ISSB Standards (IFRS S1 & IFRS S2) vs ESRS: Sustainability Reporting

IFRS Foundation updates guidance on ISSB Standards, aligning IFRS 1 and IFRS 2 to enhance global sustainability reporting and climate-related financial disclosures.

Global Baseline: Sustainability Standards Board (ISSB) Standards

The International Sustainability Standards Board has released IFRS S1 General Requirements and IFRS S2 Climate-related Disclosures as the first worldwide baseline for sustainability reporting. These Sustainability Standards Board (ISSB) Standards require companies to reveal all material sustainability risks and opportunities, especially climate risks under IFRS S2, in decision-useful detail for investors. Supported by the G7, G20, IOSCO and leading investors, the standards are designed to curb greenwashing and deliver comparable, investor-grade ESG data.

EU Framework: European Sustainability Reporting Standards (ESRS) under CSRD

Parallel to the ISSB initiative, the EU Corporate Sustainability Reporting Directive (CSRD) mandates European Sustainability Reporting Standards. Grounded in double materiality, ESRS, such as ESRS E1 for climate, oblige companies to disclose issues that affect financial performance and those that significantly impact people or the environment, providing a broader, stakeholder-oriented ESG view.

Interoperability vs. Key Differences

Both ISSB and ESRS draw heavily on the TCFD framework and share many disclosure elements, yet several differences matter for compliance teams:

- Materiality lens: IFRS S1/S2 use single materiality; ESRS applies double materiality.

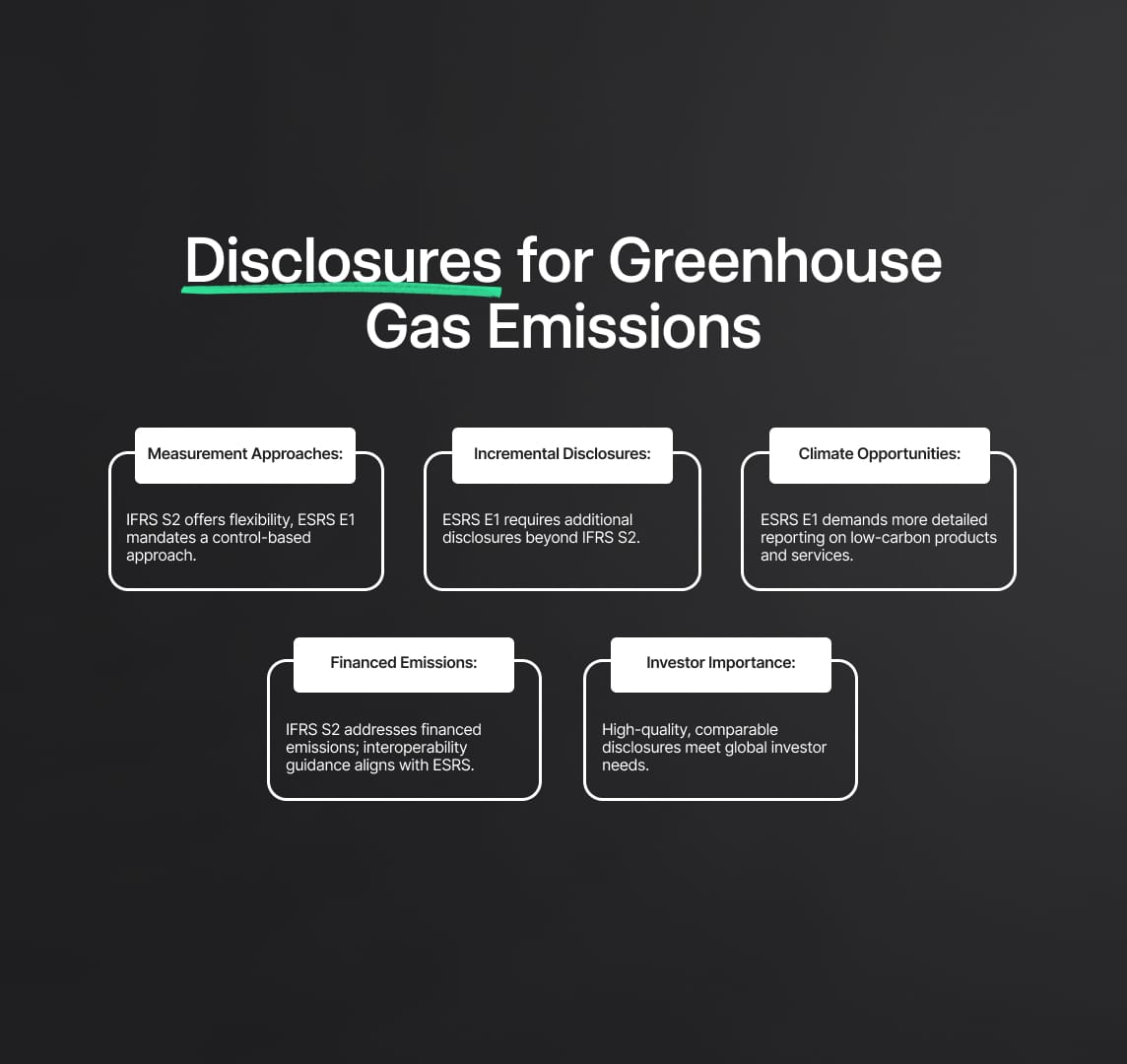

- Scenario analysis: IFRS S2 mandates quantitative climate-scenario analysis; ESRS E1 generally encourages it but does not always require it.

- Metrics: IFRS S2 specifies industry metrics (e.g., financed emissions for banks); ESRS demands additional impact metrics such as energy-consumption mix and intensity.

- Carbon credits: Both call for transparency on offsets; IFRS S2 stresses integrity and verification, whereas ESRS E1 adds further detail when credits underpin neutrality claims.

Investor Pressure and Regulatory Uptake

In 2024, a coalition of 120 global investors urged regulators to mandate IFRS S1 and IFRS S2 worldwide by 2025, asserting that a unified baseline reduces reporting costs and heightens comparability. IOSCO’s endorsement has already prompted more than 30 jurisdictions, representing roughly 57 % of global GDP, to advance ISSB-aligned rules. Investor networks such as Climate Action 100+ now benchmark companies on alignment with TCFD or ISSB, directly tying capital allocation and engagement to these standards.

Compliance Roadmap for Multiregional Companies

For entities active in both global and EU markets, simultaneous compliance with IFRS S1/S2 and ESRS is strategic and urgent. Priority actions include:

- Gap analysis between ISSB and ESRS requirements.

- Adoption of emerging interoperability guidance for climate disclosures.

- Build robust data systems capable of capturing full Scope 1–2–3 and financed-emissions inventories.

- Integrate scenario analysis into enterprise risk management to satisfy IFRS S2.

- Collect broader ESG data to meet ESRS social and governance topics.

By weaving these steps into a unified reporting roadmap, organisations can meet investor expectations, satisfy regional legal mandates, and enhance market credibility.

What’s Ahead

The sections that follow unpack technical disclosure mechanics, legal obligations and operational implications, equipping compliance officers and ESG leaders with the insight needed to navigate IFRS S1, IFRS S2 and ESRS requirements through 2025 and beyond.

Understanding the Sustainability Standards Board (ISSB) Standards: IFRS S1 and IFRS S2

1. ISSB Background: Why a Global Baseline Was Needed

Created by the IFRS Foundation in 2021, the International Sustainability Standards Board responded to investor, G20 and G7 calls for globally consistent ESG reporting. After two years of public consultation, the Board issued its first Sustainability Standards Board (ISSB) Standards, IFRS S1 and IFRS S2, in June 2023, positioning them as the comprehensive global baseline for capital-market sustainability disclosure. Building on TCFD guidance and SASB metrics, the standards sit alongside financial statements to give investors a 360-degree view of enterprise-value risks and opportunities.

2. IFRS S1: General Requirements for Sustainability Disclosure

IFRS S1 applies to all sustainability topics and sets cross-cutting principles:

| Core Principle | Regulatory Expectation | Practical Implication for Reporters |

|---|---|---|

| Investor-Materiality | Disclose any sustainability risk or opportunity that could reasonably influence enterprise value. | Non-financial impacts that do not affect the company’s outlook remain optional (contrast with ESRS double materiality). |

| Financial Connectivity | File sustainability disclosures at the same time as financials and explicitly link to related line items. | Example: connect climate-driven asset impairments in the notes to climate risk discussion. |

| Industry-Specific Focus | Use SASB standards to identify sector-relevant issues and metrics. | 77 industry standards now fall under ISSB stewardship, giving preparers a ready-made metric catalogue. |

| Framework References | Consider other leading frameworks (GRI, CDSB, etc.) when assessing material topics beyond climate. | IFRS S1 functions as the umbrella beneath which future topic-specific ISSB standards will sit. |

| GAAP-Agnostic | Compatible with any national GAAP or IFRS Accounting Standards. | Multinational groups can adopt without changing underlying accounting policies. |

3. IFRS S2: Climate-related Disclosures (Investor Lens)

The first topic-specific Sustainability Standards Board (ISSB) Standard, IFRS S2, extends TCFD architecture and demands granular climate data:

Governance & Strategy

- Explain board oversight, management responsibility and strategic responses to physical and transition climate risks across short, medium and long terms.

- Detail processes for identifying, assessing and integrating climate risks and opportunities into enterprise risk management.

Metrics & Targets

- Report cross-industry metrics, including absolute GHG emissions (Scopes 1, 2 & 3), internal carbon price, and revenue or assets linked to climate opportunities.

- Disclose legally mandated climate targets and progress toward voluntary or regulatory goals.

Scenario Analysis

- Perform at least one quantitative scenario, covering a 1.5 °C or well-below-2 °C pathway, and describe assumptions, time horizons and business resilience.

Financed Emissions (Financial Institutions)

- Banks, insurers and asset managers must measure and publish Category 15 Scope 3 (financed) emissions using PCAF-aligned metrics such as emissions per monetary unit financed and portfolio exposure to carbon-intensive industries.

4. Integrated Application: IFRS S1 + IFRS S2

The two Sustainability Standards Board (ISSB) Standards are intended to be applied together: IFRS S2 acts as a climate appendix to the general disclosure architecture of IFRS S1. Both retain the four TCFD pillars, Governance, Strategy, Risk Management, Metrics & Targets, ensuring logical coherence for preparers and users.

5. Effective Date and Global Uptake

- Effective for periods beginning on or after 1 January 2024; early adoption permitted if both standards are applied simultaneously.

- July 2023: IOSCO’s endorsement urged 130 securities regulators to adopt or allow the standards.

- By end-2024:

- 13 jurisdictions (e.g., Canada, Japan, United Kingdom, Hong Kong, Malaysia, Nigeria, Brazil) had already enacted or permitted IFRS S1 and IFRS S2 for certain entities starting 2024–2025.

- 22 further jurisdictions announced adoption plans, targeting 2025–2026 effective dates.

- Examples of fast movers:

- Hong Kong—mandatory “comply or explain” IFRS S2 climate disclosures from 2025; full compliance by 2026.

- Malaysia—large listed companies to report under ISSB Standards from 2025.

Collectively, jurisdictions representing well over half of global GDP are converging on ISSB-aligned rules, confirming IFRS S1 and IFRS S2 as the de facto international benchmark for climate and sustainability reporting.

6. Key Takeaways for Compliance Teams

- Materiality Filter —Frame disclosures around investor-relevant financial impacts; societal impacts alone are optional unless financially material.

- Connectivity —Cross-reference climate disclosures to related financial-statement effects.

- Data Depth —Prepare to capture full Scope 1-3 emissions and, for financial firms, financed-emissions inventories.

- Scenario-Ready —Develop internal capability to run Paris-aligned and high-physical-risk scenarios.

- Jurisdiction Watch —Track local regulator timelines to align first-year reporting with statutory requirements.

These Sustainability Standards Board (ISSB) Standards raise the bar for transparency, comparability and investor decision-usefulness. Mastery of their requirements now will position companies for credible, compliant ESG reporting as global adoption accelerates.

The EU’s ESRS Framework under CSRD: Regional Mandate and Global Context

1. CSRD and ESRS: Expanding Mandatory ESG Reporting in Europe

The Corporate Sustainability Reporting Directive (CSRD), effective January 2023, dramatically widens EU sustainability-reporting obligations. Roughly 50 000 EU- and non-EU-based companies with significant EU operations must begin reporting environmental, social and governance (ESG) data as early as fiscal-year 2024 (large public-interest entities first, with phased-in dates for others). To make CSRD operational, the European Commission—guided by EFRAG, adopted the European Sustainability Reporting Standards (ESRS) via Delegated Acts in mid-2023.

2. Double Materiality: The Cornerstone of ESRS

Unlike the investor-focused materiality used by Sustainability Standards Board (ISSB) Standards, namely IFRS S1 and IFRS S2—ESRS applies double materiality:

| Lens | Definition | Reporting Trigger |

|---|---|---|

| Financial Materiality | A matter capable of affecting enterprise value (identical to the IFRS/ISSB concept). | Report if relevant to investors or creditors. |

| Impact Materiality | A matter generating significant effects on people or the environment, even without near-term financial impact. | Report if outward impacts are significant for any stakeholder. |

A topic is disclosed if it meets either test, resulting in broader, stakeholder-oriented coverage (e.g., biodiversity loss or supply-chain human-rights issues) compared with the Sustainability Standards Board (ISSB) Standards’ single-materiality filter.

3. ESRS Architecture: Cross-Cutting and Topical Standards

The first ESRS set (July 2023) comprises:

- Cross-cutting: ESRS 1 General Requirements and ESRS 2 General Disclosures—analogous to IFRS S1 in scope and principle.

- Topical (10):

- Environment —E1 Climate Change, E2 Pollution, E3 Water & Marine, E4 Biodiversity, E5 Resource Use & Circular Economy.

- Social —S1 Own Workforce, S2 Workers in Value Chain, S3 Affected Communities, S4 Consumers & End-Users.

- Governance —G1 Business Conduct.

ESRS E1 overlaps most with IFRS S2: both use the TCFD pillars, Governance, Strategy, Risk Management, Metrics & Targets, but ESRS adds EU-specific disclosures (e.g., EU taxonomy alignment, absolute-target consistency with the EU Climate Law).

4. Legal Mandate and Assurance Requirements

- Mandatory compliance: Large EU companies must include an ESRS-compliant sustainability section in the management report for fiscal years starting 2025 (earlier for some).

- Assurance: From 2025, reports are subject to limited assurance, with the Commission considering a longer ramp-up to reasonable assurance.

- Audit parity: Sustainability data will face audit scrutiny similar to financial statements, reinforcing reliability.

5. Interoperability with Sustainability Standards Board (ISSB) Standards: IFRS S1 and IFRS S2

The EU and ISSB pursue a building-blocks strategy: IFRS S1/S2 deliver a global investor baseline, while ESRS layers on wider stakeholder information. In May 2024, EFRAG and the ISSB issued joint interoperability guidance to help companies produce one report that satisfies both regimes with minimal reconciliation. In practice:

- ESRS generally covers IFRS S1/S2 requirements.

- Incremental mapping tables show where additional ESRS disclosures (e.g., impact metrics, EU-policy references) exceed the ISSB baseline.

- Companies can streamline by designing data systems that capture all ESRS datapoints, then extract the ISSB subset for investor-focused reporting.

6. Key ESRS Concepts and Data Expectations (2025 Onward)

| Theme | ESRS Requirement | Compliance Implication |

|---|---|---|

| Climate Transition Plan | Describe 1.5 °C-aligned strategy, science-based targets, and capex alignment with EU objectives. | Link transition plan to financial strategy and EU taxonomy eligibility. |

| GHG Emissions | Disclose Scopes 1, 2 and 3; intensity metrics for high-impact sectors; carbon-offset use with gross/net split. | Build data pipelines for full value-chain emissions; avoid netting offsets. |

| Scenario Analysis | Explain methodology and outcomes if scenarios are used; include both high-physical-risk and 1.5 °C transition pathways when applied. | Align narrative with IFRS S2 scenario output to ensure consistency. |

| Broad ESG Metrics | Workforce diversity, gender pay gap, training hours, human-rights due-diligence processes, anti-corruption controls and more. | Integrate HR, supply-chain and compliance functions into ESG data collection. |

| EU Climate Policy Links | Report consistency with EU 2030/2050 targets; disclose taxonomy-aligned revenue and capex. | Coordinate sustainability and finance teams to tag taxonomy-eligible activities. |

7. Scope of Application and Ongoing Regulatory Refinements

- Coverage: EU firms meeting two of three thresholds (≥250 employees, ≥€40 m turnover, ≥€20 m assets) and nearly all listed companies must report.

- Third-country groups: Non-EU parents with >€150 m EU revenue plus a large subsidiary or branch must publish EU-specific sustainability data from 2028.

- 2025 omnibus proposal: The Commission is weighing scope reductions for smaller firms and prolonged limited-assurance phases—compliance teams should monitor updates closely.

8. Compliance Takeaways for Multinational Companies

- Embed double-materiality screening into risk and impact assessments.

- Map ESRS disclosures to the Sustainability Standards Board (ISSB) Standards (IFRS S1 and IFRS S2) using the 2024 interoperability matrices.

- Build audit-ready data systems for Scope 1-3 emissions, workforce metrics and EU-policy-linked indicators.

- Align climate transition plans with both ESRS E1 and IFRS S2 narratives to ensure one cohesive story for regulators, investors and other stakeholders.

- Track regulatory refinement—the EU may adjust scoping, assurance and timelines; early awareness reduces last-minute surprises.

ISSB IFRS vs ESRS: Interoperability, Gaps & Overlaps

While both frameworks borrow heavily from the TCFD four-pillar model, they differ in materiality lens, disclosure breadth and policy objectives. Understanding these divergences early reduces duplicate work, audit findings and green-washing risk.

1 | Materiality & Disclosure Scope

| Aspect | IFRS S1 / IFRS S2 (Single / Financial Materiality) | ESRS (Double Materiality) | Compliance Consequence |

|---|---|---|---|

| Core audience | Investors, lenders, creditors (“primary users”) | Investors plus employees, communities, regulators, civil society | ESRS captures all IFRS-relevant data and extra impact-only topics. |

| Required lens | Outside-in: disclose when a sustainability matter affects enterprise value. | Outside-in and inside-out: disclose significant impacts on people or planet, even if no near-term financial hit. | An ESRS report is a superset; an IFRS-only report omits impact-only issues. |

| Illustrative example | Polluting a river is disclosed only if it triggers financial risk (e.g., fines). | Same pollution is disclosed because of environmental harm, regardless of immediate cost. | Starting with ESRS double-materiality assessment captures both needs. |

Practical Tip:

Document the dual-materiality process transparently. The financial-materiality judgement required by IFRS S1 plugs directly into the “financial” half of the ESRS matrix, streamlining auditor review and investor use.

2 | Climate Strategy & Scenario Analysis

| Requirement | IFRS S2 | ESRS E1 | Interoperability Action |

|---|---|---|---|

| Scenario analysis | Mandatory. At least one quantitative scenario, including a 1.5 °C pathway and a high-physical-risk pathway. | Encouraged but disclose if used. Guidance expects both 1.5 °C and high-emission scenarios. | Perform ISSB-level scenario analysis; one disclosure meets both rules. |

| Transition plan | Explain how the entity will meet climate targets (legal or voluntary) and adjust its business model. | Describe the plan’s alignment with EU 2030/2050 goals and Paris alignment; detail if misaligned. | Craft a single narrative that references legal targets, science-based milestones and EU policy links. |

| Risk-management processes | Describe identification, assessment and integration into ERM. | Same, plus stakeholder-engagement dimension. | Augment IFRS text with stakeholder input explanation for ESRS. |

3 | Carbon-Credits & Offsets

- IFRS S2 — disclose carbon-credit integrity, verification schemes and how credits affect targets or metrics.

- ESRS E1 — add details when credits underpin neutrality claims, including permanence, vintage and geographic origin.

Unified approach: Present gross emissions first, then offsets, cite verification standards, and tag extra ESRS datapoints (origin, type, permanence) in a dedicated sub-section.

4 | Financed & Value-Chain Emissions

- Financial institutions must publish Category 15 Scope 3 (financed) emissions under IFRS S2.

- ESRS extends Scope 3 to all sectors and expects intensity ratios for high-impact industries.

Action: Build a single Scope 1-2-3 data pipeline that captures financed or value-chain emissions at source-activity level; flag PCAF-aligned metrics for banks and add ESRS-required intensity KPIs where relevant.

5 | Stakeholder & Governance Disclosures

| Topic | IFRS S1 / S2 | ESRS | Combined Disclosure Hint |

|---|---|---|---|

| Governance | Board oversight, management roles, remuneration links. | Same elements plus policies on business conduct, lobbying, anti-corruption. | Expand governance section with ESRS G1 content; tag IFRS cross-refs to financial impacts. |

| Social metrics | Only if financially material (e.g., labour shortages threaten profitability). | Workforce diversity, pay gap, supply-chain human-rights indicators always material if significant. | Incorporate social KPIs; label those relevant to enterprise value for IFRS readers. |

6 | Roadmap for Dual Compliance

- Run a double-materiality assessment.

- Map disclosures: flag which datapoints satisfy IFRS S1/S2 vs extra ESRS impact metrics.

- Centralise data: adopt one ESG system capturing Scope 1-3, financed emissions, workforce, biodiversity, etc.

- Draft one narrative that:

- aligns with the four TCFD pillars,

- embeds EU policy references where needed, and

- clearly links sustainability matters to financial statements.

- Audit-ready evidence: maintain documentation of scenario assumptions, materiality judgements and data controls.

Metrics & Targets: Emissions, Energy and Financed-Emissions

(Aligned with the Sustainability Standards Board (ISSB) Standards—IFRS, IFRS S1 and IFRS S2—and the EU’s ESRS)

1 | GHG Emissions: Scopes 1-2-3 (Core Requirement)

- Mandatory disclosure of Scopes 1, 2 and material Scope 3 in CO₂-e, following the GHG Protocol.

- Scope 3 may be omitted only in the first reporting year where data collection is impracticable; full disclosure is expected thereafter.

- Organisational boundary should align with the financial-statement consolidation perimeter, maintaining investor comparability.

ESRS E1

- Requires the same Scopes 1-2-3 plus:

- Expects a reconciliation of the financial denominator used for intensity calculations.

- Location- and market-based Scope 2 figures.

- Category-level detail for significant Scope 3 sources.

- Intensity ratios (tCO₂-e / € turnover) for high-impact sectors.

- Breakdown of Scopes 1-2 by source (fuel, process, fugitive) and, where relevant, by business segment.

Compliance Insight

Start with ESRS granularity, then tag the investor-material subset to meet IFRS S2. Maintain clear explanations of any Scope 3 estimation methods and boundary choices.

2 | Financed Emissions—Banks, Insurers & Asset Managers

| Framework | Requirement | Practical Step |

|---|---|---|

| IFRS S2 | Publish absolute and intensity metrics for Scope 3 Category 15 (financed emissions) using PCAF-aligned methodology. | Build data pipelines that capture borrower / investee emissions or credible proxies. |

| ESRS | No dedicated quantitative DR yet; however, AR 46 and ESRS 1 §131 instruct financial institutions to apply recognised standards—implicitly IFRS S2 / PCAF—whenever material. | EU financial firms should incorporate IFRS S2 financed-emission metrics now to future-proof reports and achieve dual compliance. |

3 | Energy Metrics and Other Environmental Data

ESRS E1 adds compulsory detail for all sectors:

- Total energy consumption (MWh) split by source: renewable vs non-renewable; electricity, heating, cooling, self-generated vs purchased.

- Fossil-fuel breakdown (coal, oil, gas) for high-impact sectors.

- Energy-intensity KPI (MWh / € turnover) where energy is a key climate driver.

IFRS S2 has no cross-industry energy-consumption metric; energy data appear only within selected SASB industry guidance.

Beyond climate, ESRS topical standards (E2–E5) mandate water, pollution, biodiversity and circular-economy metrics—areas not yet covered by ISSB’s global baseline.

4 | Targets, KPIs & Carbon Pricing

- Both regimes require disclosure of climate-mitigation targets (absolute or intensity), base year, timeline and progress.

- IFRS S2 specifically asks for disclosure of any internal carbon price used in decision-making.

- ESRS does not explicitly require an internal carbon-price metric but allows voluntary inclusion within strategy or transition-plan narrative.

5 | Carbon Credits & Offsets—Transparency First

Shared principles: present gross emissions before offsets; demonstrate credit integrity.

| Focus Area | IFRS S2 | ESRS E1 |

|---|---|---|

| Disclosure depth | Volume, type of projects, certification scheme, factors affecting credit quality. | Same elements, plus ban on counting avoided emissions as reductions and explicit tie-in to any “carbon-neutral” claims. |

| Investor lens | Emphasises reliability of net-zero pathways. | Emphasises reliability and substantive contribution to EU and global climate goals. |

Best practice: Provide a dedicated table detailing offset volumes, project types (nature-based removals vs avoidance), standards (Gold Standard, Verra, etc.) and permanence risk.

6 | Action Checklist for Dual Compliance

- Develop one enterprise-wide GHG inventory—capture Scopes 1-3 with ESRS-level granularity; flag IFRS-required subsets.

- Quantify financed emissions if you are a financial institution; apply PCAF regardless of ESRS’s current silence.

- Track energy data (consumption, mix, intensity) to satisfy ESRS and anticipate future ISSB expansion.

- Align targets with science-based pathways; disclose internal carbon price where used.

- Validate offsets—use high-quality credits, disclose certification and avoid over-reliance.

Presentation, Audit & Legal Considerations

(Contextualised for the Sustainability Standards Board (ISSB) Standards—IFRS, IFRS S1 and IFRS S2 and the EU’s ESRS under CSRD)

1 | Location of Reporting

| Item | ESRS (CSRD) | ISSB—IFRS S1 / IFRS S2 | Practical Implication |

|---|---|---|---|

| Placement | Must appear inside the annual management report filed with EU regulators. | Location not prescribed; may be a standalone sustainability report, integrated report, or section of the annual report, subject to local rules. | Multinationals often integrate content so that a single data set feeds both formats; use cross-references to link financial-statement notes to sustainability narrative. |

2 | Assurance & Internal Controls

- ESRS → Limited assurance is mandatory from FY 2024, with a legislative option to upgrade to reasonable assurance in later years.

- ISSB → Framework does not require assurance, but regulators, stock exchanges and investors increasingly expect it; many issuers already seek voluntary reviews.

- Best practice: Establish Sarbanes-Oxley-style controls for ESG data, embed audit trails and conduct pre-assurance dry runs.

3 | Regulatory Enforcement & Jurisdictional Risk

| Region | Enforcement Trigger | Potential Consequences |

|---|---|---|

| European Union (ESRS) | Omission or misstatement in the management report. | Regulatory sanctions, financial penalties, reputational damage. |

| Jurisdictions adopting ISSB—IFRS S1 & S2 | Failure to meet stock-exchange listing rules or local disclosure laws (e.g., Hong Kong climate rules, Canada’s forthcoming mandates). | Exchange censure, delisting risk, loss of investor confidence. |

| Investor enforcement | Asset-manager voting policies, stewardship guidelines and lender covenants. | Higher cost of capital, restricted market access. |

4 | Interoperability Checklist (IFRS–EFRAG Guidance)

| Area | ISSB Requirement | ESRS Requirement | Dual-Compliance Tactic |

|---|---|---|---|

| Scenario analysis | Must include a 1.5 °C pathway and high-physical-risk scenario. | Must disclose if scenario analysis used; strongly expects the same pathways. | Perform ISSB-level analysis and reference it in ESRS section. |

| Financed emissions (banks, insurers, AMs) | Quantify Category 15 Scope 3 using PCAF. | Not yet in core ESRS, but guidance points to IFRS S2. | Include financed-emissions table in EU report. |

| Energy mix / intensity | Not cross-industry mandatory. | Detailed disclosure for high-impact sectors. | Capture energy data once; label investor-relevant subset for ISSB section. |

| Double materiality | Single (financial) materiality only. | Double materiality assessment required. | Conduct full assessment; tag financially material items for ISSB. |

5 | Action Plan for Compliance Teams

- Map reporting locations: design a modular report that can be inserted into EU management filings and re-purposed as an ISSB section or standalone document.

- Embed ESG controls: align data-governance framework with financial-control standards to prepare for external assurance on sustainability metrics.

- Monitor local rules: track each listing venue’s adoption timeline for the Sustainability Standards Board (ISSB) Standards—IFRS, IFRS S1 and IFRS S2—as well as CSRD scope refinements.

- Use interoperability guidance as a live checklist; update disclosures whenever ISSB or ESRS application FAQs evolve.

- Communicate internally: ensure finance, sustainability, legal and investor-relations teams share one source of truth, avoiding duplication and inconsistencies.

The Role of Institutional Investors in Driving Adoption of the Sustainability Standards Board (ISSB) Standards

1 | Why Asset Owners and Managers Care

Large investors, asset managers, insurers, pension funds and sovereign-wealth funds, depend on decision-useful, comparable ESG information to price risk, allocate capital and meet their own net-zero or stewardship commitments. Their collective influence explains:

- the rapid formation of the International Sustainability Standards Board in 2021;

- the speed with which more than 30 jurisdictions began incorporating IFRS S1 and IFRS S2 after issuance; and

- the steady alignment between the ISSB’s global baseline and the EU’s European Sustainability Reporting Standards (ESRS).

2 | Global Investor Endorsement of the ISSB Baseline

- Mid-2024 investor call-to-action: A coalition of 120 global investors publicly urged regulators to mandate IFRS S1 and IFRS S2 by 2025 for both public and large private companies. Their rationale: one worldwide framework lowers reporting costs, closes data gaps and improves comparability.

- Capital-market signal: The statement accelerated rule-making in Canada, Japan, Hong Kong, Malaysia, Nigeria, Brazil and other markets, reinforcing that ISSB adoption is now a prerequisite for full market access.

3 | IOSCO Endorsement: A Regulator Cascade Triggered by Investors

IOSCO’s July 2023 endorsement of IFRS S1/S2 followed intense investor lobbying via the G20, G7 and the Financial Stability Board. IOSCO concluded the standards are “fit for purpose” for investor-focused climate and sustainability disclosure, prompting member regulators, covering ~95 % of global securities markets—to explore mandatory uptake.

4 | Investor Coalitions Embed ISSB Expectations

| Coalition / Initiative | Influence Mechanism | ISSB-Related Expectation |

|---|---|---|

| Climate Action 100+ (USD 68 trn AUM) | Net-Zero Company Benchmark | Public commitment to TCFD or Sustainability Standards Board (ISSB) Standards—IFRS S1 and IFRS S2. |

| CDP | Environmental disclosure platform used by >18 000 companies | 2024 questionnaire aligned with IFRS S2 metrics and narrative structure. |

| Principles for Responsible Investment (PRI) | Signatory reporting framework | Incorporating ISSB data points to streamline investor analysis. |

5 | Shaping ESRS and Other Regional Rules

European investors pressed for interoperability so cross-border portfolios are comparable. Their feedback helped ensure ESRS E1 mirrors IFRS S2 pillars and terminology. The same investor logic guided Canada’s creation of a local Sustainability Standards Board and Japan’s decision to allow voluntary ISSB reporting. Emerging-market regulators, from Nigeria to Brazil, are likewise adopting ISSB standards to attract capital and reduce transparency risk premia.

6 | How Investors Use the Data

- Portfolio alignment & stewardship – Net-zero-committed managers need high-quality Scope 1-2-3 and financed-emission figures to track progress and engage laggards.

- Voting & shareholder proposals – Resolutions now demand ISSB-aligned climate risk reporting; majority support rates keep climbing.

- Risk pricing – Banks, rating agencies and insurers integrate ISSB-structured data into credit spreads and underwriting decisions, rewarding issuers with transparent climate strategies.

Best Practices for Dual Compliance with the ISSB Standards

1. Launch a Robust Double-Materiality Assessment

Begin with a cross-functional, stakeholder-informed evaluation of financial and impact materiality. Map every relevant sustainability topic, then tag each issue as financially material, impact-material or both. Record methodology, results and board sign-off in a transparent matrix to anchor disclosure decisions and satisfy ESRS documentation requirements while feeding investor-focused ISSB content.

2. Build on the ISSB Global Baseline and Layer ESRS Add-Ons

Treat the IFRS S1 and IFRS S2 core, governance, strategy, risk management, scenario analysis and Scope 1-2-3 emissions, as the universal foundation. Next, bolt on ESRS-specific disclosures: energy consumption, biodiversity, workforce diversity, pay-gap details, EU taxonomy alignment and any other topical metrics triggered by impact materiality. Use an internal cross-reference table so one narrative serves both audiences without duplication.

3. Use ISSB–ESRS Interoperability Guidance as a Live Checklist

Leverage the 2024 joint mapping tables to ensure nothing slips through the cracks—e.g., financed-emission metrics for banks (IFRS requirement) or community-impact disclosures for ESRS. Treat the guidance like an internal audit tool to validate dual compliance before publication.

4. Embed Financial-Grade Governance and Controls for ESG Data

Install enterprise-wide data governance: clear ownership, automated consolidation, audit trails and periodic internal reviews. Apply SOX-style controls to emissions, energy, safety and diversity figures so they withstand limited assurance under CSRD and anticipated assurance of ISSB reports.

5. Perform a Gap Analysis and Roadmap to Deadlines

Compare current disclosures with both frameworks, flag shortfalls (e.g., scenario modelling depth, Scope 3 category coverage, water-use metrics) and assign owners, budgets and timelines. Create a milestone calendar that syncs with annual-report production and audit cycles.

6. Form a Cross-Functional Steering Committee

Unite Finance, Sustainability, Risk, HR, Operations, Legal and Investor Relations under board oversight. Provide training on Sustainability Standards Board (ISSB) Standards, IFRS, IFRS S1 and IFRS S2, and ESRS so every data owner understands deadlines and quality expectations.

7. Strengthen Scenario-Analysis Capability

Adopt or enhance quantitative and qualitative climate-scenario tools, covering at least a 1.5 °C transition pathway and a high-physical-risk pathway. Document assumptions, models and results for disclosure and continuous strategic use.

8. Align Sustainability and Financial Narratives

Ensure sustainability information explicitly links to financial-statement impacts, asset impairments, capex plans, revenue forecasts and risk factors. Consistency between the management report, notes and ESG disclosures is critical for both frameworks and boosts investor trust.

9. Monitor Emerging Standards and Jurisdictional Nuances

Track exposure drafts for forthcoming topics (biodiversity, human capital) and sector-specific ESRS. Maintain a multi-jurisdictional compliance matrix so local variations, such as SEC climate rules or country-specific assurance formats—are incorporated early.

10. Craft a Coherent, Forward-Looking Narrative

Beyond technical compliance, weave a clear story: strategic priorities, transition-plan milestones, opportunities unlocked by sustainable innovation and progress against targets.

11. Engage Investors and Regulators Proactively

Host ESG investor briefings, respond to stewardship questionnaires and participate in industry working groups. Early dialogue helps prioritise data investors value most and positions the company as a cooperative, transparent issuer.

12. Pilot Internal Audit and Voluntary External Assurance

Have internal audit test ESG controls, then run a dry-run limited-assurance engagement with your external auditor. Early assurance uncovers gaps, de-risks future audits and signals authority and trustworthiness to the market.

Conclusion & Outlook: Turning Compliance into Strategic Advantage

- Convergence is accelerating. The Sustainability Standards Board (ISSB) Standards provide a global investor baseline, while the ESRS adds depth for EU stakeholders.

- Building-block reporting wins. Collect data once, disclose it in modular formats to satisfy multiple regimes, and update the core dataset as new standards (e.g., IFRS S3, sector ESRS) emerge.

- Investor scrutiny will intensify. Standardised data will drive capital-allocation decisions, credit spreads and index inclusion. Transparent, assured reporting will lower perceived risk and cost of capital.

- Regulatory enforcement is imminent. Early, full compliance, underpinned by robust governance, scenario analysis and double-materiality insight, positions companies for smooth audits and reputational upside.

By integrating these best practices into corporate DNA, organisations transform mandatory reporting on IFRS and ESRS into strategic resilience, operational efficiency and enhanced market confidence, key advantages in the rapidly evolving sustainable economy.

Reduce your

compliance risks