European Benchmarks Regulation (BMR): Reforms and Compliance Insights

On October 17, 2023, the European Commission proposed a review of the Benchmarks Regulation to streamline reporting requirements in financial services legislation. It highlighted the broad scope of the BMR and low uptake of licensing routes for third-country benchmark administrators.

Why the European Benchmarks Regulation (BMR) Still Sets the Standard

Financial benchmarks, indices such as interest-rate fixings, foreign-exchange reference rates and commodity prices, anchor trillions of euros in loans, derivatives and investment products. After the LIBOR and FX-rate manipulation scandals revealed deep conflicts of interest, the European Union adopted the European Benchmarks Regulation (BMR) in 2018 to restore confidence and impose binding duties on benchmark administrators, data contributors and supervised users.

In late 2023 the European Commission tabled a broad review of this benchmark regulation, aiming to keep market integrity high while trimming unnecessary compliance costs. EU legislators struck a political agreement in December 2024, clearing the way for “BMR 2.0” to apply from 1 January 2026. The revamped framework narrows supervision to the most systemically important indices, fine-tunes the third-country regime and introduces tailored rules for ESG-climate and commodity benchmarks.

This article unpacks both the original BMR and the 2023-24 reforms. Written for compliance teams, asset managers and risk officers, it explains:

- why robust benchmark governance matters;

- the core obligations placed on administrators, contributors and users; and

- how BMR 2.0 reshapes day-to-day controls.

Authoritative material, ESMA Q&A, Commission staff papers and IOSCO principles, is referenced throughout so readers can align internal policies with global best practice. By safeguarding benchmark integrity without stifling innovation, the updated European Benchmarks Regulation seeks to strike the right balance for Europe’s capital markets. The next sections show how.

Background: From the LIBOR Scandal to a Binding EU Benchmark Regulation

The European Benchmarks Regulation (BMR) traces its roots to the 2012 revelations that several global banks had manipulated LIBOR and key foreign-exchange fixings. Those scandals shattered confidence in reference rates that underpin trillions of euros in financial contracts. In 2013 the International Organization of Securities Commissions (IOSCO) issued voluntary Principles for Financial Benchmarks on governance, transparency and methodology. The European Union went a step further, hard-wiring those best practices into law through its landmark benchmark regulation.

2016 Adoption and 2018 Entry into Force

- Regulation (EU) 2016/1011, better known as the original BMR, was adopted in June 2016 and applied in full from January 2018. Its mission: make every benchmark referenced in the EU reliable, transparent and resistant to manipulation.

What Fell in Scope?

- Broad definition: “any index” that determines a payment on a financial instrument, contract or investment fund. That captures interest-rate benchmarks (LIBOR, EURIBOR), FX fixings, securities and commodity indices, plus many proprietary offerings.

- Targeted carve-outs: central-bank rates, single-stock indices and certain bespoke contracts remained outside the rulebook to keep the focus on publicly disseminated, market-wide benchmarks.

Tiered Oversight Based on Systemic Importance

| Category | Threshold / Status | Supervisory Intensity | Example |

|---|---|---|---|

| Critical benchmarks | ≥ €500 bn outstanding contracts or formally designated by regulators | Full-scale, pan-EU oversight (ESMA direct supervisor) | EURIBOR |

| Significant benchmarks | ≥ €50 bn contracts or vital to a Member State’s stability | Authorisation plus lighter reporting | Key national bond indices |

| Non-significant benchmarks | All others | Core BMR principles; some waivers possible | Niche commodity indices |

Core Compliance Obligations

- Administrator authorisation: every EU benchmark administrator had to register with its National Competent Authority (NCA) by January 2020, set up robust internal controls and publish a detailed benchmark statement plus contributor code of conduct.

- Usage restriction: EU-supervised entities (banks, insurers, asset managers) may reference only benchmarks or administrators listed on the official ESMA register—creating a powerful incentive for global index providers to meet BMR standards.

- Third-country regime: non-EU benchmarks gained market access via one of three routes, equivalence, recognition or endorsement, with an initial grace period that was later extended beyond 2021.

- Supervision and penalties: day-to-day oversight sits with NCAs, while ESMA directly polices critical and, since 2022, recognised third-country administrators. Manipulating a benchmark is also outlawed under the Market Abuse Regulation, carrying severe fines.

- Contingency planning: benchmark users must embed fall-back provisions in contracts. A 2021 BMR amendment even allows the Commission to impose a statutory replacement for a defunct rate—averting chaos during the LIBOR wind-down.

Tangible Impact and Emerging Frictions

Since 2018 the European Benchmarks Regulation has:

- forced major indices such as EURIBOR to adopt transaction-based methodologies,

- accelerated the roll-out of alternative risk-free rates, and

- brought hundreds of benchmarks under transparent, public oversight.

Yet the “one-size-fits-all” model burdened small, local indices, and global convergence stalled: by 2023 only about 5 % of non-EU providers had secured EU recognition, leading some to withdraw from the market and curbing benchmark diversity.

Why Reform Became Inevitable

Those drawbacks prompted the European Commission’s 2023 review, which aims to refocus supervision on the most systemically important indices while easing compliance for lower-risk and third-country benchmarks. The next section breaks down how the forthcoming “BMR 2.0” reform addresses these challenges, and what it means for benchmark administrators, contributors and users.

2023–24 Review of the European Benchmarks Regulation (BMR): Rationale and Objectives

In October 2023 the European Commission unveiled a sweeping review of the European Benchmarks Regulation (BMR), often called “benchmark regulation”, as part of its drive to simplify EU financial-services rules. The initiative, eventually endorsed by Parliament and Council in December 2024, has five clear objectives:

- Lift the administrative burden on low-impact indices

Hundreds of non-significant benchmarks faced virtually the same authorisation process as critical benchmarks, an approach the Commission deemed disproportionate. The proposal therefore aims to exclude 80–90 % of small-scale administrators from full BMR compliance, freeing resources for innovation without jeopardising market integrity. - Keep systemic benchmarks robust and trustworthy

BMR 2.0 concentrates supervisory fire-power on indices that genuinely matter for financial stability, those whose disruption could ripple through loans, derivatives or investment funds. Critical benchmarks will still meet the highest governance, methodology and transparency standards. - Secure EU access to global benchmarks

With only ≈ 5 % of third-country providers meeting the existing recognition rules, EU firms risked losing key FX and commodity indices when the latest transition period expired. The revised benchmark regulation narrows the third-country regime so that only systemically important foreign benchmarks must obtain authorisation, while others remain available to EU users. - Boost competitiveness by cutting red tape

The reform is a pillar of the EU’s “Long-term Competitiveness” agenda, which targets a 25 % reduction in reporting and administrative costs across the Single Market. A leaner BMR supports deeper, more efficient capital markets on the road to 2030. - Reflect today’s priorities, ESG, climate benchmarks and SME needs

Since 2016 ESG indices have exploded, and the BMR already hosts Climate Transition Benchmarks (CTB) and Paris-Aligned Benchmarks (PAB). The 2023 review strengthens safeguards against “greenwashing” and channels lessons from the LIBOR wind-down, tailoring obligations so smaller firms and innovators can comply proportionately.

In short, the European Commission’s package keeps the core integrity of the European Benchmarks Regulation intact while recalibrating the rulebook to be risk-based, innovation-friendly and globally connected. The next section dissects the concrete rule changes—benchmark by benchmark—and highlights what administrators, contributors and users must prepare for under BMR 2.0.

Narrowing the Scope to Critical and Significant Benchmarks

The headline reform of the revised European Benchmarks Regulation (BMR), is its much tighter perimeter. From 2026 onward, only benchmarks that meet the critical or significant thresholds (or are expressly designated by supervisors) will remain subject to full benchmark regulation. Everything below that bar—roughly 80-90 % of today’s “non-significant” indices—drops out of compulsory oversight, relieving smaller providers of an onerous regime while keeping the most systemically important rates under the microscope.

How the New Materiality Test Works

| Benchmark tier | Original BMR (2018-2023) | Revised BMR 2.0 (political deal Dec 2024) |

|---|---|---|

| Critical | In scope. ≥ €500 bn in contracts or formally designated as systemically important (e.g., EURIBOR). Direct ESMA supervision; toughest rules. | Unchanged. Same €500 bn or designation test; ESMA still supervisor. |

| Significant | In scope. ≥ €50 bn or NCA designation. Full BMR duties (slightly lighter than critical). | In scope. ≥ €50 bn or designation by ESMA/NCA. Administrators must self-monitor usage and apply for authorisation within 60 working days after crossing the line. |

| Non-significant | In scope by default (with some waivers). | Out of scope. Administrators may opt-in voluntarily for a “BMR quality label,” but authorisation is no longer compulsory. |

Key Points Compliance Teams Need to Track

- €50 bn cut-off. Administrators must monitor the rolling average nominal amount referenced by their index. Once it tops €50 bn, the clock starts: 60 working days to file for authorisation (EU) or recognition/endorsement (non-EU). Failure to self-notify can trigger sanctions.

- €500 bn = critical. Nothing changes for the heavyweight benchmarks, if your index is already tagged critical (or designated in future), expect ESMA to stay directly on top of governance, methodology and contingency planning.

- Below €50 bn = freedom, mostly. Indices under the threshold are outside BMR unless they fall into a special bucket (see below). Providers can still apply to be regulated if market credibility or investor mandates make it worthwhile.

Special Buckets That Still Matter

| Category | Why it stays inside the rulebook | Revised trigger |

|---|---|---|

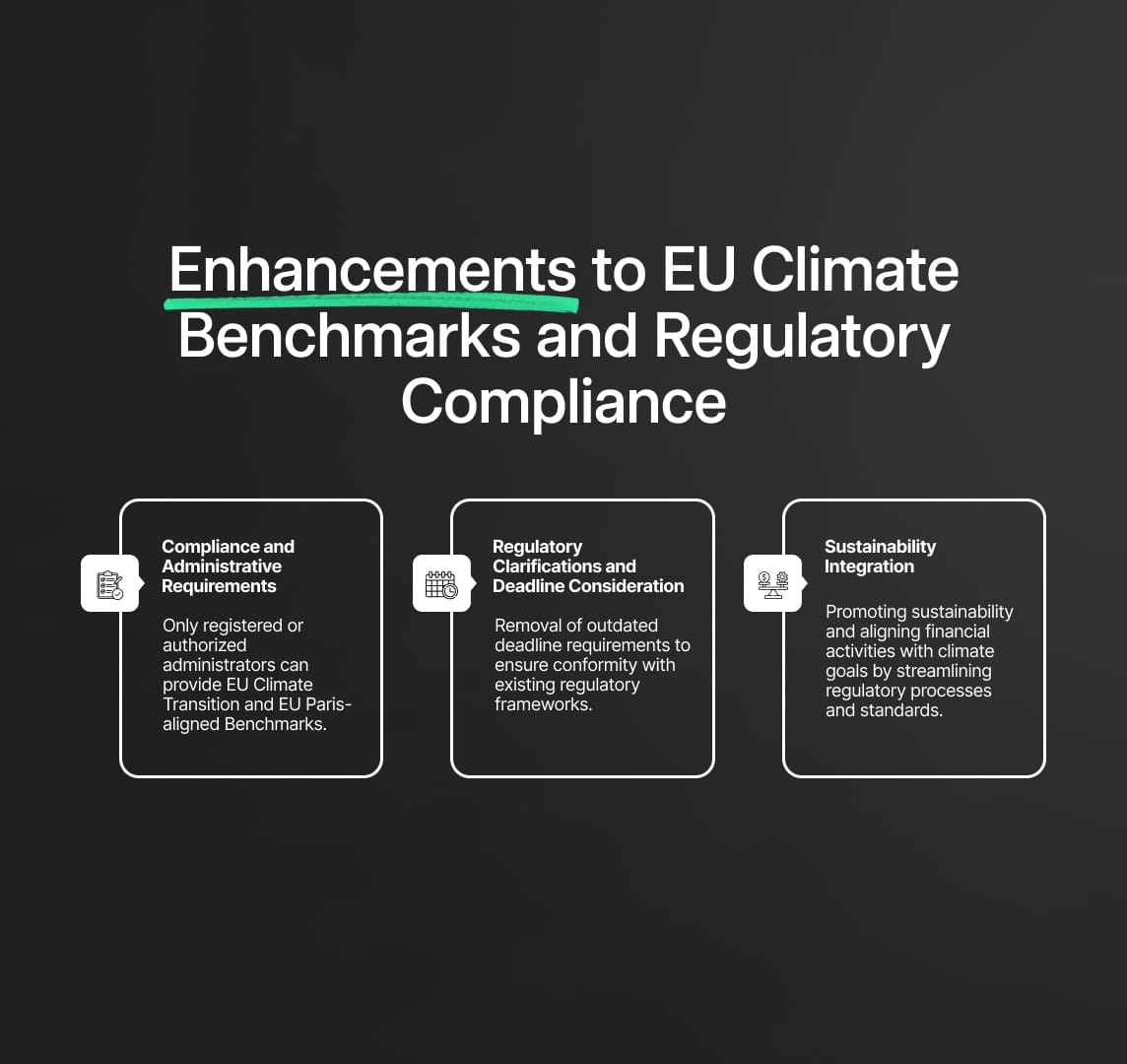

| EU Climate-Transition & Paris-Aligned Benchmarks (CTB/PAB) | EU policy priority to guard against “greenwashing.” | Every CTB/PAB—regardless of size—must be authorised/registered (or recognised if non-EU). The previous obligation for large administrators to offer a CTB/PAB disappears. |

| Commodity benchmarks | Many rely on unregulated spot-market data that is harder to police. | Two-step test: • ≥ €200 m average notional (12-month) • Data comes mainly from non-supervised entities. Below €200 m = out. |

| Spot-FX rates under capital controls | EU firms need access for hedging where no EU substitute exists. | Commission can grant a case-by-case exemption so EU banks can keep using them. |

Opt-In & Qualitative Designation

- Voluntary “significant” status. An administrator whose usage is above ~€20 bn—but still below €50 bn, can ask its national authority for the significant label, gaining the marketing benefit of appearing on the ESMA register.

- Regulatory override. Even under €50 bn, an NCA (in consultation with ESMA) may deem a benchmark significant if its cessation would seriously hurt market integrity, consumers or local financial stability and no substitute exists.

What This Means in Practice

- Compliance budgets refocused. SMEs and boutique index providers can redeploy resources from regulatory filings to product development and data quality.

- Bigger onus on usage analytics. Mid-size administrators must build tooling to track contractual reference values in near-real time, or risk missing the 60-day authorisation window.

- Investor due-diligence shift. Buy-side firms will rely more on their own governance checks when using out-of-scope indices, or will nudge providers to opt in for the “BMR-compliant” badge.

- Continued high bar for EURIBOR and peers. The flagship European rates that anchor mortgages and derivatives remain under intensive, centralised supervision, protecting trust in the EU financial system.

In short, BMR 2.0 moves Europe from a one-size-fits-all regime to a risk-based benchmark regulation model, trimming red tape without diluting safeguards for the indices that truly matter.

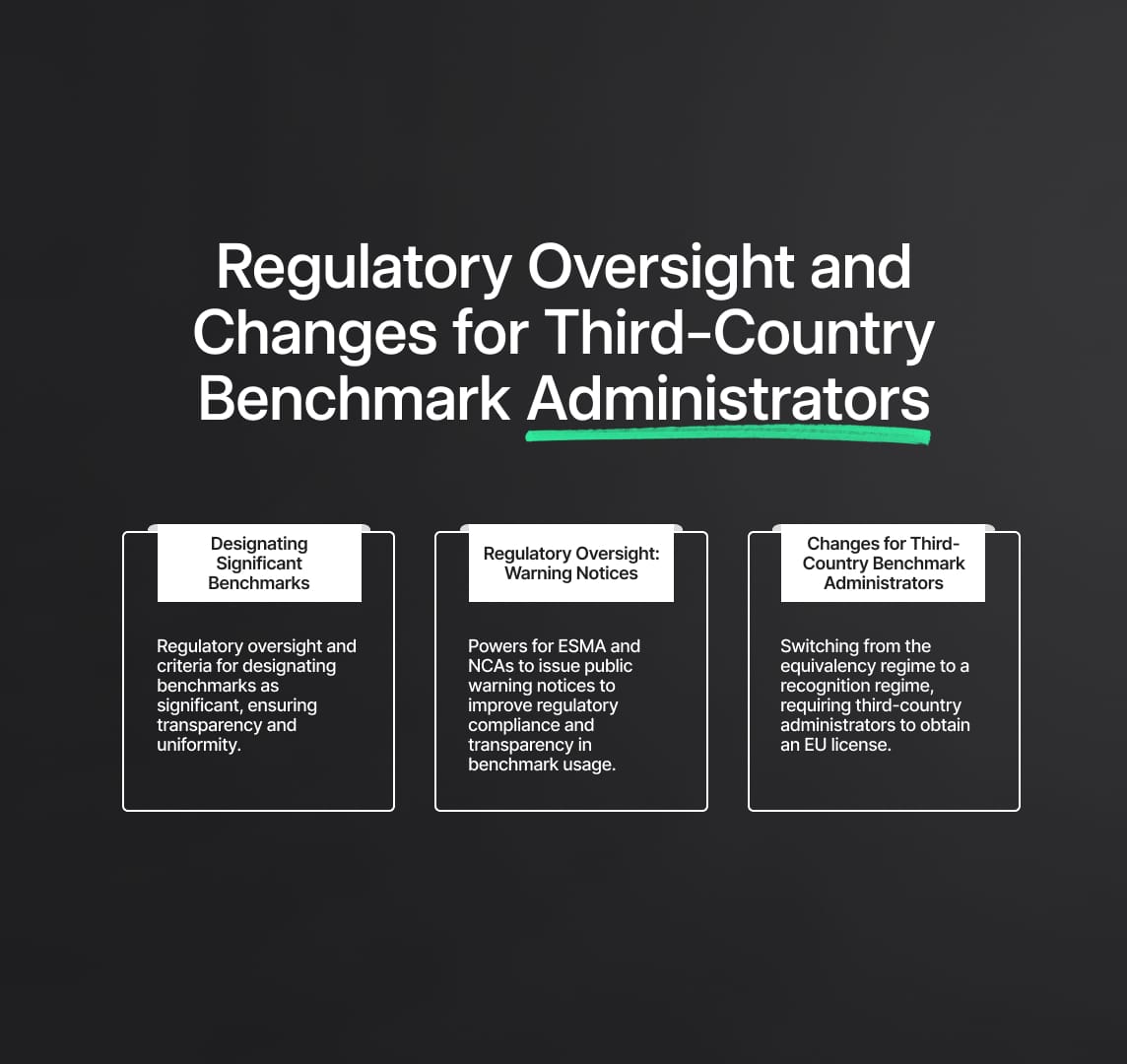

Third-Country Benchmarks: A Risk-Based, Market-Friendly Rewrite of the European Benchmarks Regulation (BMR)

The European Benchmarks Regulation (BMR) has always struggled with how to treat benchmarks administered outside the EU. Under the original benchmark regulation, third-country administrators were expected either to obtain EU recognition or to operate from a jurisdiction deemed “equivalent” to the BMR—a costly ask that only ≈ 5 % of global providers satisfied by mid-2023. That gap threatened to cut EU banks, asset managers and corporates off from vital indices ranging from Asian equity benchmarks to specialist commodity and FX rates.

How BMR 2.0 Resolves the Third-Country Dilemma

- Scope aligned with EU materiality rules

- Only third-country benchmarks that would qualify as significant (≥ €50 bn in EU-referenced contracts) or critical (≥ €500 bn or formally designated) remain in scope.

- Smaller foreign benchmarks, by far the majority, become freely usable by EU-supervised entities without any BMR authorisation.

- One-stop supervision by ESMA

- From 2026, ESMA replaces the patchwork of national regulators as the single authority for all third-country recognition and endorsement files, giving non-EU providers a clear, uniform process.

- Permanent, more credible recognition regime

- Recognition no longer expires with the end of a transition period.

- The non-EU administrator must appoint an EU-based legal entity as its representative, giving ESMA real enforcement leverage.

- Designations for benchmarks just below the threshold

- ESMA can still pull a foreign benchmark into the regime if its cessation would materially harm EU markets and no substitute exists—even if it sits below €50 bn.

- Targeted spot-FX exemption

- The European Commission may exempt specific non-EU spot-FX benchmarks—especially where a currency is under capital controls and no EU alternative exists, so EU firms can continue hedging without disruption.

- Extended transition period

- The current blanket relief for non-EU benchmarks now runs until 31 December 2025, smoothing the hand-over to the new rules that take effect on 1 January 2026.

At-a-Glance: Access Routes for Non-EU Benchmarks

| Access route | Original BMR (2018-2023) | BMR 2.0 (in force 2026) |

|---|---|---|

| Equivalence (country-level) | Commission may declare another jurisdiction’s rules “equivalent”, allowing all its benchmarks to be used. Rarely applied. | Unchanged in principle; still expected to be infrequent. |

| Recognition (administrator-level) | Non-EU administrator applied to an individual NCA; recognition was time-limited and required an EU legal representative (often just a natural person). | Now processed centrally by ESMA; available only to significant/critical benchmarks; recognition is permanent; representative must be an EU-incorporated legal entity. |

| Endorsement (benchmark-by-benchmark) | An EU-authorised administrator could endorse a foreign benchmark and assume responsibility for BMR compliance. | Still possible, but ESMA supervises the endorsing EU entity; likely used less because many foreign benchmarks will be out of scope. |

| Exemption (new spot-FX regime) | Not available. Only rolling transition delays kept FX rates usable. | Commission can place designated spot-FX benchmarks on an exemption list so EU users may reference them without recognition or endorsement. |

Practical Implications for Compliance Teams

- Vastly smaller compliance universe: Only a handful of global indices, those that truly matter for EU financial stability, need to navigate ESMA recognition or endorsement.

- Clear accountability: A single EU regulator (ESMA) and an on-the-ground EU legal entity make enforcement credible without burdening dozens of national authorities.

- Continuity of market access: EU firms retain seamless access to niche or regional benchmarks that fall below the €50 bn threshold, eliminating the “cliff-edge” risk that hung over previous transition deadlines.

- Still risk-based control: If a once-minor foreign benchmark grows in EU importance, ESMA can reclassify it as significant and pull it into the regulatory net—maintaining the integrity objective at the heart of the European Benchmarks Regulation.

In sum, BMR 2.0 re-engineers third-country access from a one-size-fits-all barrier into a proportionate, risk-based gateway. EU market participants keep the global data they need, third-country administrators avoid needless red tape, and regulators can still lock down the benchmarks that genuinely underpin Europe’s financial system.

Climate Benchmarks and ESG in the European Benchmarks Regulation (BMR)

The 2019 update to the European Benchmarks Regulation (BMR) introduced two flagship low-carbon indices, the EU Climate Transition Benchmark (CTB) and the EU Paris-Aligned Benchmark (PAB), to steer capital toward decarbonisation. Administrators offering a CTB or PAB must apply strict selection criteria (emissions cuts, sector exclusions) and provide granular ESG disclosures.

What BMR 2.0 Changes, and What It Keeps

| Topic | Position under original benchmark regulation | Position under BMR 2.0 |

|---|---|---|

| Mandatory scope | CTB/PAB always in scope, whatever their size. | Unchanged. Every CTB and PAB—EU or third-country—must be authorised, recognised or endorsed. No de-minimis carve-out, safeguarding credibility and limiting greenwashing. |

| “Must-offer” duty for large administrators | Significant administrators had to endeavour to launch at least one CTB by 2022 (or explain why not). | Deleted. Market now drives product development; no legal compulsion, but regulators still encourage innovation in sustainable indices. |

| ESG methodology & disclosure rules | Detailed minimum standards on carbon intensity, trajectory (-50 % vs market, -7 % p.a.), exclusions and transparency. | Maintained. ESMA/NCAs remain responsible for policing methodology, data quality and public benchmark statements. |

| Link-up with broader EU sustainable-finance legislation | Article 13 BMR already requires ESG factor disclosure for most benchmarks. | Continues. Streamlining of templates is under review, but core disclosure obligations stay. |

Compliance Take-aways

- Zero-threshold rule: CTB and PAB labels carry an automatic BMR licence or recognition requirement, even if the index falls below the €50 bn “significant” line.

- No more forced product launches: Large benchmark providers are free to prioritise climate offerings organically, yet the regulatory door stays open for voluntary expansion.

- Ongoing transparency checks: Administrators must keep publishing robust decarbonisation data and methodology notes; ESMA will scrutinise claims to avert greenwashing.

For index sponsors and users alike, the message is clear: climate-linked benchmark regulation remains front-and-centre in Europe’s sustainable-finance agenda. If you run, or invest against, a CTB or PAB, full BMR compliance is non-negotiable, regardless of market share.

Commodity Benchmarks: Tailored Oversight Under BMR 2.0

Commodity-price indices, from crude oil and natural gas to gold, wheat and coffee, raise distinct governance issues under the European Benchmarks Regulation (BMR). Many are built on contributor surveys rather than on-exchange trades, and the contributors themselves are often outside the perimeter of financial supervision. BMR 2.0 keeps that reality firmly in view by splitting commodity benchmarks into two risk-based buckets:

| Commodity benchmark bucket | Trigger for BMR scope | Rationale | Practical outcome |

|---|---|---|---|

| Exchange-based / regulated-data benchmarks | Inputs come mainly from “readily available” transaction data on regulated markets. In scope only if the index is significant (≥ €50 bn EU usage) or critical (≥ €500 bn or designated). | Trades are already supervised elsewhere, so incremental manipulation risk is lower. | Most exchange-derived commodity indices fall out of scope unless they cross the €50 bn threshold. |

| Benchmarks with non-supervised contributors (e.g. survey-based oil or metals prices) |

Total average nominal value of EU-referencing contracts ≥ €200 m over 12 months. | Data comes from producers, brokers or PRAs not otherwise regulated; lower materiality threshold guards against manipulation. | Even mid-sized benchmarks must stay BMR-compliant once they top €200 m. Below that, they fall out of scope. |

Journalistic/PRA indices remain supervised. Law-makers kept price-reporting-agency benchmarks (think Platts Brent, Argus fuel indices) under the benchmark regulation irrespective of size above the €200 m floor, reflecting their systemic importance to energy markets and consumer prices.

Compliance checkpoints for commodity administrators

- Categorise each index: is the data exchange-traded or survey-based?

- Track notional exposure: monitor rolling 12-month EU usage against the €200 m and €50 bn lines.

- Maintain Annex II controls where required: robust methodology governance, contributor codes of conduct, conflict-of-interest policies and contingency plans.

- Prepare for 2026: only indices breaching the thresholds, or PRA-style benchmarks, remain on the ESMA register after 1 January 2026.

For users of commodity indices, BMR 2.0 offers clarity: high-impact or data-sensitive benchmarks stay under strict BMR oversight, while niche indices shed unnecessary red tape, preserving market integrity without stifling innovation in benchmark design.

Enhanced Oversight and Enforcement Powers under BMR 2.0

The 2024 reform package gives supervisors tougher, better-targeted tools to guarantee that every benchmark still captured by the European Benchmarks Regulation (BMR) remains accurate, transparent and trustworthy.

1. ESMA: Europe-wide “single interlocutor”

- Expanded remit: The European Securities and Markets Authority now supervises all critical benchmarks, every third-country benchmark that needs recognition or endorsement, and coordinates EU-wide policy for significant indices.

- Central gateway for non-EU providers: Foreign administrators file one application with ESMA, eliminating the old patchwork of national competent authorities (NCAs). Expect more consolidated guidance and Q&A as ESMA builds a pan-EU centre of expertise on benchmark regulation.

2. National Competent Authorities: sharper frontline duties

- Threshold policing: NCAs monitor the €50 billion “significant” line and the 60-day authorisation clock for local administrators.

- Designation powers: Where a benchmark falls below €50 billion but its cessation would hit market integrity or consumers, an NCA, after consulting ESMA, can still label it significant.

- Opt-in management: Out-of-scope administrators that want the BMR “quality label” must apply through their home NCA.

3. Public warnings and use restrictions: a new enforcement lever

If ESMA or an NCA finds that a significant benchmark or an EU Climate/Paris-Aligned Benchmark breaches BMR rules they can:

- Publish an official warning naming the non-compliant index and the failings.

- Ban new exposures: EU-supervised banks, insurers and asset managers must immediately stop referencing the benchmark in new contracts.

- Mandatory transition: Existing positions must switch to an alternative within a set grace period.

The threat of a public blacklist is a strong incentive for administrators to fix problems quickly and maintain compliance with the European Benchmarks Regulation.

4. Standard identifiers for clarity and data hygiene

- Legal Entity Identifier (LEI) for every administrator.

- International Securities Identification Number (ISIN) for each benchmark.

Regulators urge administrators to obtain and publish these codes so users can reference benchmarks unambiguously in contracts, databases and regulatory reports—boosting transparency and cutting operational risk.

5. Penalties remain robust, and now more focused

Fines, suspensions and other sanctions still apply when an administrator:

- Fails to notify that it has crossed the €50 billion significance threshold,

- Continues to publish an un-authorised benchmark, or

- Obstructs supervisory investigations.

With ~80 % fewer benchmarks in scope after the reform, regulators can concentrate resources on the indices that genuinely matter, heightening the deterrent effect.

6. Living rulebook: ongoing reviews and technical guidance

The updated benchmark regulation mandates periodic Commission reviews and empowers ESMA to issue detailed Q&A and technical standards (e.g., how to calculate aggregate EU usage). Compliance teams should monitor:

- ESMA Q&A updates,

- Delegated acts refining threshold metrics, and

- Cross-references to other EU regimes (PRIIPs, SFDR, EMIR reporting).

International Context: How the European Benchmarks Regulation (BMR) Shapes, and Learns From, Global Benchmark Governance

The EU’s benchmark regulation remains the most comprehensive framework worldwide, but it sits inside a larger, fast-evolving ecosystem of rules and best practices. A clear view of that landscape helps compliance teams anticipate cross-border issues and keep governance standards aligned.

| Region / body | Regulatory model | Recent moves and interplay with BMR 2.0 |

|---|---|---|

| IOSCO | Principles-based. The 19 IOSCO Principles (2013) form the global baseline for benchmark integrity—covering governance, methodologies and contributor conduct. | The European Benchmarks Regulation hard-codes IOSCO into law and layers on extra detail. Many non-EU administrators rely on “IOSCO-compliant” status when marketing benchmarks into Europe. |

| United Kingdom | On-shored BMR + targeted tweaks. FCA oversees the UK Benchmarks Regulation. Transition relief for non-UK indices has been pushed to 2025 (and signalled to 2030). | The UK used BMR powers to create synthetic LIBOR for legacy contracts—an intervention now echoed by the EU, US and others. Divergence is modest but firms should track UK-specific guidance as the Future Regulatory Framework evolves. |

| United States | Enforcement-led, sectoral statutes. No EU-style authorisation regime; integrity enforced via antitrust, fraud and sector rules (CFTC, SEC). The LIBOR Act 2022 provides a statutory fallback but does not license administrators. | Major US index providers follow IOSCO voluntarily; only large US benchmarks marketed into the EU will need BMR recognition after 2026. |

| Asia-Pacific (JP, AU, SG, CA) | Select licensing. Japan and Australia license administrators of systemically important rates; Singapore and Canada blend IOSCO compliance with supervisory guidance. | These jurisdictions track EU/UK outcomes: TIBOR, BBSW, SOR, CDOR have been revamped to meet IOSCO. None impose a benchmark regime as broad as the EU’s. |

| Global coordination | FSB & BIS steering. The Financial Stability Board drove the risk-free-rate transition and still monitors benchmark resilience. | EU authorities share lessons via the FSB; other members often adopt EU playbooks—e.g., statutory replacement powers for benchmark cessations. |

Key Take-aways for Cross-Border Compliance

- IOSCO is the lingua franca. Wherever your benchmark is based, aligning with the IOSCO Principles gives you a transferable governance passport, and makes upgrading to BMR 2.0 simpler if your EU usage tops €50 billion.

- UK and EU are drifting, not divorcing. Core concepts, critical versus significant benchmarks, contributor codes, fallback planning, remain parallel. But timelines and relief measures differ, so multi-currency programmes must map both rule sets.

- The US favours deterrence over licensing. For EU-facing benchmarks, that means reconciling a disclosure-heavy European Benchmarks Regulation file with a lighter US home regime.

- Statutory fallback powers are now standard. The EU, UK and US have each used legislation to impose replacement rates for LIBOR. Expect the same playbook if another critical benchmark falters.

- Size now dictates scope. After the 2024 reform, only foreign benchmarks that are significant or critical for EU users need recognition. Smaller indices can market into Europe on an IOSCO-only basis, but must watch growth triggers closely.

Bottom line: The EU’s benchmark regulation continues to set the high-water mark for formal oversight, yet global momentum is moving toward the same goal, robust, transparent and reliable indices. Firms active across regions should treat BMR 2.0 as the strictest common denominator, building IOSCO-aligned controls that can scale up to full EU authorisation if usage crosses the new materiality lines.

Implications for Compliance Officers and Market Participants under BMR 2.0

1. Benchmark Administrators inside the EU

- Re-map your product universe. Re-classify every index against the new scope tests. Many “non-significant” benchmarks will fall outside the European Benchmarks Regulation (BMR) from 2026.

- Decide whether to opt-in. Staying under the benchmark regulation can signal quality and keep institutional clients comfortable. Balance that marketing benefit against lower compliance costs if you exit.

- Build threshold-tracking dashboards. Any benchmark that might exceed €50 billion in EU exposure needs automated alerts, a 60-day authorisation playbook and clear NCA notification lines.

- Special cases:

- Climate benchmarks (CTB/PAB) – always in scope, no matter the size.

- Commodity benchmarks – may stay inside the rulebook at €200 million if data comes from non-supervised contributors.

2. Benchmark Administrators outside the EU

- Check EU usage now. If no index is significant or critical for EU clients, you will no longer need recognition or endorsement after 31 Dec 2025.

- Plan for ESMA recognition if your index crosses the new materiality lines. A single ESMA file replaces 27 national processes, but you must appoint an EU-incorporated legal representative.

- Watch the spot-FX exemption list. Engage with the Commission if you publish a currency rate that could qualify.

- Use the transition window. The extended grace period to end-2025 is your chance to restructure EU offerings or finalise compliance.

3. Financial Institutions & Other Benchmark Users

- More choice, more homework. Many foreign or niche indices will be freely usable under the updated BMR, but they won’t appear on the ESMA register. Enhance due-diligence checklists (governance, IOSCO alignment, data quality).

- React fast to regulator warnings. A public notice from ESMA or an NCA will ban new exposure and trigger mandatory transition for legacy contracts. Build monitoring and fallback procedures today.

- Revise policies by 2026. Update internal rulebooks that equate “on the ESMA register” with “permitted”, that shortcut will no longer hold.

4. Documentation & Contract Management

- Fallback clauses stay best practice. In-scope benchmarks still require robust alternatives under Article 28(2) BMR. Out-of-scope indices are exempt, but contract resilience argues for keeping fallbacks anyway.

- Disclosure touch-ups. Prospectuses, KIIDs and client letters that boast “authorised benchmark” status may need correction if an index drops off the register by design, not by default.

5. Competitive Dynamics

- Lower entry barriers. Niche benchmark providers can launch products without the full weight of benchmark regulation, potentially undercutting incumbents.

- Differentiate on integrity. Regulated administrators should emphasise governance, transparency and BMR compliance to justify pricing and retain market share.

6. Supervisors: ESMA & NCAs

| Task | ESMA | NCAs |

|---|---|---|

| Third-country recognition & endorsement | Sole authority | — |

| Direct oversight | Critical benchmarks; recognised non-EU administrators | Significant EU benchmarks |

| Designation powers | Can pull foreign benchmarks into scope | Can label domestic benchmarks “significant” and manage opt-ins |

| Enforcement | Public warnings, use bans, sanctions | Same, within national remit |

Action Checklist for 2025

| Q4 2024–Q1 2025 | Q2–Q3 2025 | Q4 2025 |

|---|---|---|

|

• Map all benchmarks to new categories • Decide opt-in/opt-out strategy |

• Build usage-tracking and notification tools • Draft ESMA recognition files if needed |

• Update contracts & disclosures • Final compliance tests before 1 Jan 2026 |

Conclusion: A Sharper, Risk-Based Benchmark Regulation

The revamped European Benchmarks Regulation (BMR) channels five years of practical experience into a leaner, more proportionate rulebook. By zeroing in on critical and significant indices, EU legislators preserve trust in the benchmarks that anchor Europe’s financial system while freeing smaller players to innovate. Compliance teams now face a dual challenge: scaling down where regulation no longer applies and doubling down where it still does. Mastering that balance—and communicating it clearly to clients, will be the hallmark of strong governance in the benchmark regulation era ahead.

Reduce your

compliance risks