CRR3 and CRD6: EBA's Centralised Pillar 3 Data Hub

The EBA's Pillar 3 data hub under CRR3 and CRD6 introduces centralized prudential disclosures, new IT submission standards, and enhanced data validation to boost transparency and regulatory oversight across EU financial institutions.

On 11 October 2024, the European Banking Authority (EBA) launched a critical consultation on the creation of a Pillar 3 data hub. This development is part of the broader regulatory framework under the Capital Requirements Regulation (CRR3) and Capital Requirements Directive (CRD6), which aims to significantly enhance the transparency and accessibility of prudential disclosures within the European Union. The consultation outlines the technical standards and IT solutions that financial institutions, especially large ones, must adopt when publishing their Pillar 3 disclosures. This article provides an in-depth look into the technical aspects of these updates, focusing on their alignment with CRR3, CRD6, and the EBA's centralized data hub for disclosures.

CRR3 and CRD6

The Capital Requirements Regulation (CRR3) and Capital Requirements Directive (CRD6) are the most recent updates to the EU’s regulatory framework for banking institutions. These updates build on the earlier CRR2 and CRD5 regulations and are closely aligned with the Basel III reforms, which seek to bolster the banking sector's resilience and risk management practices. While CRR3 directly applies across the EU, CRD6 offers directives that member states must implement through national legislation.

CRR3: Changes and Pillar 3 Disclosures

One of the major updates in CRR3 is the enhancement of prudential disclosure requirements, specifically outlined in Articles 434 and 434a. These articles mandate that the EBA must centralize all prudential disclosures, making them readily accessible to the public through a unified electronic access point on its website. The objective of this centralization is to increase transparency, ensuring that stakeholders such as investors, regulators, and the public can easily access consistent and comparable data regarding the financial health and risk profiles of banks.

The Pillar 3 disclosure framework under CRR3 builds on the Basel III Pillar 3 requirements. It is designed to enhance market discipline through mandatory disclosure of key metrics such as capital adequacy, liquidity coverage ratios, and leverage ratios. In addition, CRR3 reinforces the Large Exposures Framework and introduces measures to improve the transparency of risk-weighted assets (RWAs), which will require institutions to report more detailed data about their internal models and the outcomes of stress tests.

The EBA Pillar 3 data hub project is central to this disclosure mandate. According to the EBA's proposal, the data hub will allow for uniform submission of Pillar 3 data by institutions, utilizing standardized IT processes and data exchange formats. The hub will facilitate not only the collection of disclosures but also their validation and dissemination in a machine-readable format, making it easier for stakeholders to download and analyze the data.

CRD6: Empowering National Regulators

The Capital Requirements Directive (CRD6) complements CRR3 by providing a framework for national regulatory authorities. Article 106 of CRD6 empowers these authorities to require more frequent disclosures than the minimum standards set by CRR3. It also gives them the authority to set deadlines and require institutions to publish disclosures using specific media or platforms, in addition to the centralized platform on the EBA’s website. This flexibility allows national regulators to respond more dynamically to emerging risks and ensure that disclosures meet the specific needs of local markets.

CRD6 further mandates that regulators can set out requirements regarding the frequency of disclosures, which may be necessary in times of financial instability or market volatility. This allows for greater oversight and quicker response times, ensuring that market participants are kept informed of any significant changes to an institution's risk profile or capital adequacy. Additionally, the CRD6 empowers competent authorities to enforce stringent deadlines for submission of prudential data and offers them the ability to impose penalties for non-compliance.

Together, CRR3 and CRD6 aim to foster a more resilient and transparent banking sector across the EU, ensuring that all stakeholders have access to reliable and standardized information. By centralizing prudential disclosures through the Pillar 3 data hub, the EBA is enabling a more streamlined and efficient process for the dissemination of critical financial data, while CRD6 grants regulators the flexibility to impose stricter disclosure requirements when necessary.

This combined framework also emphasizes supervisory convergence across the EU, ensuring that financial institutions, regardless of their jurisdiction, are subject to the same prudential reporting standards, thereby reducing regulatory arbitrage and enhancing the stability of the EU financial system.

EBA’s Pillar 3 Data Hub: Centralising Prudential Disclosures

A major part of the European Banking Authority's (EBA) consultation is focused on the development of a Pillar 3 data hub, which will act as the central repository for prudential disclosures from all EU financial institutions. This centralization initiative aligns with the requirements of the Capital Requirements Regulation (CRR3) and the Capital Requirements Directive (CRD6), aiming to streamline the submission, publication, and accessibility of disclosure data. The Pillar 3 disclosures, as mandated by Articles 434 and 434a of CRR3, are crucial for improving transparency and market discipline, allowing stakeholders to have real-time, standardized access to the financial health data of institutions.

IT Solutions and Processes for the Pillar 3 Data Hub

The draft Implementing Technical Standards (ITS) outlined in the EBA’s consultation define the IT solutions and processes that large institutions and others must follow when submitting their Pillar 3 disclosures. These solutions aim to standardize data submission formats and streamline the reporting process, leveraging the EBA’s existing regulatory infrastructure and experience in data collection and reporting.

Key Features of the IT Solutions

- Standardized Data Formats: The EBA requires institutions to submit their data in standardized, machine-readable formats, such as XBRL (eXtensible Business Reporting Language). This standardized format ensures that data from different institutions can be easily aggregated and compared, improving the overall quality and usability of the disclosures. The use of machine-readable formats also supports automation and further aligns with Basel III Pillar 3 requirements for consistent and comparable risk data reporting.

- Technical Validations: Before the data is made publicly available through the Pillar 3 data hub, the EBA will conduct a series of technical validations to ensure the accuracy, completeness, and consistency of the submitted information. These validations are designed to prevent errors that could mislead stakeholders, ensuring that the published data maintains a high level of integrity. The validation processes are aligned with Part Eight of CRR3, ensuring that all required disclosures under the regulation are systematically checked for compliance.

- Submission Channels: Institutions, particularly large and complex ones, are required to use secure IT channels for submitting their disclosures. The EBA’s draft ITS outlines a differentiated approach, where the submission process varies based on the size and complexity of the institution. This tiered approach ensures that the regulatory burden remains proportionate to an institution’s risk profile and operational capacity. Smaller institutions may follow simplified processes, while larger ones are subject to more stringent submission and validation protocols.

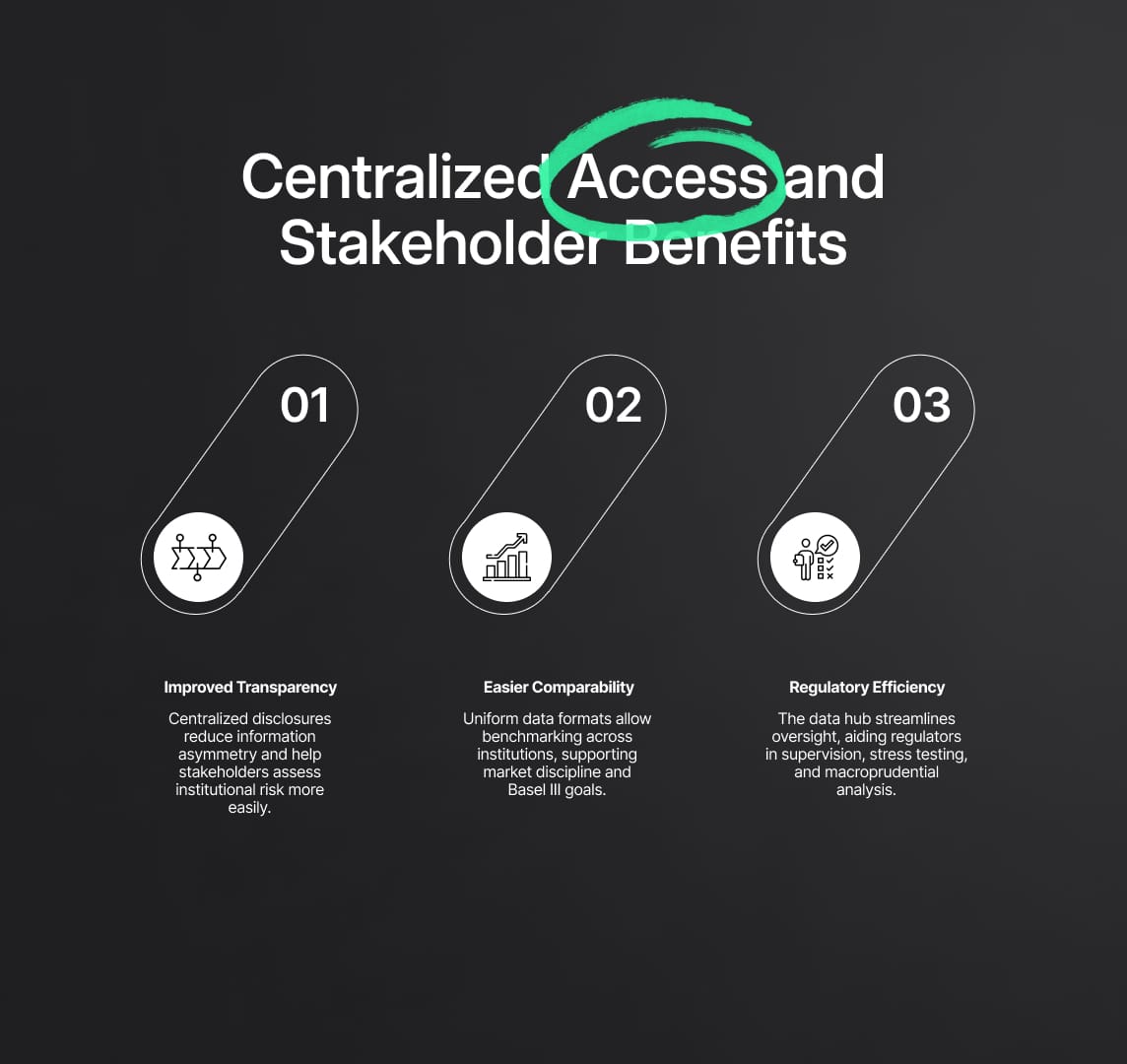

Centralized Access and Stakeholder Benefits

The EBA’s Pillar 3 data hub will provide a centralized platform where stakeholders, including regulators, investors, and the general public, can access all prudential disclosures in a standardized format. This centralization offers several benefits that align with the regulatory objectives of CRR3 and CRD6:

- Improved Transparency: Centralizing the disclosures allows stakeholders to access clear, standardized information, reducing the potential for information asymmetry. The platform will make it easier for market participants to assess the risk profiles of institutions and make informed decisions based on consistent and accurate data.

- Easier Comparability: With all data presented in a uniform format, stakeholders can more easily compare disclosures from different institutions. This comparability enhances market discipline by allowing investors and regulators to benchmark performance and risk management across the EU’s banking sector, in line with the goals set out in Basel III.

- Enhanced Regulatory Efficiency: For regulators, the data hub simplifies the monitoring and analysis of prudential disclosures. By providing a centralized access point for all disclosures, the EBA enables more effective oversight of compliance with CRR3 and CRD6 requirements. The platform also supports Competent Authorities, allowing them to use the data for supervisory reviews, stress testing, and macroprudential analysis.

Consultation and Industry Feedback

The EBA’s consultation on the draft ITS runs until 11 November 2024 and seeks input from both institutions and users of Pillar 3 information. This consultation is a key step in ensuring that the final standards are both practical and effective. The EBA encourages feedback not only on the proposed IT solutions but also on the usability and accessibility of the data hub itself.

Pilot Exercise and Feedback Analysis

In parallel with the consultation, the EBA is conducting a pilot exercise involving voluntary institutions. This pilot tests the proposed submission processes and IT solutions, providing valuable feedback that will be used to refine the final standards. In particular, the pilot will assess the feasibility of the proposed technical validations and data submission formats in real-world settings, ensuring that the final ITS are both robust and user-friendly.

Additionally, the EBA has incorporated feedback from an earlier discussion paper published in December 2023. This paper collected industry opinions on the feasibility of centralized disclosures and the use of machine-readable formats. The EBA has analyzed this feedback and incorporated it into the current consultation. Both the pilot findings and the industry feedback will play a crucial role in shaping the final version of the ITS, which will be submitted to the European Commission for adoption after the consultation concludes.

Future Impact of CRR3, CRD6, and the Pillar 3 Data Hub

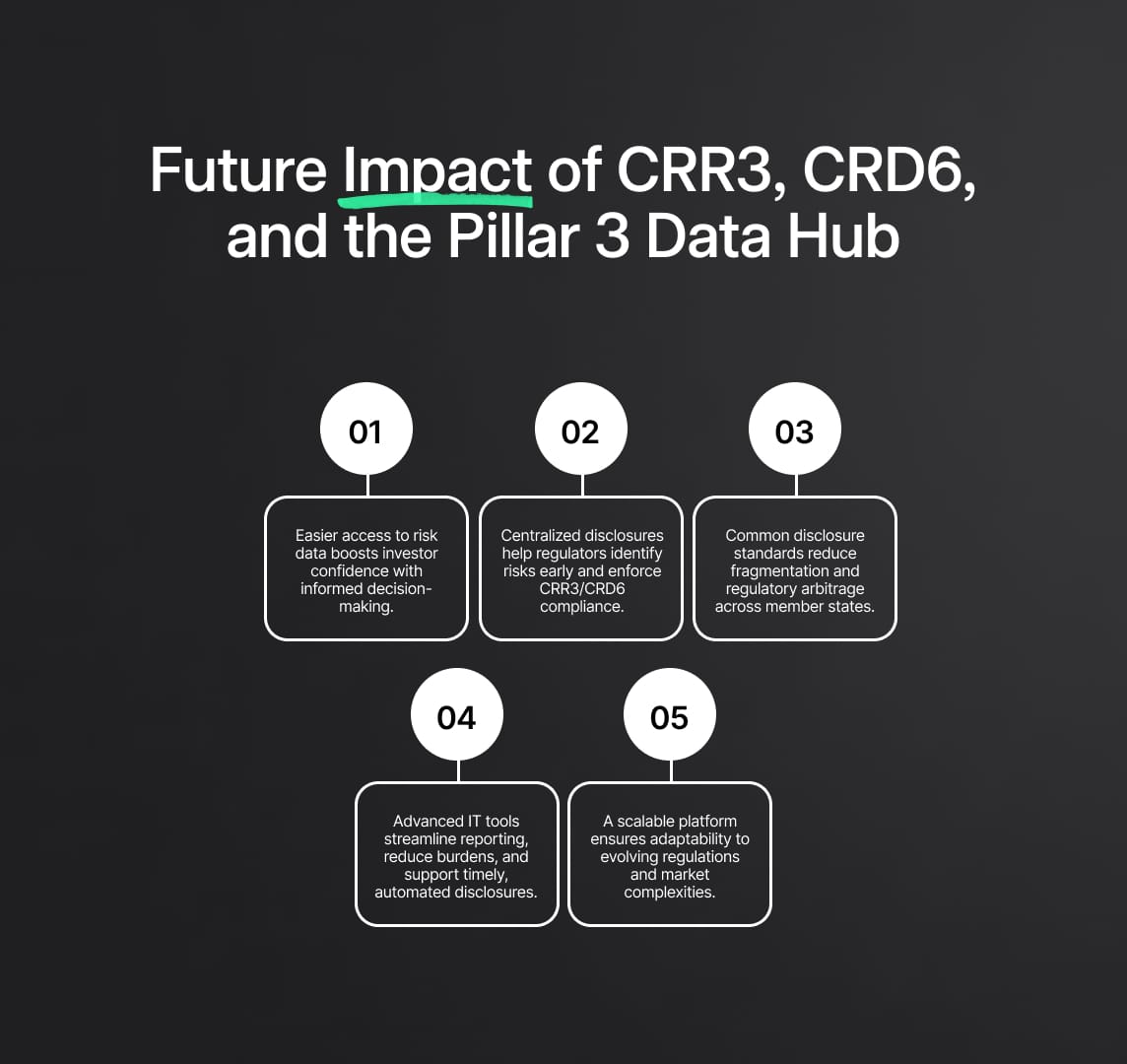

The implementation of CRR3, CRD6, and the EBA’s Pillar 3 data hub will have a profound impact on the future of the EU banking sector. The centralization of prudential disclosures and the standardization of submission processes are expected to create several long-term benefits, transforming how institutions report their capital and risk data.

- Increased Market Discipline: By making detailed financial and risk data more accessible, the Pillar 3 data hub will enhance market discipline. Investors and other stakeholders will have better insights into the risk profiles and capital adequacy of institutions, leading to more informed decision-making and fostering greater market confidence.

- Enhanced Regulatory Oversight: The centralized platform will enable regulators to monitor institutions more effectively, ensuring that they comply with prudential requirements set out in CRR3 and CRD6. The ability to compare disclosures across institutions will allow regulators to identify emerging risks more quickly and take preemptive measures to maintain financial stability.

- Harmonization Across the EU: CRR3 and CRD6 will ensure that all EU banking institutions adhere to a common set of disclosure standards, reducing fragmentation across national borders. This harmonization is essential for fostering a more integrated and resilient banking system within the EU. It also reduces the potential for regulatory arbitrage, ensuring a level playing field across jurisdictions.

- Technological Innovation and Efficiency: The use of advanced IT solutions for data submission and validation will drive innovation in how institutions handle regulatory reporting. This could lead to further automation and efficiencies in compliance processes, ultimately reducing the operational burden on institutions and improving the timeliness of disclosures.

- Future-Proofing Financial Transparency: As financial markets evolve and become more complex, the EBA’s data hub provides a flexible and scalable platform for maintaining transparency. This system can adapt to future regulatory changes, ensuring that the EU banking sector remains resilient in the face of new challenges. The flexibility of the data hub will also support the future integration of new disclosure requirements, keeping pace with changes in Basel III and other international regulatory frameworks.

Reduce your

compliance risks