

1. Machine-Readable Format under MiFIR Regulation

A significant change in RTS 24 under the MiFIR Regulation is the requirement that order book data be maintained in a machine-readable format. The shift from traditional, manual data formats to automated digital systems ensures that regulatory authorities can process large datasets more effectively, reducing the risk of errors and improving market oversight.

This change aligns with global trends in RegTech, where large datasets are increasingly processed through automated systems. For instance, the adoption of XML and JSON data formats under the ISO 20022 standard will streamline the transmission and analysis of order book data, providing NCAs with near real-time insights into market movements.

Real-world Example: When a market experiences high-frequency trading activity, regulators can utilize the machine-readable format to swiftly analyze order flows, detect potential market manipulation, and assess overall market stability.

2. Enhancing Data Consistency

The amendments to RTS 24 under the MiFIR Regulation also aim to standardize the fields and formats used for order book data across different venues and market participants. This consistency will facilitate easier comparison of market activity between different trading venues, allowing regulators to perform more effective market surveillance.

For instance, a uniform data format across regulated markets and multilateral trading facilities (MTFs) will enable regulatory bodies to reconstruct historical order books in the event of market abuse investigations.

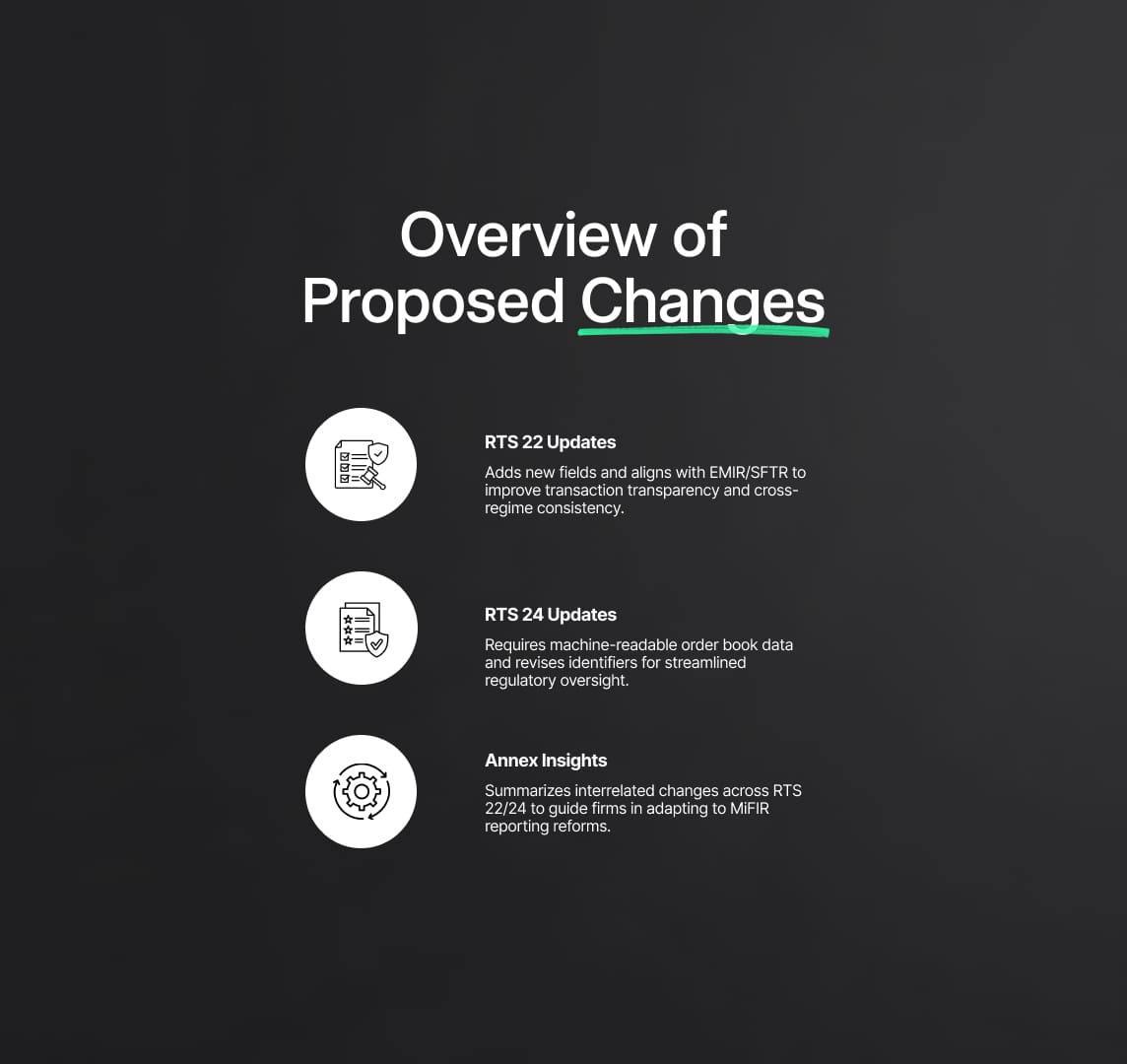

Annexes: A Consolidated Overview of Proposed Changes

The consultation paper provides a detailed examination of the proposed changes to both RTS 22 and RTS 24 under the MiFIR Regulation, with specific emphasis on the implications for transaction data reporting and order book data maintenance. These annexes serve as a comprehensive resource that outlines how these changes interrelate, providing crucial insights into the rationale behind each amendment.

For RTS 22, the annexes detail key revisions that include:

- New fields added to capture more granular transaction information, such as the Transaction Effective Date and new entity identifiers. These fields aim to enhance transparency and accountability by ensuring every party involved in the transaction is clearly identified.

- Alignment with international standards like EMIR and SFTR, reducing discrepancies across reporting regimes and ensuring that the data collected is more consistent and comparable across different jurisdictions.

For RTS 24, the annexes address:

- The shift to a machine-readable format for order book data, which will enable more efficient regulatory oversight and data processing.

- New fields and amendments designed to streamline the collection of order book data, including specific updates to existing identifiers to ensure consistency with changes introduced in RTS 22.

These annexes are crucial for financial institutions as they provide a consolidated view of the upcoming regulatory landscape under MiFIR Regulation. Firms must carefully review these annexes to ensure their systems and processes are aligned with the new reporting requirements, especially considering the technical complexity introduced by Distributed Ledger Technology (DLT) and cross-framework alignment efforts.

Next Steps in the MiFIR Regulation Revision Process

The MiFIR Regulation consultation period provides an opportunity for stakeholders to contribute feedback before the final standards are implemented. The deadline for comments is set for 3 January 2025, giving industry participants a window to address concerns or propose alternative solutions to the proposed changes.

Following this consultation phase, ESMA will carefully evaluate the feedback and incorporate it into a final report, which will be published and submitted to the European Commission for approval in Q1 2025. Once endorsed, the revised RTS 22 and RTS 24 standards under the MiFIR Regulation will become enforceable, introducing a new layer of complexity and transparency to the EU’s financial reporting framework.

Impact on Transaction Reporting

The changes proposed in RTS 22—which governs the reporting of financial transactions—are extensive and target several critical areas. These changes are designed to enhance the accuracy and completeness of transaction reporting, ensuring that the data collected by National Competent Authorities (NCAs) is robust enough to support comprehensive market oversight and mitigate risks.

Real-world implications of the amendments include:

- Increased scope for reporting derivatives: New requirements mean that Over-the-Counter (OTC) derivatives such as Interest Rate Swaps (IRS) and Credit Default Swaps (CDS) will need to be reported with more precision, especially for transactions involving systemically important financial institutions. This change is particularly relevant for derivatives linked to global indices or benchmarks.

- Use of new identifiers: The introduction of identifiers like the Trading Venue Transaction Identification Code (TVTIC) will streamline the linking of complex trades executed across multiple venues. For example, a block trade initiated on one exchange but executed across several others will now be easier to track from initiation to completion.

Enhancements in Order Book Data Maintenance under MiFIR Regulation

The amendments to RTS 24, which covers how investment firms and trading venues maintain order book data, reflect a growing emphasis on the digitization and automation of regulatory processes. This aligns with the broader goals of the MiFIR Regulation to promote transparency and reduce the risk of market manipulation.

The key enhancements to RTS 24 include:

- Mandatory machine-readable formats: Investment firms and trading venues will now need to ensure that their order book data is submitted in a format that allows for seamless electronic processing. This will enhance the ability of regulators to quickly identify patterns of misconduct, such as market manipulation or insider trading.

- Improved data consistency: With the amendments, data collected under RTS 24 will now align more closely with transaction data reported under RTS 22. This will ensure that order book data, which details the bids, offers, and other market orders, can be effectively cross-referenced with transaction reports.

These enhancements are critical for maintaining the integrity of the EU’s financial markets, especially in light of the increasing role that high-frequency trading (HFT) and other automated trading strategies play in modern finance.

MiFIR Regulatory Implications

The proposed changes to MiFIR Regulation have significant implications for financial institutions, particularly in terms of compliance and operational adjustments. For instance, firms involved in securities lending or derivatives trading will need to update their systems to accommodate the new reporting fields, such as those capturing Transaction Effective Dates or new aggregated order identifiers.

Additionally, the integration of Distributed Ledger Technology (DLT) into financial markets presents both challenges and opportunities. The proposed regulatory amendments ensure that DLT-based financial instruments, such as tokenized securities, are subject to the same rigorous reporting standards as traditional assets. This ensures that the benefits of blockchain technology—such as improved transparency and security—are fully realized within the EU’s regulatory framework.

In practice, firms operating in the DLT space will need to ensure that their reporting systems can capture and transmit the necessary data, including details of smart contracts and digital token identifiers (DTIs). This is particularly relevant for financial institutions exploring tokenized bonds or equity offerings, as the new reporting standards will require these transactions to be reported with the same level of detail as traditional financial instruments.

Reduce your

compliance risks